A number of hypotheses have been put forward to explain the huge market swings seen in the first four months of this year, but most can be questioned, says Lukas Daalder, Chief Investment Officer of Robeco Investment Solutions.

“Markets have been pretty volatile since the start of the year and it is tempting to look for scapegoats to explain it all,” he says. “The loss of credibility of central banks and low interest rates, in combination with volatility enhancing trading strategies, probably all have played a role – and could play a very important role in the future. But they simply cannot be blamed for all the volatility we have seen in recent months.”

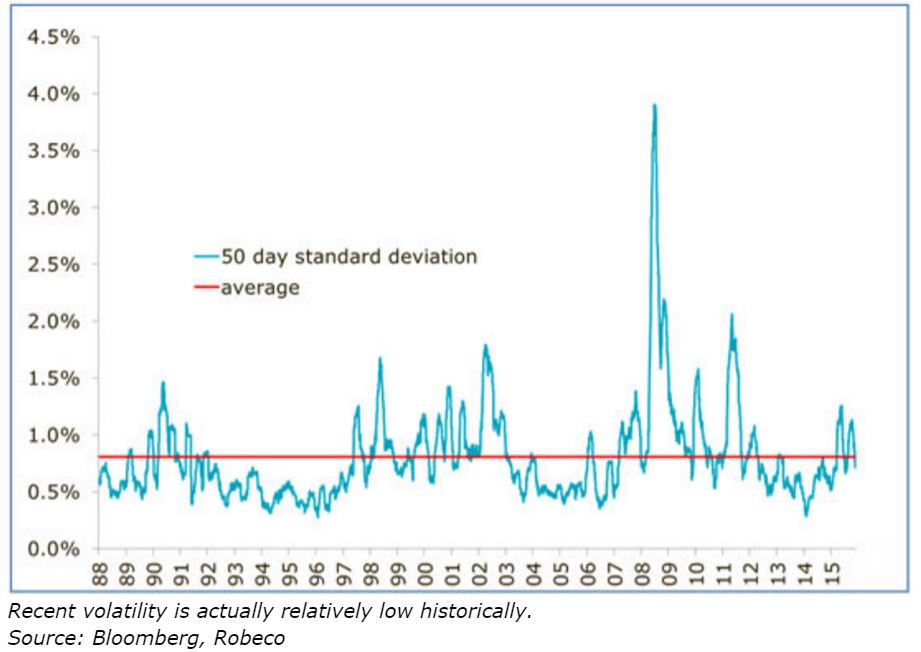

“Looking at the development of the standard deviation in the MSCI World Index daily changes shows no clear trend change, but rather a normal rise in volatility, following the remarkable low point in volatility reached in 2014. Even if we take the peak in volatility seen during the past six months, it does not rank in the highest 10% measured from 1988.”

Nothing to see here

“Put differently, things may feel very volatile, but history tells us this is nothing out of the ordinary,” adds Daalder, whose multi-asset portfolio maintains a neutral position in equities. “What we have seen is the natural rise in volatility that is connected with the later stages of the recovery in global stocks. On balance, stocks still move higher in this stage, but these gains come at a higher volatility. Range trading is the best option here, buying into the sell-offs and selling into the rallies.”

So is this normal? Yes, says Daalder, though he concedes that markets can be irritatingly bipolar, moving from ‘Sell everything!’ to ‘Buy everything!’ in the same quarter. “We know that volatility is a normal feature of financial markets. We lived through the 2007-2009 crisis and survived the 2000-2002 drawdown, so we are well aware that things can get rocky at times,” he says.

“The thing that we are questioning here is the fact that we continually seem to go from an ‘end-of-the-world’ kind of market to a ‘move-along-nothing-to-see-here’ trading environment in just a matter of weeks. Is this just business as normal (in the later stages of a bull market), or are there arguments to suspect that there are other, more structural elements at work?”

Five reasons to be cheerful

It is the former, says Daalder, who says there are six principle arguments for periods of higher volatility, none of which are structural:

1. More uncertainty in the underlying macro data: In fact, the evidence shows that GDP data has been a lot less volatile over the past four quarters when compared to the past. And the Citi Surprise index, which tracks the deviation between data releases and consensus expectations, has not seen large swings.

2. Low interest rates: Weird things happen in theory when interest rates drop to zero or below that. But the data does not show a correlation between low rates and lower or more volatile stock market returns, and when company earnings prospects are included, the impact of rates is pretty hard to prove.

3. Weakening central bank power: If markets start to question the effectiveness of monetary policy, it is reasonable to think this will lead to structurally higher volatility. However, the fact that the current policy mix is becoming less effective should not be mistaken for signaling the end of the strong force that central banks can still exert.

4. Riskier trading strategies: The rise of strategies such as Value at Risk (VaR) or momentum trading, can indeed amplify risk that was already in the market. But this is a phenomenon observed more in sovereign bonds rather than in naturally more volatile equities. And these strategies comprise less than 1% of the total investment market.

5. Increased ‘risk-off’ regulation: Declining stock markets can induce pension funds to reduce risk to meet regulatory requirements, for example by selling stocks into an already depressed market. Although this can play a role in a longer-term perspective, it is less likely to have caused the swings seen in the first four months of this year.

Don’t sell in May, don’t go away

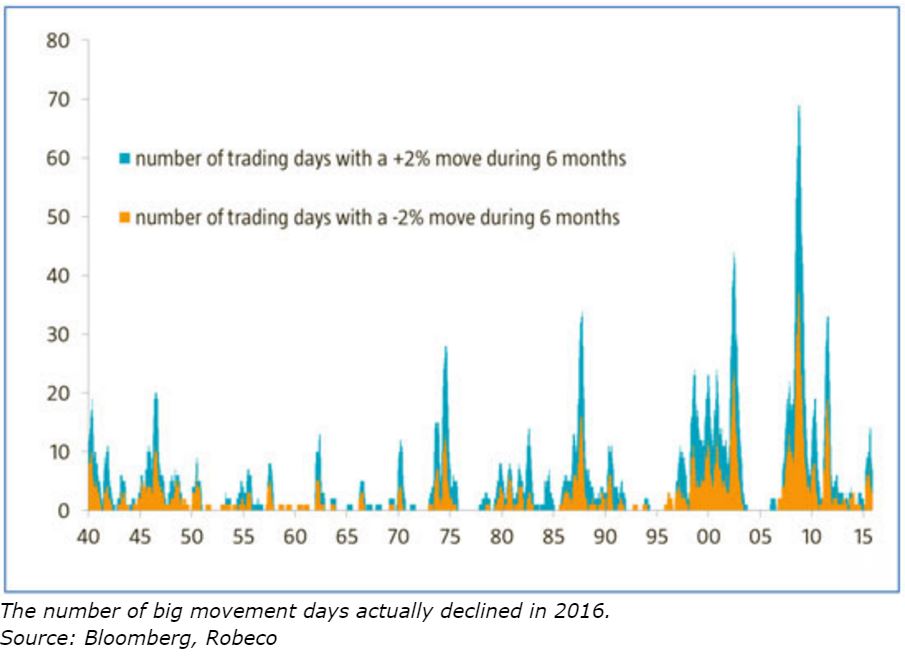

Concluding, Daalder says that while it is impossible to remove often irrational sentiment from the market, the old adage of ‘Sell in May and go away’ is no more applicable in this month than it apparently was in January. “When worldwide stocks ended the first week of 2016 down by more than 6%, the ‘this-will-be-a-lost-year’ commentaries came in early. In fact, ’Sell everything!’ was the key takeaway,” he says.

“It wasn’t until rumors of an oil production cut by OPEC finally managed to break the downward spiral of the price of a barrel of oil that sentiment shifted. From then on, ‘Buy everything!’ was the name of the game, and most, if not all, of the losses were reversed in the weeks that followed. In fact, if you had missed the first four months, you might draw the conclusion that 2016 has been a pretty uneventful year so far…”

){kind=link}