Global equities are by no means cheap, but they are reasonably valued. Considering the scale of the pandemic they performed surprisingly strongly in 2020, and we think they will continue to do well in 2021. However, we expect the market recovery to broaden out across a broader range of sectors compared to the past 12 months.

Technology stocks - no sign of a bubble

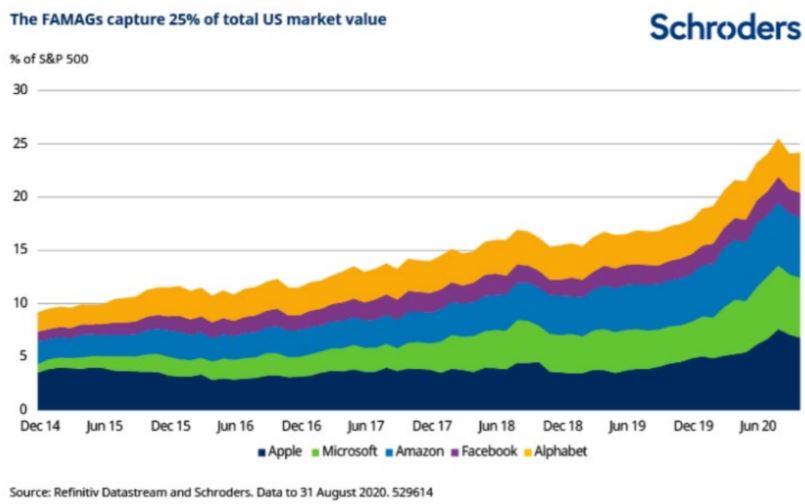

The market rally in 2020 was led by a fairly narrow range of tech stocks, in particular Amazon, Apple, Microsoft, Facebook and Alphabet (sometimes known as the FAMAGs).

This was primarily due to the justifiable perception that these companies are dominant in their respective fields, have high rates of long-term revenue and earnings growth, and have been beneficiaries of forced changes to work, social and shopping practices during lockdown. In effect these companies were the “lockdown leaders” (see chart below).

The mega-cap technology platforms now account for a quarter of the entire S&P 500 market capitalisation (these stocks eclipsed 25% of the index on August 21, 2020 and remained so for the rest of the month).

Inevitably this degree of concentration has drawn comparisons with the 1999 “internet bubble”. However, we believe this view is misplaced. Firstly, the tech bubble in 1999 was driven by investor exuberance around anything tech-related, regardless of profits or even revenue. Whereas, the technology sector in 2020, and particularly the largest platforms, have delivered exceptional revenue and earnings growth which we will believe will likely continue into 2021 and beyond.

Secondly, looking back in history the current degree of concentration in the equity market is not unusual. In the 1960s and 70s the S&P500 was dominated by a similarly small number of very large companies such as AT&T, Exxon, GE and GM.

Covid-19 has clearly accelerated the adoption of new technologies such as e-commerce and remote working. These changes in corporate and consumer behaviour will likely continue after the pandemic. Corporates have already changed their working practices and “fast-tracked” changes that were already underway – such as a transition to the Cloud or rapid adoption of automation – and will likely accelerate these plans further as the benefits become apparent. E-commerce has proven itself during the pandemic across a wide range of areas. In many parts of the world, e-commerce penetration levels are still relatively low, providing potential for continued and substantial growth.

In short, the “technological transformation” already underway well before the pandemic has simply been accelerated by Covid19.

Technology will continue to provide a fertile hunting ground for investors in the coming years. The biggest risk to the sector is likely to come from regulation (see below), rather than any rapid diminishment in the underlying growth rate.

Market recovery set to broaden out

During 2020, investors flocked to safety amid the global uncertainty, with growth and defensiveness being a key part of the

equation (as with the technology names). However, the announcements during November that several effective Covid-19

vaccines have been developed gave investors an incentive to think about “normalisation” and economic recovery in 2021 and

2022. The chart below shows the returns from global stock markets in the 11 months to November 30.

Investors have begun to look at the potential for revenue and earnings growth in many “out-of-favour” areas that suffered during the pandemic. The most obvious of these are those that were effectively shut-down, such as hotels, restaurants, leisure enterprises and travel companies. It seems highly plausible that when the recovery, takes hold many of these businesses will experience a sharp rebound.

In addition, expectations in cyclical sectors such as energy, materials or industrials are low and merit attention. It is clear that there are major structural challenges (such as the energy transition) that will continue to significantly affect many companies in these sectors in the future.

However, we believe that some companies will continue to adapt and prosper, and that a sustained pick-up in global demand in 2021 will drive significant revenue and profit growth.

This will certainly be the case in many parts of the industrial sector in our view, as operating leverage (the sensitivity of profitability to a sales improvement, with a given level of fixed cost) will be substantial in many cases around the world.

We expect to see a significant broadening of the market in 2021. Technology can still do well, but some of the un-loved areas may do better still. We don’t see it being as simple as buying the cheap sectors and selling the expensive ones since, to quote the great Sage of Omaha, “Price is what you pay, Value is what you get”.

Not all cheap oil, commodity or industrial companies offer good value, and neither do all banks or insurance companies. There will likely be substantial dispersion in every sector as the global economy transitions in 2021. As such stock selection remains highly relevant, in our view.

Valuations of global equities remain (relatively) attractive, especially outside the US

Global equities are, in aggregate, reasonably valued and in line with their long-term averages on a forward basis. The global dividend yield also remains materially above the bond yield, supporting the relative case for equities over Treasuries.

As an asset class, we believe they will continue to do well in 2021 as the recovery broadens out. It is worth noting though that after a period of massive outperformance by the US versus the rest of the world (around 8% annualised over the last 10 years), the US is now trading at a premium to its long-term normalised earnings valuation. Meanwhile, the rest of the world is now trading at a substantial discount.

European and Japanese profits are expected to rebound the most in 2021 and possibly in 2022 as well. The Chinese economy is already recovering, driving a powerful recovery dynamic across Asia as a whole. The US will remain a highly quality defensive equity market with by far the greatest depth and liquidity of any global market. However, while the flight to safety has created a flow toward the US, as the recovery takes hold we believe this may partly reverse, and capital will begin to flow elsewhere.

New president, new agenda

At the time of writing it is clear that there will be a Democrat president and a Democrat Congress. It is worth noting that, contrary to popular opinion, Democratic administrations have usually presided over higher stock market returns than their Republican equivalents. But there is no question that the Democrat agenda will be markedly different to that of the previous administration.

Under Joe Biden we expect a shift toward liberal values: greater equality, higher minimum wages, improved social support (especially healthcare coverage) and proper environmental controls. A number of these policy initiatives could, if implemented, materially impact the outlook for parts of the US economy. For example, stricter drug pricing controls could significantly affect the US healthcare sector, while the introduction of a $15 mandatory minimum wage would greatly impact all areas of the service sector.

The Department of Justice investigation into Google, announced in the late summer, indicates that scrutiny of the large internet platforms is increasing. The Democrats are likely to accelerate this process once in power. However, the Democrat’s failure to secure control of the US Senate will limit Biden’s ability to increase taxes, specifically the corporate tax rate which would rise to 28% and take 8-12% off S&P earnings if passed. Other policy initiatives, such as healthcare reform, may also struggle to make it through the upper house.

From a foreign policy standpoint, a Biden administration is likely to maintain a tough stance on dealings with China, but will restore relations with Europe and Asia. In general, we would expect the political backdrop under the Democrats to be less confrontational, more constructive, and ultimately more in line with most major trading partners.

Thematic investing will be even more relevant post-Covid

Taking a step back from the pain of Covid-19, the noise of politics, and the uncertainties around the trajectory of economic recovery, most of us would agree that there are a small number of undeniable and substantial trends that have the potential to materially affect the way we live, work, socialise and interact in the future.

Some of these trends (often referred to as “mega-trends”) are not new: climate change, healthcare innovation, urbanisation, automation and digitalisation have been relevant themes for many years now.

Others, such as sustainability, food & water provision and changing lifestyles are emerging as important and urgent areas of change, driven by population growth and rising consumerism in emerging markets.

The common denominators across all the megatrends are two-fold. Firstly, they are all becoming rapidly more relevant as humanity consumes a greater and greater proportion of the Earth’s resources. Secondly, the challenge of these trends is being met by rapidly accelerating innovation that is driving a technological transformation across virtually every sector and industry group.

It is this innovation dynamic that we believe creates a strong rationale for a themes-based investment approach. If we are right about the themes, and consistent in our approach toward assessing them, then in all likelihood having exposure to at least one of them could be highly incremental to a more traditional index-based equity portfolio. Given that many of the themes encompass different sectors and industries, there is also a high probability that allocating to them can enhance the overall risk/return profile of a portfolio over time.

Looking towards the new green industrial revolution

As an example of the rapidly increasing importance of certain key themes, global climate change is a case in point. In order to stabilise global temperatures within the +2 degrees C limit defined as “safe” by the Intergovernmental Panel on Climate Change (IPCC), spending on greenhouse gas mitigation will have to rise to at least $2 trillion a year over the next 10 years. That cost will have to be borne by governments, consumers and of course, companies.

Green policy momentum is now building rapidly, led by the European Union with ambitious targets to reduce emissions by 2030, and the EU Green Deal channelling at least a quarter of the €750 billion recovery package towards decarbonisation initiatives. The EU has committed to becoming a net zero carbon economy by 2050, and China has also committed to achieving that goal by 2060.

The UK government has committed to a target to generate enough offshore wind to power every home in the UK together. It’s also announced a ban on new petrol and diesel cars and vans from 2030, five years earlier than previous targets.

Under Biden, it is likely that the US will dramatically reverse its recent course and initiate a Green Deal similar to the European model. Biden has already pledged to recommit the country to the Paris Agreement and to a net-zero emissions reduction target by 2050.

The opportunity for growth is vast and still under-appreciated in our view. Momentum behind the transition to a low carbon economy is accelerating rapidly now. The most crucial driver has been the dramatic improvement in the competitiveness of clean energy technologies, to the point where they require little or no subsidy to compete with fossil fuels. Investments to displace combustion engine vehicles and fossil fuel power generation are now ramping rapidly, and we expect the next five years to be a critical inflection point in that transition.

We continue to believe the automotive sector is set for very rapid and fundamental change, with an accelerated adoption of electric vehicles (EV), taking EV penetration up towards 50% of global new car sales in 10 years time, and eventually close to 100%.

More broadly, the transition to a green economy will offer tremendous opportunities for investors as investment builds and adoption rates surprise on the upside. The same is true for other key trends where innovation is rising.

{kind=link}