While we thought that sterling would come under intense pressure as global investors fled the currency, the pound has been devalued to a greater extent than analysts anticipated and we believe it will weaken further to $1.10 next year. The flipside is that both equities and fixed income markets have performed above expectations, largely as a result of ongoing quantitative easing and central bank intervention, both by the Bank of England and the European Central Bank.

But, as I said last month, there is a rising fear that the theory of central bank intervention is not matching the reality in so much as ongoing monetary stimulus may be harming markets as much as it is helping them – certainly monetary stimulus is doing little to boost productivity growth. Against that backdrop, if inflation were to pick up and interest rates were to rise, there could be significant implications for risk assets, given how a yield-starved world has been forced to hunt for returns everywhere else.

We have clearly had an extremely reassuring central bank ’comfort blanket’ put around what, on the face of it, look to be very expensive risk assets; and this has underpinned valuations and helped us navigate through a challenging macro-economic and geo-political backdrop. As a result, people have become used to explaining away what in absolute and historic terms look to be expensive valuations, by referencing the bond market at all times.

That to me feels relatively fragile and if you overlay that with an increasing recognition that monetary policy is doing bad things as well as good things, along with socio-economic tensions globally, then the cry for a fiscal response must be on the increase.

In the US the election is looming and both parties appear to have greater appetite for fiscal measures than historically, but this may not come about in the short-term given the ongoing political polarisation, capped by a divisive Presidential campaign that will likely see a divided government regardless of who is elected. The forthcoming Autumn Statement may raise the prospect for fiscal policies in the UK – where the government has been somewhat critical of the Bank of England’s monetary policy – while Europe and Japan arguably need fiscal easing the most. From a bond market perspective the expectation is that curves would steepen materially if there was a regime shift into fiscal.

So while our central case is that the status quo is maintained and we continue to experience low inflation, low growth, and low interest rates, we are mindful that if growth picks up on the back of increased fiscal stimulus, the interest rate environment is challenged for the same reason and the current valuation of risk assets is contested, we could see a dislocation in markets. This ultimately depends on bond yields rising, how quickly they might do so, and where we ultimately end up, but the worst-case scenario is that risk assets become a turbulent place to be in the next six months.

A significant pick-up in inflation is one factor that could challenge the status quo, so our thoughts have turned to whether the world is being too complacent about inflation. In the UK inflationary pressures linked to a weaker sterling are undoubtedly hitting suppliers and making their way to retailers and we have already seen inflation in September beating analyst expectations. In the US, mild stagflationary pressures are present, with growth stable to slowing and price pressures building from both rising labour costs and powerful base effects that could see headline CPI inflation doubling to 2% by year-end. This could result in the Fed feeling bold enough to raise rates in December, which would likely increase volatility across risk assets.

Against this backdrop we remain neutral and cautious on equities. That said, we have been seeing pockets of opportunity, in particular within Asian emerging market equities. In this region, we see better and more stable growth prospects with most EM economies having adjusted to slower trade; scope for local monetary and fiscal support; reduced China fears; and rising capital flows. Crucially valuations are attractive, with earnings supported by the above factors and rising sales forecasts in 60% of countries in Asia. We are therefore seeing opportunities among high-yielding and high-growth Asian emerging market companies, though are mindful of the risks posed by any US interest rate rise and the impact of the US dollar.

This is my last update ahead of the US election, and whatever the outcome of the vote, history has shown us that there is usually a short sharp sell-off in equities for a brief period of time when a new president comes in and then the market returns to the status quo. However, what is potentially concerning is that markets and volatility do not really seem to be pricing a Trump victory which could be a risk if the unexpected were to happen.

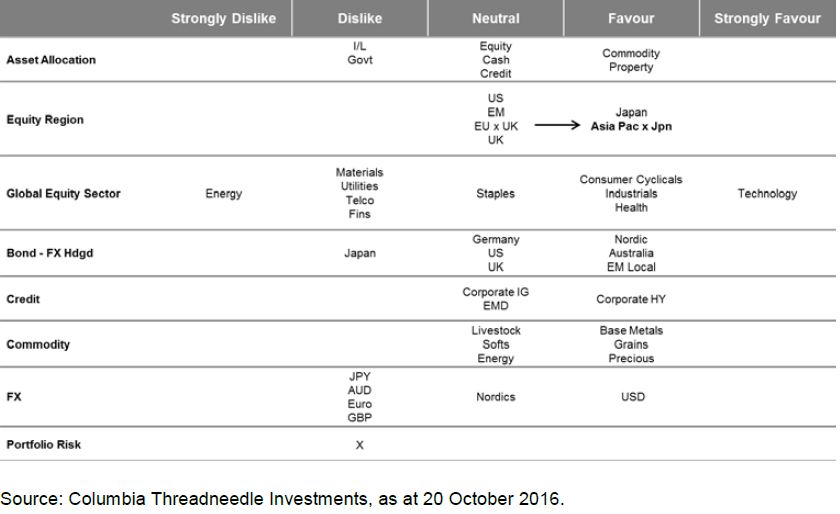

Figure 1: Asset allocation grid

){kind=link}