In the UK and US, meanwhile, markets have “baked in” the expectation that interest rates will be lower than today for the next 10 and 30 years respectively. It is all the more striking, then, that this has coincided with a meaningful repricing of short-end rates across developed markets[1]. The broad message across rates markets is: lower, and lower for longer.

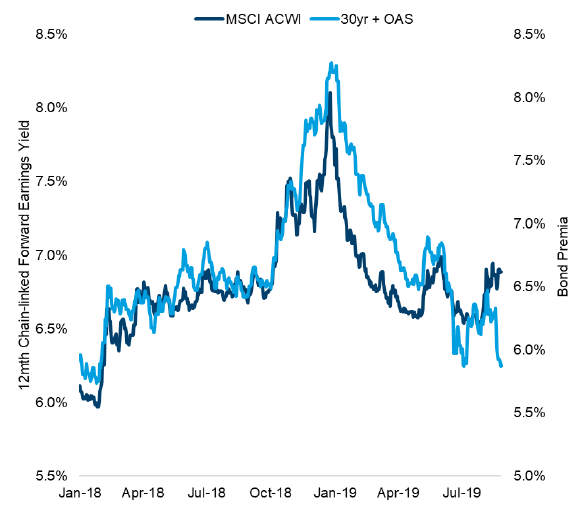

This plunge in yields is captured in the light blue line in Figure 1, which shows our heuristic of bond premia – 30-year yields with credit (option-adjusted spread) risk layered on top. For the past 18 months, shifts in bond premia have related very closely to movements in equity earnings yields, shown in dark blue. As discount rates have fallen (or risen), so future equity earnings have appeared more (or less) attractive today. This relationship was tested in August, as equities shrugged off the lurch lower in bond premia. What is going on?

It may be that the narrow path[2] markets have been discounting – whereby central banks cut rates enough to avert recession but not by enough to raise inflation such that rates may ultimately need to rise again – is becoming more tenuous. The re-escalation of global trade wars has raised uncertainty on the future of supply chains once more, putting a brake on companies’ investment plans and causing sharp swings in inventories. Insofar as changes in investment and inventories have, in turn, driven the entirety of economic contractions since the 1940s, without exception[3], it is feasible that equity investors are beginning to reassess.

Manufacturing and export-led Germany has probably just dipped into recession, and most major economies have reported chunky inventory draws. Ergo: ceteris paribus, stock prices should be lower.

Figure 1: Bond and equity premia

- Source: Columbia Threadneedle Investments, 30 August 2019.

But other things are not equal. Markets more broadly may have reviewed the reaction function of global central banks, and the US Federal Reserve in particular, to place greater weight on external factors such as trade than hitherto. The rationale here would be that risks to US (and global) growth and stability from trade policy is so outsized that a single tweet could “trump” all the analysis and forecasts made by the wealth of expertise in major central banks. Federal Reserve Chair Jerome Powell emphasised these risks in his speech at Jackson Hole on 23 August.

It is possible, if uncomfortable, to square this circle too with market behaviour. Although earnings expectations for global equities this year have fallen considerably to reflect modest contraction, 2020 expectations have held ground and discount rates have fallen such that earnings growth of around 7% is secured over the next twelve months. If Powell delivers on monetary policy, but President Trump doesn’t fully carry through threats on trade, risk assets could get a powerful short-term boost.

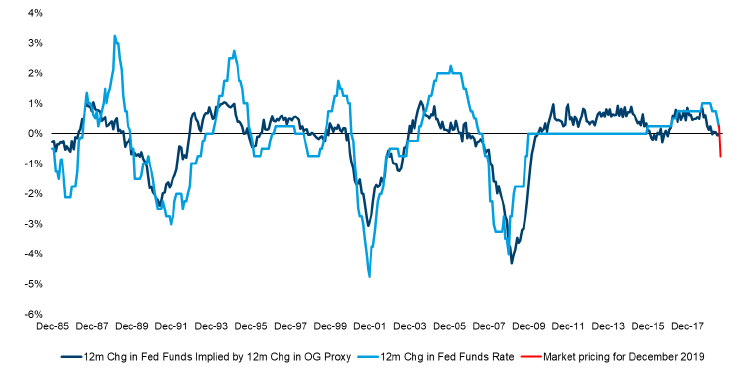

We are sceptical of the latter, which appears to be both dangerous and highly consequential over longer periods. Furthermore, the current underlying run rate of the US economy likely means that should a trade truce occur – which could happen at any moment – lower interest rates may not be appropriate. Our high frequency monthly proxy for the US output gap[4], for example, is the most elevated it has been since the mid-noughties.

Changes in the output gap also do a reasonable job of predicting wages with a 12-month lead and point to further pressures in the pipeline; they also suggest that the Fed Funds rate should be flat/unchanged (Figure 2). Simply put: the frameworks deployed by the US Federal Reserve would probably be pointing to rising, not falling, inflation risks right now.

On balance, the narrow path for asset markets turned more tenuous in August. We maintain our cautious risk and neutral equity view, in place since mid-March and end-May, alongside light overall duration risk.

Figure 2: US output gap and the Fed Funds rate

- Source: Bloomberg / Columbia Threadneedle Investments, 30 August 2019.

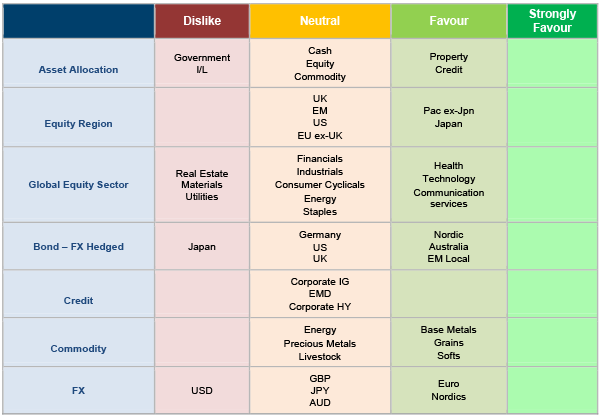

Figure 3: Asset allocation snapshot

- Source: Columbia Threadneedle Investments, 30 August 2019.

){kind=link}