With risk assets back to record highs, markets are currently looking for the next catalyst that would push equities higher. But with the Fed potentially signaling a looming reduction in asset purchases at the next FOMC meeting on June 16, it seems wise to remove some risk off in portfolios from a tactical standpoint. Yet, alternatives are scarce, with bonds potentially hampered by rising inflation expectations, and cash yielding zero or negative interest rates.

In this context, we have reiterated in recent months the attractiveness of some hedge fund strategies. Among them, our stance on CTAs and Event-Driven is the most constructive. CTAs are currently long equities and commodities, and their exposure to fixed income is virtually zero or negative.

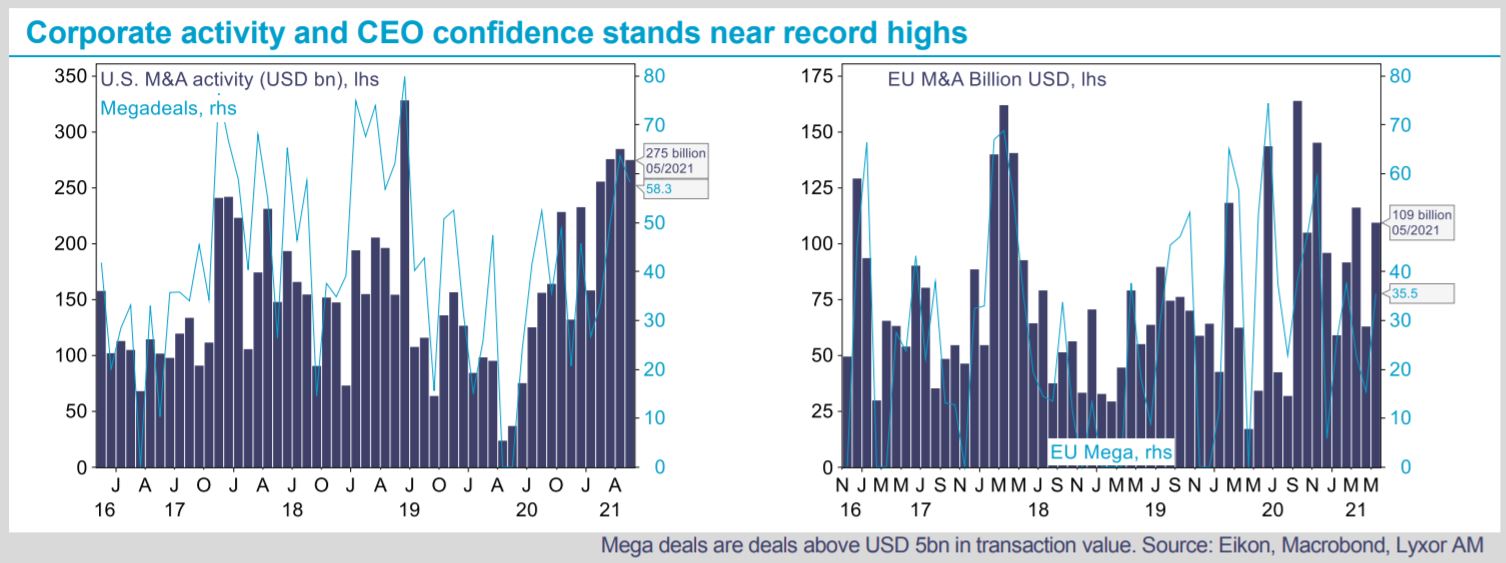

We believe the strategy is attractive, all the more so since its asset mix brings some diversification versus traditional asset classes. Concurrently, Event-Driven has benefitted and should continue to benefit from unprecedented levels of corporate activity. Global M&A volumes have attained more than USD 350bn in May, the fourth consecutive month with volumes above USD 300bn. In parallel, mega deals are back in the U.S. The share of announced deals above USD 5bn represented more than 50% of overall volumes for the third month in a row in May. Cyclical sectors still experience the largest volumes, such as Technology, Consumer Cyclicals, Financials, and Industrials. Amongst defensive sectors, M&A activity in the Health Care sector also remains strong in the U.S. and Europe. Recent deal announcements involve Discovery acquiring WarnerMedia for USD 43bn and the USD 8.45bn planned acquisition of MGM by Amazon, both in the media sector. In Europe, the EUR 30bn acquisition of Deutsche Wohnen by Vonovia in the real estate sector also suggest mega mergers have some potential to lift corporate activity in Europe.

Our stance on Merger Arbitrage is highly constructive. Elevated M&A volumes, along with attractive deal spreads which stand close to 6%, should continue to be supportive. With CEO confidence near record highs and low interest rates still in place, the M&A frenzy is set to continue.

Finally, after the sharp appreciation of risk assets, we believe

low beta strategies are increasingly attractive and upgrade the strategy to Overweight from Neutral.

){kind=link}