Although revenues in FICC struggled, equity capital markets and advisory business were very strong in the first three quarters of 2015. M&A enjoyed a record phase, with the total value of announced transactions reaching $4.6 trillion in 2015, beating the $4.3 trillion peak seen in 2007, according to Thomson Reuters data cited Dec. 21 by the Financial Times.

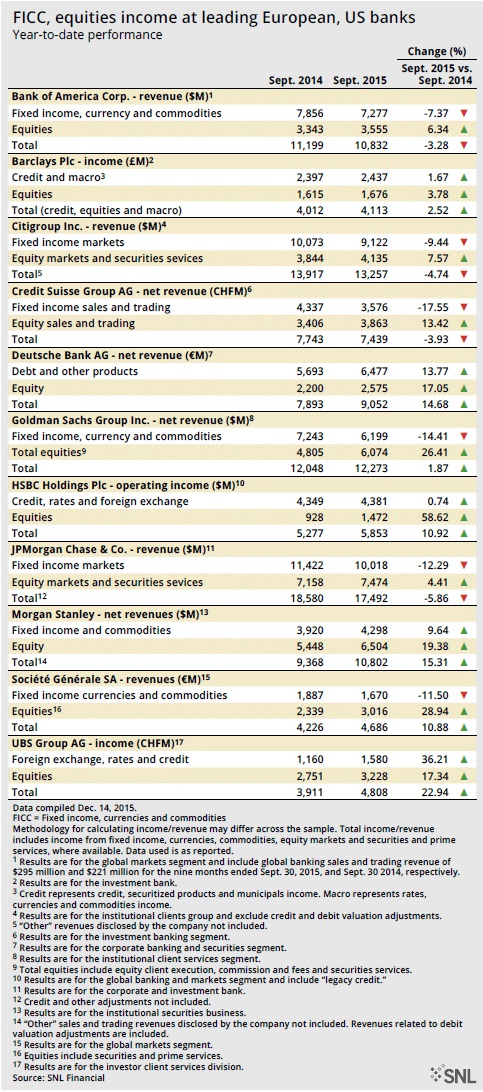

By contrast, the mixed picture within FICC has led to restructuring on both sides of the Atlantic. European banks fared somewhat better than their U.S. peers in the nine months to September. With the exception of Credit Suisse Group AG and Société Générale SA, the European banks in SNL Financial’s sample reported improved FICC revenue year over year, while only Morgan Stanley among the leading U.S. banks saw progress.

Quantitative easing helped European banks during 2015 while the long-awaited Fed raise hurt FICC revenue in the U.S.

By contrast, the wholesale equities business was very strong almost everywhere, bolstered by exceptional M&A markets. JPMorgan Chase & Co., Goldman Sachs Group Inc. and Morgan Stanley performed strongly in equities, ensuring that the foremost U.S. banks retained their leadership in investment banking revenues from FICC and equities.

Nevertheless, four of the six European banks, including Deutsche Bank AG, UBS Group AG and HSBC Holdings Plc, recorded double-digit year-over-year improvements in investment banking revenues during the first three quarters. This could come as a surprise given the talk of restructuring, although the quarterly figures do look far less promising than the nine-month equivalents.

through the first nine months of 2015, a trend they may well need to continue in (...)){kind=link}