Momentum is unloved: being a good follower is rarely seen as a strength, and few asset managers would brag about using momentum as an investment factor, even though they know that ‘the trend is your friend’. Part of this unpopularity comes from the fact that momentum is a purely behavioural factor: only human irrationality can explain it, and we are not at ease with our own shortfalls.

However, there is humility in accepting that ‘others’ may have useful information on stocks and that the herding effect of investors can sometimes be considered useful. Here are a few pointers on how best to use momentum.

The data needed to assess momentum is, very simply, the history of the price of each stock

In this respect, momentum is unlike factors such as value or quality that require fundamental data. However, momentum can be a tenuous factor. If you consider too short a horizon, perhaps one week, you could meet its opposite factor, the short-term reversal. Equally, if you look at data over too long a period, you could come up against a long-term reversal. So you have to choose the right horizon, typically one year, to see the momentum effect as it is described in academic research.

The stock price is only one of the measures of the true underlying effect, which is about the changing sentiment towards a given company.

Etienne Vincent, Head of Global Quantitative Management, THEAM

Etienne Vincent, Head of Global Quantitative Management, THEAM

Yet, momentum is not really on the stock price

The stock price is only one of the measures of the true underlying effect, which is about the changing sentiment towards a given company. This change in sentiment can be measured at different ‘levels’ of interested parties: The most knowledgeable group about the company is its board members, who have to disclose their buys and sells, at least in the US. Since this measure is difficult to obtain in markets outside the US, we do not use this indicator.

The second largest group providing a sentiment measure comprises the analysts who follow the stock

Any revision to their earnings estimate suggests a change in their sentiment on the company, and we often use this change as a momentum indicator. The third, even larger, group is the investors who drive the stock price up and down. This is the price momentum, which we also use. There is actually an even larger group, which we do not use: the company’s customers, whose sentiment can be assessed by measuring the popularity of the company’s products, for instance based on the tone expressed in Twitter feeds.

As humans, we can feel ill-at-ease with using such measures, because they show that there is herding instinct behind our decisions: we prefer not to be alone in taking a given risk, whether buying or selling. In traditional economical models, it is very difficult to account for this momentum effect, as information is supposed to disseminate instantly. However, in psychology, the herding effect is well documented and can be traced to a survival need: copying one’s peer is a much more efficient way to survive than venturing alone down new paths.

Etienne Vincent, Head of Global Quantitative Management, THEAM

Traditionally, however, momentum at the stock level is measured ignoring by how much the price of a given stock tends to move in tandem with equity market indices. Momentum strategies relying on those traditional measures of momentum tend to suffer quite heavily from changes in the direction of markets.

In turn, idiosyncratic stock momentum measures how much the price of a stock moves after removing the momentum component due to the stock price simply moving along with equity market indices. That is, by how much the price of a stock moves because of information relating to the specific company in question and not because of information that affects all stocks. Strategies based on idiosyncratic stock momentum ignore the noise created by what can impact all stocks simultaneously and tend to generate higher returns. This is why our momentum strategy is based on idiosyncratic momentum for each stock in a given sector.

Of course, it is easy to see the absurdity of momentum in times of asset bubbles

Pure momentum investors tend to be ‘the last fools to buy’ before the bubble bursts. In general, momentum also leads to high portfolio turn-over, which is costly. Yet returns can still be captured by following the crowd at an appropriate pace, even if we don’t like doing so.

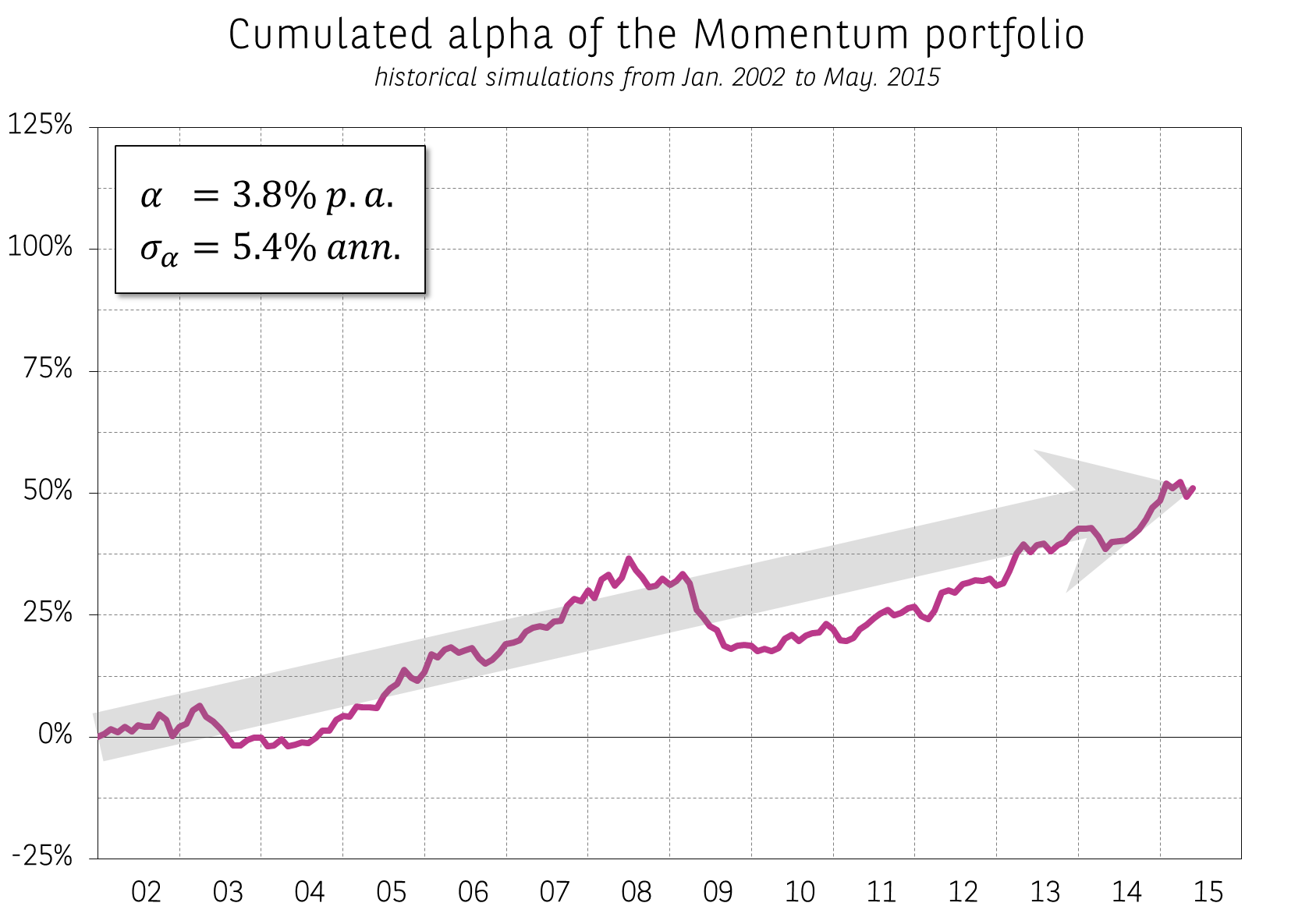

Exhibit 1: historical simulations of a long-short portfolio based on MSCI World Universe with stocks ranked by a proprietary measure of momentum

- Source: MSCI, Exshare

){kind=link}