Almost all of the performance of diversified portfolios, across both equities and fixed income, could be explained by factors

RISK FACTORS HELP US TO UNDERSTAND THE MARKET

Risk factors help explain systematic return patterns in the equity market and in other asset classes.

In traditional finance theory, such as the Capital Asset Pricing Model (CAPM) that was set out by Treynor, Sharpe and others in the 1960s, there is a single equity market risk premium, measured by beta. This risk premium compensates investors for holding equities rather than less risky assets. An investor can capture the equity market risk premium by holding the market portfolio of stocks.

But since CAPM was introduced researchers have put forward convincing evidence that there are other systematic sources of return in the equity markets than simply the market beta. These alternative return premia, or risk factors, include those relating to stocks’ size, their valuation, their momentum and their historical riskiness.

So now we can talk about “smart beta”: a combination of market beta and alternative risk premia representing these other factors.

Smart beta = market beta + alternative risk premia

Factor investing means the attempt to capture particular factor risk premia in a systematic way, for example by building a factor index and replicating it, or by constructing a portfolio that gives you exposure to a range of risk factors. The objective is to combine factors to enhance the long-term performance of portfolios.

FACTOR INVESTING IS A SUBSET OF SMART BETA

Factor investing, including factor indices, are part of the smart beta trend. But smart beta goes beyond factors.

Smart beta indices include all indices that depart from the traditional method of weighting components by their market capitalisation—companies’ individual stock market footprint.

Equally weighted, minimum variance indices, maximum Sharpe ratio and equal risk contribution indices are all part of smart beta. Many of these index approaches have factor “tilts” but they are a by-product of the index design.

In contrast, factor indices are those that are designed intentionally to capture a specific risk premium, such as value, size, low volatility, quality or momentum.

FACTORS AND ACTIVE MANAGEMENT

Factor investing has attracted a lot of interest because the past performance of traditional active managers seems to be due in a large extent to exposure to particular risk premia. There’s a lot of evidence that the average active manager has had long-standing exposure to particular factors, such as size and momentum.

For example, an influential study of the past performance of the Norwegian Government Pension Fund, published in 2009, showed that almost all of the performance of the fund’s external managers, across both equities and fixed income, could be explained by factor “tilts”.

This observation raises an important question. If a fund’s performance can be attributed in large part to a combination of return factors, why not seek to replicate the factors in a systematic and low-cost way? We are seeing a lot of interest in doing just this via smart beta indices and ETFs.

I don’t want to downplay the role of active investors altogether. This type of fund management will always play an important role. But active managers should be rewarded for taking truly idiosyncratic risks.

DON’T GET LOST IN THE FACTOR ZOO

In their influential 1992 paper, “Common Risk Factors in the Returns on Stocks and Bonds”, Eugene Fama and Kenneth French showed that, in addition to the market risk premium, two other factors relating to firms’ size and to value help to explain stock returns.

Since then, researchers have provided evidence for the existence of other factors, including momentum, low volatility and quality.

Momentum is a well-documented tendency for persistence in stocks’ price returns: stocks that have recently outperformed tend to continue to do so for some time. The low volatility factor is a return stream associated with less risky stocks and the quality factor represents the performance of a subset of more defensive stocks.

But statistical analysis can be and has been used to claim the existence of more and more factors. In fact John Cochrane, president of the American Finance Association, has recently referred to a “zoo” of factors. We recently counted around 250 in published academic papers, and their number has been increasing exponentially.

To avoid getting lost in the factor zoo—so as not to be misled by spurious correlations—we think that there should be solid empirical evidence for the existence of a factor and that there should also be some theoretical justification for its existence.

LYXOR’S FIVE-FACTOR FRAMEWORK

Lyxor’s equity market factor framework focuses on those alternative risk premia that have solid theoretical support and which are backed by empirical evidence. The framework has five components: in addition to the Fama- French factors of value and size we include momentum, low volatility and quality.

FACTOR APPROACHES WORK BEST REGIONALLY

Our research suggests that factor investment approaches work best in a regional context.

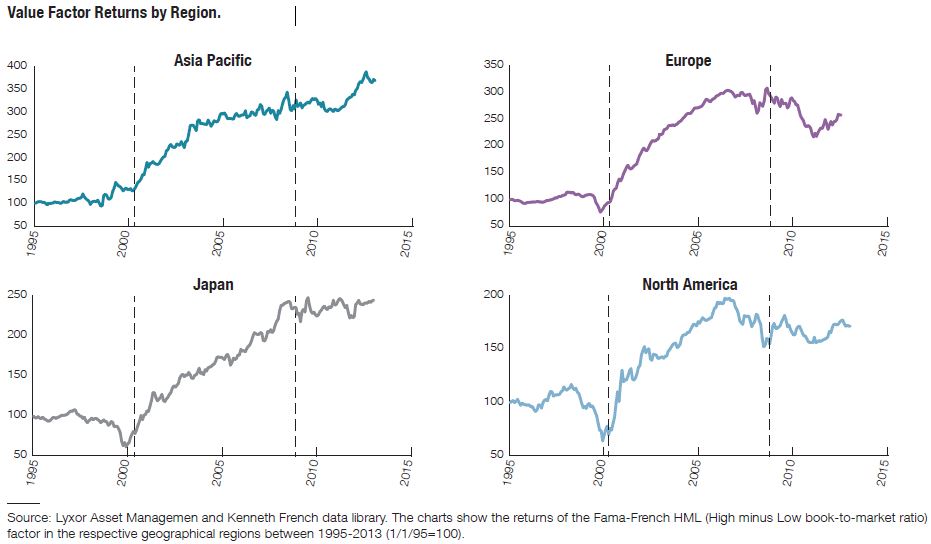

Value Factor Returns by Region.

Size Factor Returns by Region.

Over the period between 1995 and 2013 value factor investing produced positive relative returns in the US, Europe, Japan and Asia-Pacific, particularly in the period between the market peaks of 2000 and 2008. But, relative to local largecap stocks, small caps have done better in the US than in the other three regions. These differences in factor returns across regions probably reflect differences in market structure.

THE EXPLANATORY POWER OF FACTORS VARIES

When compared to traditional market beta, the ability of alternative factors like value and size to explain market returns is not fixed. Our research suggests that the ability of individual factors to explain stock returns probably moves in a 5-10 year cycle and, over time, reverts to the mean.

And it’s important to point out that the collective power of factors also varies. Since 2005, the combined impact of the Fama-French value and size factors on the US equity market was lower than in the 2000-2005 period, for example. Value and size stocks moved very much in unison during the period after the dot-com bubble burst.

These observations suggest that it makes sense to diversify across factors in a portfolio.

It’s important to point out that there is diversity a mongst factor a pproaches

THE VALUE FACTOR HAS TWO COMPONENTS

Within Lyxor’s factor framework, two factors are similar in that they both focus on stocks that trade at a valuation discount to the market portfolio: quality and value.

The quality factor highlights higher-quality, less cyclical, lowerleverage companies with above-average yields: these are defensive stocks that are likely to underperform in a rising market but which offer better protection in a downturn.

Our value factor focuses on distressed stocks, which are relatively risky but which offer the potential of large price gains in a recovery[1]. Examples of stocks in this category are BP after the 2010 Deepwater Horizon oil spill or Tesco after the 2014 disclosure that the company’s earnings had been overstated.

Société Générale calculates indices based on both these factor approaches, the SG Quality Income and the SG Value Beta indices. In our view these strategies are highly complementary for a portfolio investor.

FACTOR STRATEGIES MUST TAKE INTO ACCOUNT LIQUIDITY AND CAPACITY

Factor-based strategies are of interest to many types of investor, including the very largest pension and sovereign wealth funds.

But the potential implementation costs of a smart beta strategy of any size are important, particularly for the largest investors. Any investment portfolio that deviates from the market capitalisation-weighted index will generate some incremental costs as a result of additional turnover.

Research by Frazzini and others, published in 2012, suggests that value is the factor with the greatest potential investment capacity, followed by size and momentum.

It’s important to point out that there is diversity amongst factor approaches, something that may alleviate potential capacity constraints and concerns over crowding. For example the value factor indices published by the main index providers have subtle differences in their methodologies, so they don’t all hold the same stocks in the same proportions.

ALLOCATING EQUALLY ACROSS FACTORS CAN GIVE POWERFUL RESULTS

One of the principal reasons for the rising interest in factor investing is that diversifying across factors appears to give more powerful results than diversifying in the traditional way, by asset class, because of the lower correlations we observe between factors.

But how much of a portfolio should we allocate to each factor? When asset allocators consider how much of their portfolios to devote to equities and bonds they usually start with quite distinct return and risk forecasts for these two asset classes, leading to a variable equity/bond allocation for investors with different risk appetites. This type of forecasting exercise, which is not easy, is even more difficult for factor returns.

In the table and chart below we show the return and risk characteristics of five world factors and we compare them to the MSCI World Net Total Return Index. All the factor indices produce higher Sharpe ratios than the market portfolio, but note that the returns of the individual factor indices are within a range of just over 3% a year.

Factors need to be used consciously and carefully, with full knowledge of their characteristics

In fact a simple approach to factor allocation—equalweighting— has a lot of benefits. Our calculations show that for this period equal weighting produced better returns than other, more complex approaches to allocation, such as equal risk contribution, volatility weighting or minimum variance.

FACTORS SHOULD BE USED SENSIBLY

Factors can be a powerful tool to represent in a systematic way how the equity market’s returns are produced. They are having a major impact on how investing and asset allocation are done. But factors need to be used consciously and carefully, with full knowledge of their characteristics.

MOVING FROM THEORY TO PRACTICE

Investors may feel lost when confronted with 250 risk factors. They are required not only to understand the characteristics of each factor but also how to combine them in a portfolio. And to move from theory to practice, factor investing demands both technical expertise and experience. It’s also natural to question whether factors should be used as part of a strategic allocation or to take more tactical investment positions.

To help answer such questions, together with my co-author Zélia Cazalet I have recently written a paper entitled “Facts and Fantasies About Factor Investing”. We take a holistic view of risk factors, aiming to demonstrate certain factors’ persistence and suggesting how to allocate between them in portfolios.

){kind=link}