A spectacular momentum crash unfolded since late August, caused by the bounce back in sovereign bond yields. Within equity markets, value stocks experienced an impressive rebound while momentum stocks fell strikingly. Critically, the rise in bond yields and the rebound in value stocks reflect improved growth expectations, which contradicts the mood among economic forecasters. Meanwhile, some market commentators have established a parallel between recent events and the “quant quake” of August 2007, which marked the debut of the global financial crisis. However, the key difference is that in the summer of 2007, bond yields and value stocks reached a peak, not a bottom, before initiating a dramatic and long-lasting descent.

Momentum strategies in a long/short format buy assets whose price had gone up in recent months and sell assets whose price has gone down during the same period. Trend following CTAs implement that strategy in a multi asset framework while several L/S Equity strategies implement it at the single stock level. Both strategies suffered a blow so far in September. The Lyxor CTA Peer Group was down -3.6% last week, and the Market Neutral L/S Equity Peer group was down -0.4%. Interestingly, Directional L/S Equity strategies were not significantly impacted by the momentum/value reversal, contrary to their Market Neutral peers. At the level of individual strategies, some CTAs were down in a range of -5/-7% in a single week. These underperforming strategies were nonetheless those that outperformed on a year-to-date basis. Despite the drawdown, they are still up in a range of +15/+20% since the beginning of the year. Within our peer group of 31 Market Neutral L/S strategies, the worst performer was down almost -7%.

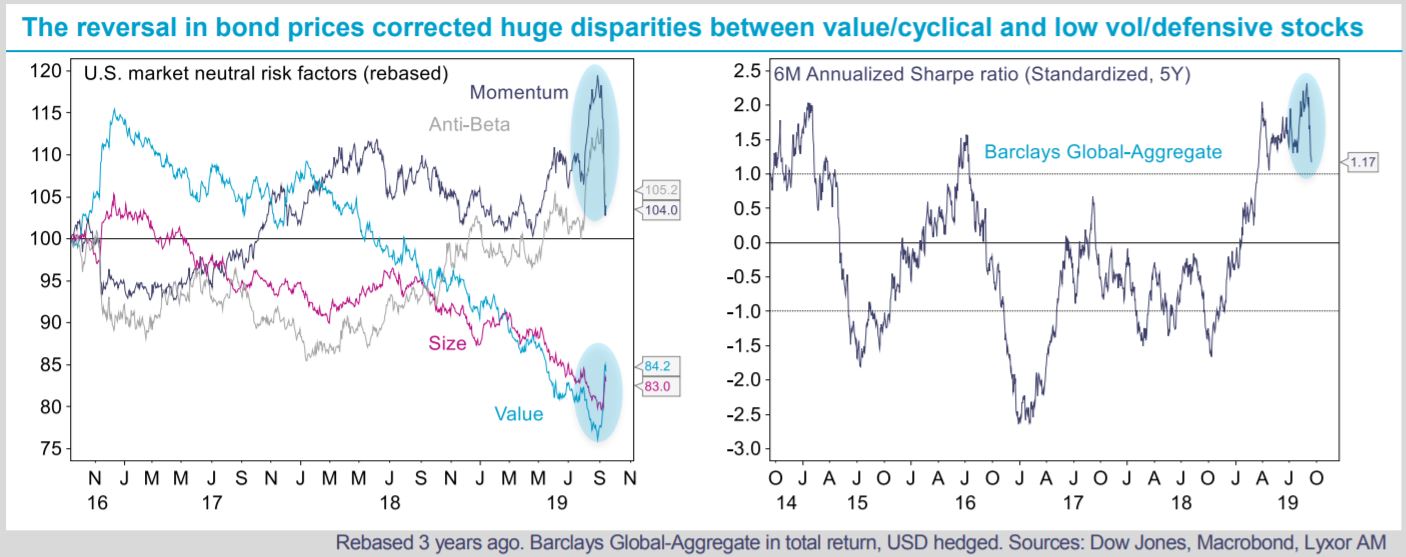

Momentum corrections happened regularly last year but the violence of the current event mirrors the exceptional bond market rally over the past 18 months.

It caused significant distortions in stock markets, fueling low volatility/ defensive stocks. However, these shocks tend to be short term. We do not expect it to be long lasting and stick to our views, i.e. Neutral CTAs and Overweight Market Neutral L/S Equity. Finally, some strategies such as Global Macro benefitted from recent market movements, up +0.9% last week, while others such as Event Driven and L/S Credit, were unchanged.

){kind=link}