A combination of negative factors, from US economic uncertainty to the Volkswagen scandal, caused equities to experience their worst period since the Eurozone crisis of 2011, while bonds and gold – which normally rise in value during difficult periods – also declined.

However, this is an extremely rare event, occurring for the first time in two decades, and does not symbolize the ‘Return to Normalization’ that Robeco has forecast in its 2016-2020 Expected Returns, Daalder says. Instead, “we continue to believe that at times there are good returns to be made, and do not expect the all-negative return to become the ‘new normal’ just yet. The main risk to this scenario is that the world economy becomes tangled up in a recession, but the odds of that happening remain small.”

Five trigger points

Daalder identifies five main trigger points for the market volatility that has dogged investors over the past half-year, four of which are inter-related:

- Uncertainty over future US Federal Reserve policy following its 17 September decision not to raise rates, raising doubts about the underlying strength of the US economy, partly due to…

- Weaker data for US industrial production, which has been under pressure for two straight quarters now, mainly because of negative growth in the mining sector (including shale), which has led to…

- Uncertainty over the financial stability of various oil and mining companies following the strong declines in oil and commodity prices this year, plus also…

- Deteriorating cash flow in the oil-producing countries, which has caused the Saudis for example to withdraw USD 50-70 billion from global asset managers over the past six months in order to fund their rising deficit. Meanwhile…

- The Volkswagen scandal shocked investors, and although it did not lead to a market-wide sell-off, it undoubtedly had a negative impact on overall investor sentiment, particularly since it involved a previously squeaky clean industrial titan.

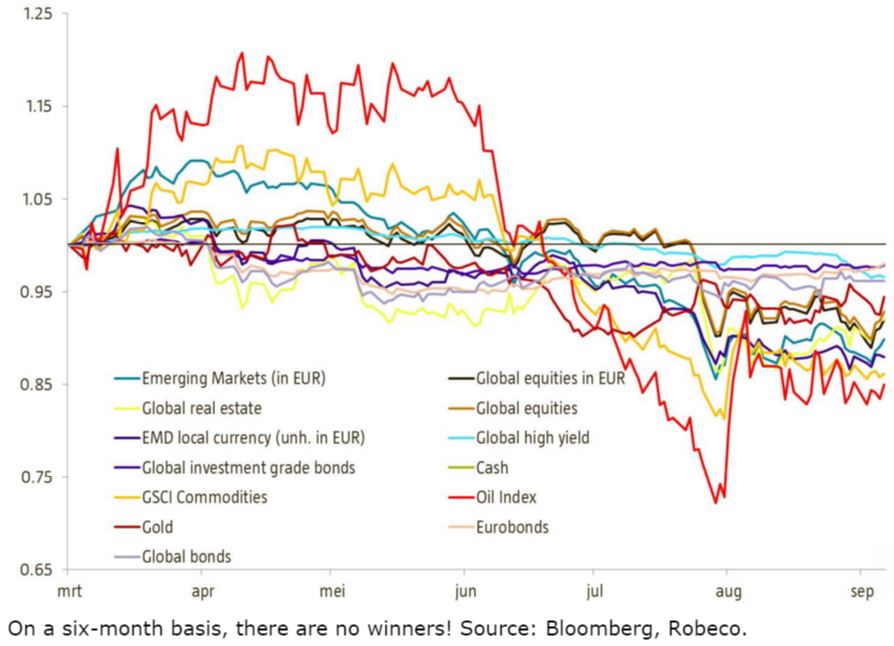

“The logical consequence of putting more risk and uncertainty into the financial markets is that risky assets underperform, so it should come as no surprise that equities and high yield/credit markets became under pressure in the recent turmoil,” says Daalder.

“What is remarkable though is that there appears to have been no hiding from the selling pressure this time round. On a six-month time horizon, none of the major asset classes (excluding cash, of course) managed to put in a positive return.”

There has only been one verifiable occasion in which this has happened before, at the beginning of 1995, after the Fed reached the end of a tightening cycle and both equity and bond values plunged, creating havoc on financial markets around the world. “Maybe if we had data going back to the gruesome 1970s, when stagflation was the name of the game, we would end up with more of these all-lose periods,” says Daalder. “But given that the explosion in oil prices drove the financial markets back then, it is clear that there was at least one asset class that was doing fine. So we are looking at a rare event, at least based on the data that we have.”

So what now for investors?

“The question that this raises is whether it is just pure bad luck, or whether this is the ‘new normal’, and something we should be expecting more often moving forward,” he says. “It should firstly be stressed that this six-month timeframe is of course pretty randomly chosen. Had we used a nine-month timeframe, we would still have seen a positive result for real estate, for example.”

“Added to this is the fact that the loss in the US bond market was a pretty close call to begin with: following a number of weak macro releases, US 10-year yields are trading below the 2% again, which means that six-month returns have been pushed back in the black. So it was really just a temporary dip.”

Overweights in equities and HY bonds

Daalder warns though such temporary dips may recur. “If we look at the outlook for the various asset classes for the next five years, we expect markedly lower returns, either compared to the recent past, or the steady state long-term average,” he says. “By definition, this raises the odds that numerous – if not all – asset classes yield a negative return on any given timeframe. This does not mean that we are considering putting all our money into cash though. There will still be periods where there is good money to be made in the various assets.”

He says Robeco Investment Solutions, which runs a multi-asset portfolio, actually increased its allocation to equities during the recent sell-off, “as we do not believe that a recession will hit the US, or that China will experience a hard landing. We have also raised our overweight in high yield bonds, as the recent widening of the spreads has now created a much more interesting buying opportunity.”

{kind=link}