The market crash that began in March sent the spread of EM debt (for the hard currency aggregate) to nearly 700 bps. It is now only 30 bps away from the pre-crisis level. This spread tightening reflects the ongoing economic recovery EM countries. Trends in Covid-19 are taking the right direction, except for India. In many countries, authorities are easing restrictions even before the virus is yet to be sustainably contained. As a result, real-time activity indicators are improving, suggesting that Latin America and Asia are about -15% off from average, when MEA countries are at around -5%. The Chinese recovery, which is firming and now spreading to consumption, has also been a key support for EM countries. Moreover, surging global dollar liquidity and the recovery in global trade provided a healthier environment for EM assets. Lastly, the intensifying political risks in DM relative to EM countries lured investors in EM HC debt.

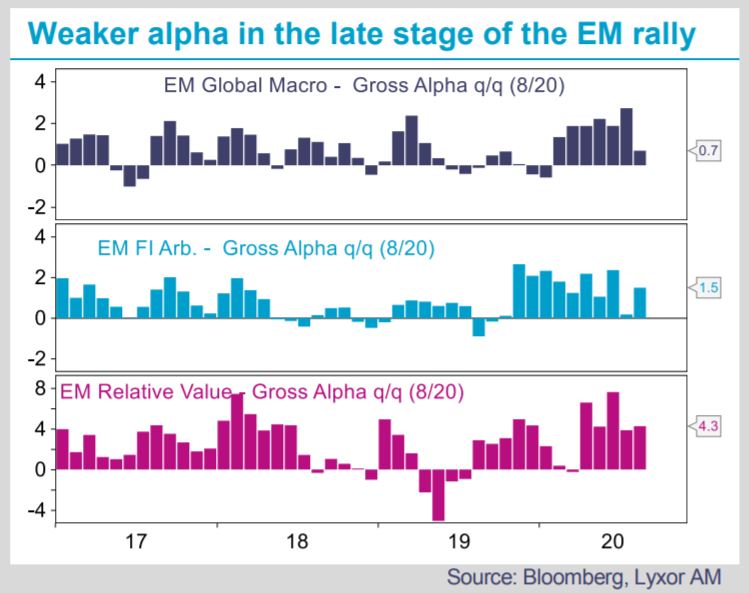

Hedge funds allocating to EM debt (including global macro, fixed income or relative-value styles) successfully navigated the market crash in aggregate. They benefitted from their reduced overall exposures and their tilt on higher quality issues. Since then, they added risk in their portfolio, favoring weaker quality issues until July, allowing them to keep the lion’s share of their alpha since March. They tended to miss the late stage of the rally in August. Concerned by the weaker summer liquidity, less attractive valuations and record EM debt issuance, they started to build up their cash positions. Meanwhile, the dispersion across EM debt assets, which climaxed in April, has vanished across countries, ratings, sectors, and maturities. Besides, their pairwise correlations steadily rose since June, suggesting a less diversified set of drivers and more sensitivity to flows returning in the space instead. Additionally, regional relative-value opportunities have shrunk. Market and fundamental models suggest EM HC debt fair spread levels are about 40 bps higher, both on a relative and absolute basis. All in all, the rally in EM assets has eroded the potential for alpha generation. Hedge fund managers currently stay long on average but are keeping dry powder to capture opportunities at a later stage.

We believe this weaker alpha environment is only temporary. Current EM debt spreads might not reflect the uneven EM countries recovery prospects. The pandemic left deep scars in most of them, which are calling for more stimulus support.

Authorities will need to find a delicate policy balance with enough fiscal expansion to support growth while avoiding capital outflows. Heterogenous EM inflation trends (and central banks target rates) are likely to become major differentiators going forward. Moreover, EM countries will likely be unevenly successful in finding new growth drivers as deglobalization accelerates. A softer commodity cycle, concentrated supply chains, DM ageing, and protectionism could prevent global trade from reverting to the previous cycle levels. Increasing competition between U.SChina and the upcoming U.S. elections would also unevenly affect EM countries.

We therefore expect a more discriminating environment for EM assets to return, favorable for alpha generation. In the meantime, we still think EM debt provides valuable diversification in credit portfolio, with an annualized 4/5% yields.

to nearly 700 bps. It is now only 30 bps away from the pre-crisis level. This spread tightening reflects the ongoing economic recovery EM countries. (...)){kind=link}