The Spanish debt trajectory looks unsustainable. While the debt trajectory is by no means stable in the USA, UK and especially Japan, default risk appears low for now in all three cases.

A country’s current public debt and deficit situation have important implications for economic policy and for economic and financial market performance. In this article, potential future paths of the debt/GDP ratio are modeled in order to help assess fiscal sustainability, with a focus on the US, the UK, Japan and several Eurozone countries. Due to the low predictability of its deficit and growth figures, Greece’s debt paths have not been modeled. It seems rather clear, however, that Greece’s public sector debt is not sustainable, despite the restructuring earlier this year.

The "Mechanics" of Debt

Arithmetically, the development of the debt/GDP ratio depends mainly on five factors, which can be linked through the equation pictured:

- Initial level of government debt/GDP

![]() Initial level of government debt/GDP (B/Y).

Initial level of government debt/GDP (B/Y).

![]() Average interest rate on debt issued (i).

Average interest rate on debt issued (i).

![]() Budget balance excluding interest

payments/GDP (the so-called primary budget

balance, p/Y).

Budget balance excluding interest

payments/GDP (the so-called primary budget

balance, p/Y).

![]() Real economic growth (g).

Real economic growth (g).

![]() Inflation (?).

Inflation (?).

The effect of the debt stock and interest rates is straightforward: an increase in both will increase the interest burden and make it more difficult to stabilize the debt path. The most dramatic recent case is Ireland where debt jumped from very moderate to very high levels due to the government’s decision to guarantee the balance sheets of a number of failing banks. GDP growth is important in a simple accounting sense, as higher growth will increase GDP and thus mechanically lower the debt/GDP ratio. Inflation has comparable effects, as it increases nominal GDP growth, thus lowering the debt/GDP ratio for a given level of real GDP growth. The direct effect of economic growth and inflation is most important for high debt countries. For example, the 13 percent decline in Greek nominal GDP since 2009 has resulted in an increase of its debt/GDP ratio from 127 percent to 147 percent, all else equal. Had the economy instead grown by 10 percent as the US, its debt ratio would have fallen to 116 percent. Finally, higher interest rates and a more negative primary balance both raise the debt/GDP level.

Interactions Between These Variables Are Important

Apart from the direct effect of the single variables as shown in the equation, there are also important interactions between them. In recent years, ample academic evidence has accumulated which shows that high public sector debt reduces GDP growth. This may simply be because highly-indebted governments tighten fiscal policy to try to reduce the deficit, or it may be because consumers and companies cut back on expenditures when debt and deficits are rising (so-called "Ricardian" effects). In addition, an increasing debt ratio may lead to higher risk premia demanded by investors, which increases interest rates and slows investment spending. On the other hand, higher GDP growth typically improves the primary balance, as it increases tax revenue and lowers spending, for example for unemployment benefits. Higher inflation also typically improves the budget balance as it will boost tax revenue (also via so-called "tax bracket creep"), while spending should be less affected unless it is indexed to inflation. However, higher inflation might also increase inflation expectations, leading to rising interest rates. Such dynamics render forecasts for the deficit and debt path quite uncertain.

"Non-Linear" Sensitivity to Market Interest Rates

The direct impact of a temporary rise in market interest rates on debt is usually rather small, as most advanced countries have average debt maturities between 5 to 10 years and thus must only refinance a small part of their debt every year. It therefore takes time before higher market interest rates "feed through" into the overall cost of financing. Still, as could be observed in recent years and months, a rise in market interest rates can nevertheless lead to countries losing access to capital market financing quite quickly if the market begins to discount even higher interest rates in the future. The fact that interest payments on current debt are not that high doesn’t necessarily help if such negative market feedbacks set in. Moreover, once countries have "locked in" a high interest rate, it will also take time to lower the interest burden even if market interest rates fall again.

Other Keys to Debt Sustainability

Is there a definite level of government debt/GDP above which a government is unable to fund itself and has to default? The answer is a clear "no". For example, data by Reinhart & Rogoff (2010) show that governments have defaulted at a very wide range of debt/revenue ratios. Of course, as argued above not only the debt level itself but also the costs of servicing it is important. However, the ratio of interest payments to government revenue has not been a very helpful indicator of default risk either: Japan’s interest payments-to-revenue ratio is, for example, higher than those of Spain, but bond markets show little concern about Japan’s fiscal sustainability. More important for debt sustainability are likely to be factors such as the share of government debt held by – arguably more loyal – local investors and the share of debt that is denominated in foreign currency. In the case of the European "periphery" all debt is formally denominated in domestic currency (i.e. euro) but markets have started to worry that an exit from the Eurozone would transform the debt into foreign currency liabilities. Finally, a key to debt sustainability is the willingness of the central bank to act as "buyer of last resort". The fact that the ECB has shown considerable reluctance to take on this role has been a key reason for the worries over debt sustainability and default in the European "periphery".

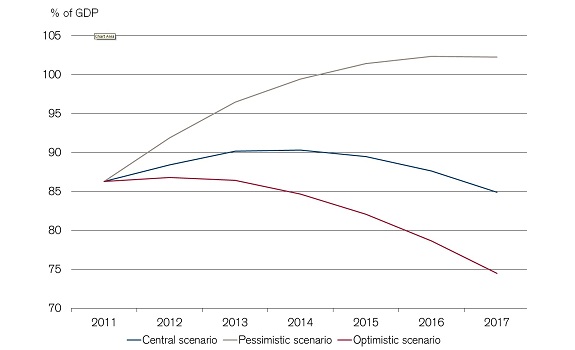

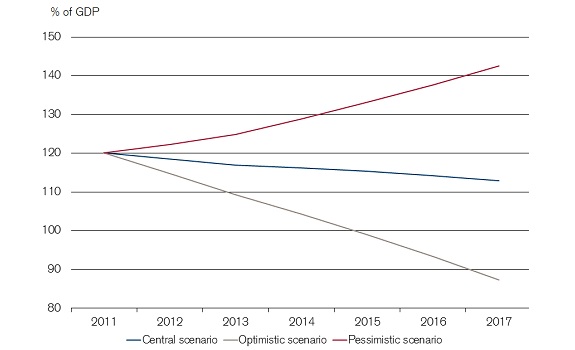

German, French and UK Debt Appear Sustainable

- Germany

The simulations show that Germany has the best fiscal outlook within the sample, as its debt ratio should fall sharply in coming years. Even in the case of a recession and higher interest rates the debt ratio would not rise fast.

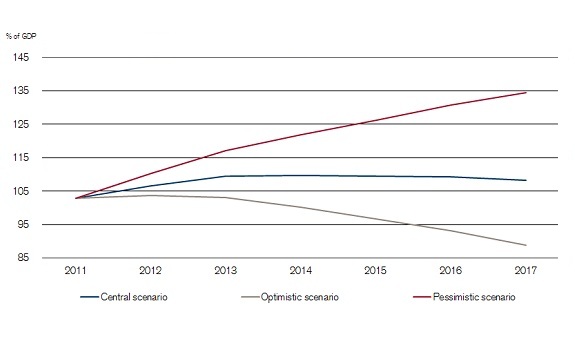

- France

In France, the trajectories are less positive but still point to sustainability. That said, if France witnessed a combination of recession and higher interest rates (pessimistic scenario) markets could get worried about debt sustainability.

- UK

The UK simulations look slightly worse than those for France. The UK, of course, has the advantage of a "fully owned" lender of last resort. However, if the Bank of England were required to intervene heavily in the case of the pessimistic scenario, one could imagine a crisis developing in which the GBP began to depreciate, bond yields would rise in response to depreciation and inflation fears, resulting in a currency-cum-debt crisis.

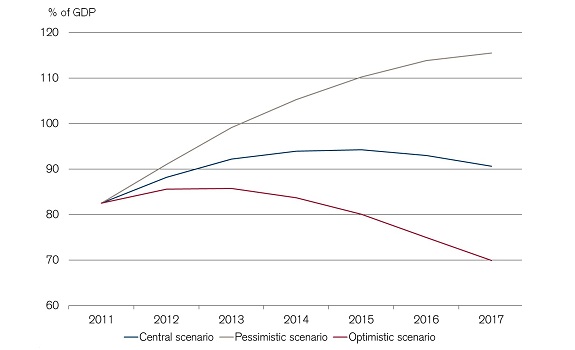

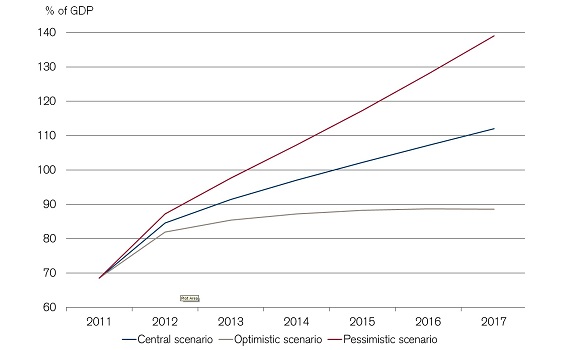

Italy, Portugal and Ireland Are Borderline Cases

- Portugal

Italy, Ireland and Portugal look like borderline cases. Among them, Portugal and Ireland are, of course, already under a bailout program by the so-called Troika, and both are small. Therefore, worries about a (further) debt crisis are not that great.

- Ireland

Ireland could benefit if some of the banks’ obligations that have been guaranteed by the government are taken over by the EFSF or ESM (as is planned in the case of the Spanish bank re-capitalization), or if the government can impose additional "haircuts" on the private holders of such assets (bank creditor "bail-ins"). Moreover, growth is resuming in Ireland, and the government has been able to regain access to capital markets.

- Italy

The Italian debt profile looks the best among the three countries because Italy is no longer running a primary fiscal deficit. What makes the debt vulnerable to some form of default, however, is quite simply its size. With such high debt Italy would be forced to run a primary surplus for a very extended period even if interest rates decline somewhat from current levels, and therefore some form of debt restructuring would provide a lot of relief and might be an attractive option for the government to choose.

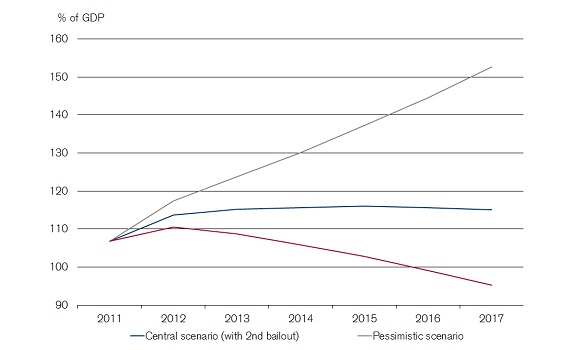

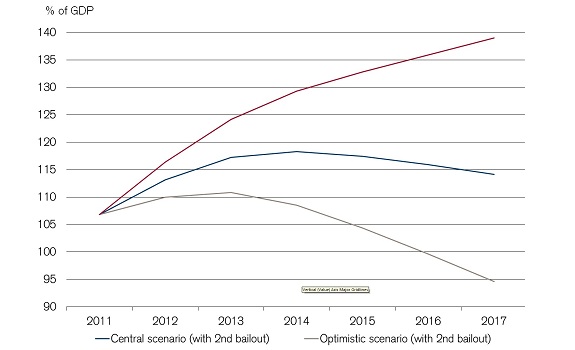

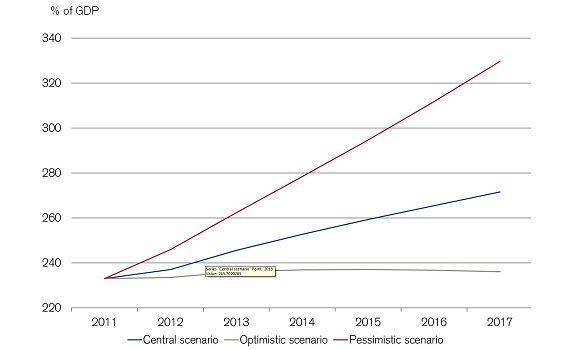

Spain’s Debt Trajectory Is Worrying

- Spain

The most worrying debt trajectory within the Eurozone is that for Spain. Even in the optimistic scenario the country will only achieve a stabilization of the debt ratio rather than a decline. The key problem are still high deficits, rather than the debt level itself which is lower than elsewhere. That said, the debt ratio would be higher if the Spanish government had to fund the recapitalization of its banks by itself. This is the reason for the EU-funded bank recapitalization program.

Two Rather Different "Big Elephants" in the Room

- US

The debt profiles for the two largest industrial countries in the world look far from comforting. While the US debt ratio should stabilize at around 110 percent of GDP in the base case, an economic downturn in the US or a rise in yields would make debt rise further. Like in the UK one could imagine an eventual currency-cum-fiscal crisis developing. That said, the status of the US dollar as the world’s reserve currency probably gives the Fed substantially more leeway to "monetize" debt without such a crisis.

- Japan

The Japanese debt ratio is on a seemingly unstoppable upward path unless growth turns out to be significantly higher than currently projected, or interest rates were still lower – which seems close to impossible. At some point, some form of debt restructuring may occur. More likely would be enhanced attempts at so-called financial repression (i.e. enhanced measures to entice domestic investors to hold JGBs). Inflating away debt appears more likely in the US than in the highly inflation-averse Japanese economy.

){kind=link}