As the tenth anniversary of the Global Financial Crisis passed this month, our thoughts turned to the ongoing muted volatility in financial markets. The ‘Goldilocks’ conditions of improving growth without price pressures are something of a surprise, yet appear to be increasingly discounted in analysts’ and investors’ expectations. This situation may appear to be benign, but with valuations across many asset classes appearing full (not to mention negative term premia in bonds) potential risks are mounting.

Among the risks we see on the horizon are geo-politics, changes in central bank leadership, taper tantrums, and the dollar and emerging markets.

Political risk remains elevated in the United States, but had also been rising in Japan with polls indicating Prime Minister Shinz? Abe was falling out of favour with the Japanese electorate. Japan is a favoured equity allocation across our managed funds, so the possibility of Abe losing his position was of some concern to us. However, the panic appears to be over, at least for now. Improved economic growth data and a less hostile attitude from the public following recent scandals looks to have headed off any political crisis for Abe. Moreover, two recent cabinet appointments have been particularly encouraging, with two potential opponents of Abe given prominent positions within his Liberal Democratic Party, meaning neither are likely to pose a challenge to the Prime Minister. Our base case is that Abe survives this scare and political stability remains until at least 2021.

A change in central bank leadership could challenge the easy monetary policy conditions that have underpinned risk assets in recent years, threatening the ‘lower for longer’ rate environment. In Europe, Mario Draghi’s term ends in October 2019, but he could bid for the Italian leadership next year; while in the US Janet Yellen’s tenure ends in January 2018 – although her position is, to a degree, dependent on President Trump. In Japan, Bank of Japan governor Haruhiko Kuroda’s term ends in April and he could be replaced by a Bank of Japan traditionalist who may be swift to normalise monetary policy. We are mindful that accelerated central bank normalisation could have serious repercussions for global risk assets.

Taper tantrums are possible in Europe as the European Central Bank turns less accommodative, especially as the ECB is the marginal buyer of bunds: Mario Draghi has talked of a strengthening and broadening recovery in the euro area and has signalled further tapering of his QE programme as we go into 2018. Ditto with the Fed, where term premia in US rates has turned negative once again. With share buybacks having slowed dramatically, equities may be vulnerable – although we do note that they price in greater risk premia than the likes of corporate bonds. The dollar has been weak of late, which has helped emerging market rates in particular and risk assets more broadly. But if the dollar reverses course, there could be meaningful impacts on other asset markets.

We have also been looking at the health of emerging markets excluding Asia, where we have a neutral allocation, noting that countries that were hit hard by the taper tantrum of 2013 – such as Brazil, Mexico, Russia and South Africa – have undertaken meaningful reforms, with higher quality growth as a result. Russia remains intimately linked to the price of oil, but oil at $50 a barrel is seen as manageable for both Russia’s economy and oil companies. South Africa is probably the weakest spot in EM ex-Asia, with soggy growth, growing political risk and low real interest rates limiting the scope for policy stimulus. While in Mexico, weakness around the US elections provided an opportunity to build into well-supported companies, against a backdrop of strong consumption prospects that may be helped by policy easing as inflation comes off the boil. Corporate sentiment in Mexico is positive, not withstanding the evolution of US trade policy and timing of further rises in US interest rates.

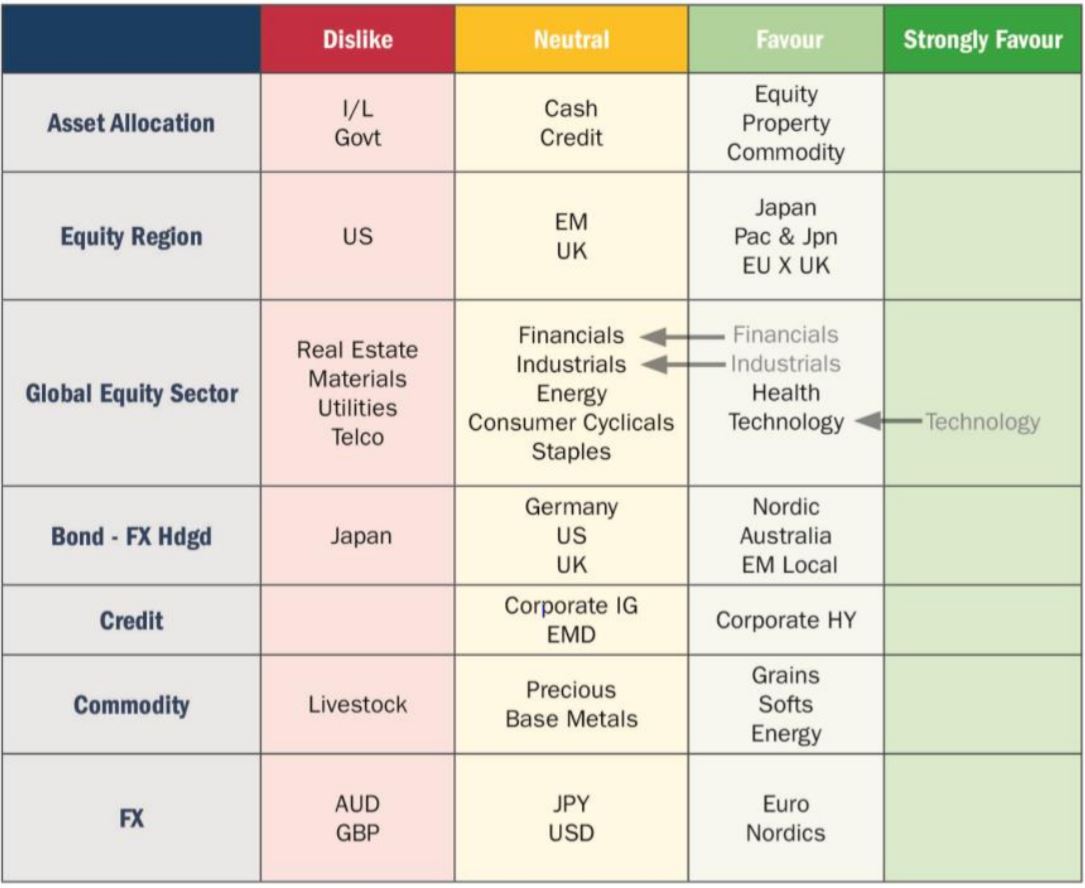

Taking all of the above into consideration, we have made no changes to our broad asset allocation this month. However, our global equities team has downgraded three sectors: industrials and financials have moved to neutral from favour, while technology has moved from strongly favour to favour.

We remain positive on technology, but the valuations were such that we felt it was prudent to clip back our exposure to the sector.

Asset allocation snapshot

- Source: Columbia Threadneedle Investments, as at 31 August 2017.

){kind=link}