Historically, it has delivered strong returns, causing headaches for advocates of the Efficient Markets Hypothesis (“EMH”). Its persistence breaks one fundamental rule of the EMH: if past stock prices help predict future returns, they do not fully reflect all available information. Research on the causes of Momentum persistence was popularized by Hong and Stein in 1999 (“A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets”).

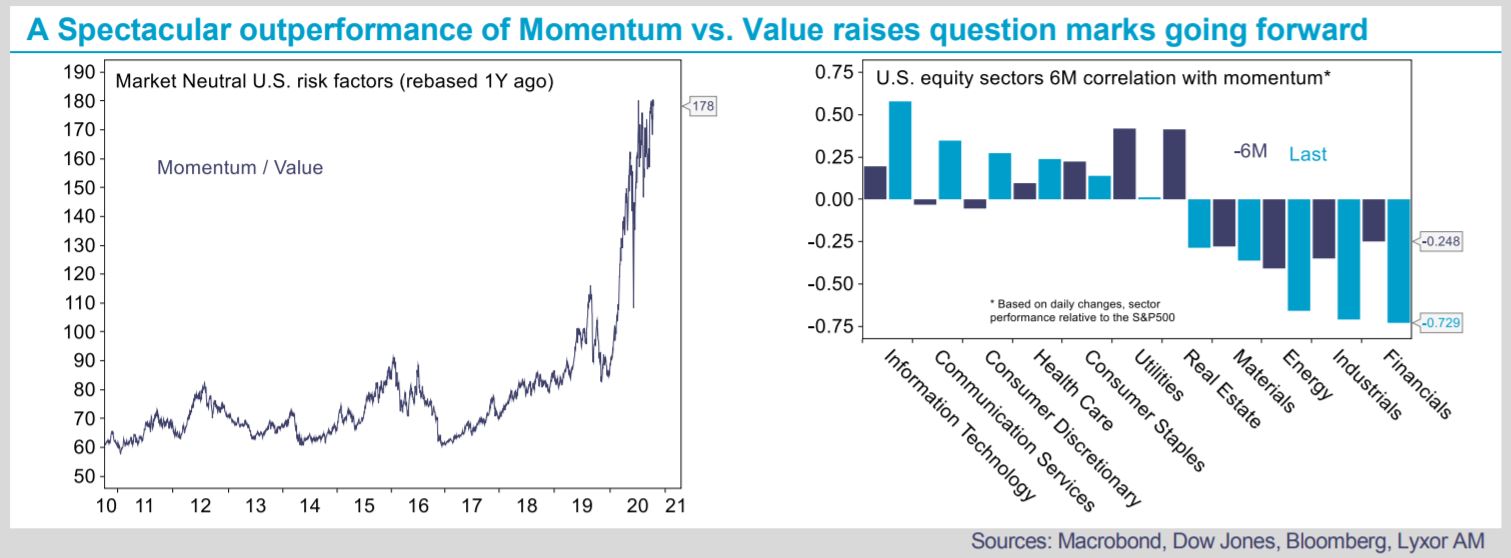

In recent months, the Momentum risk factor has delivered strong returns, particularly in the U.S. (+7.7% in Q3- 2020). It is currently long sectors such as IT, Consumer Discretionary, and a number of defensive sectors (i.e. Communication Services, Consumer Staples, Health Care) reflecting future growth uncertainty.

In parallel, it is negatively correlated to Financials and Energy returns. Looking at its correlation to other risk factors, we see that Momentum has been tantamount to Low Beta for some time. It is also increasingly vulnerable to rises in bond yields. We estimate that a +10bps rise in Treasury yields would drag Momentum’s performance by -2.4%.

The above suggests that Momentum is vulnerable to richly valued sovereign bonds but at the same time is protected by asset purchases from central banks. The latter have de facto anchored bond yields at current levels. A sharp and sudden rebound in cyclical and/ or value stocks (i.e. Industrials, Materials, Energy, Financials, etc.) would be painful but seems unlikely due to uncertain economic prospects amid the COVID-19 resurgence. Yet, the relative performance of Momentum vs. Value has been so spectacular in the past year that we raise caution going forward.

Factor rotations tend to cause substantial damage to some alternative strategies. CTAs are by construction exposed to the Momentum risk factor but from a cross-asset perspective. A vast amount of L/S Equity strategies, especially systematic Market Neutral ones are exposed to Momentum. Our stance on such strategies is currently defensive. Finally, Event-Driven is among the few strategies that does not bear Momentum risk.

){kind=link}