Low Inflation: Dry Powder?

The declining rate of global growth continues to preoccupy investors concerned about the impact on markets. At issue is the fear that the world’s currently subdued rate of inflation is a symptom of flagging demand and future difficulties in building national wealth, especially in smaller, less developed economies.

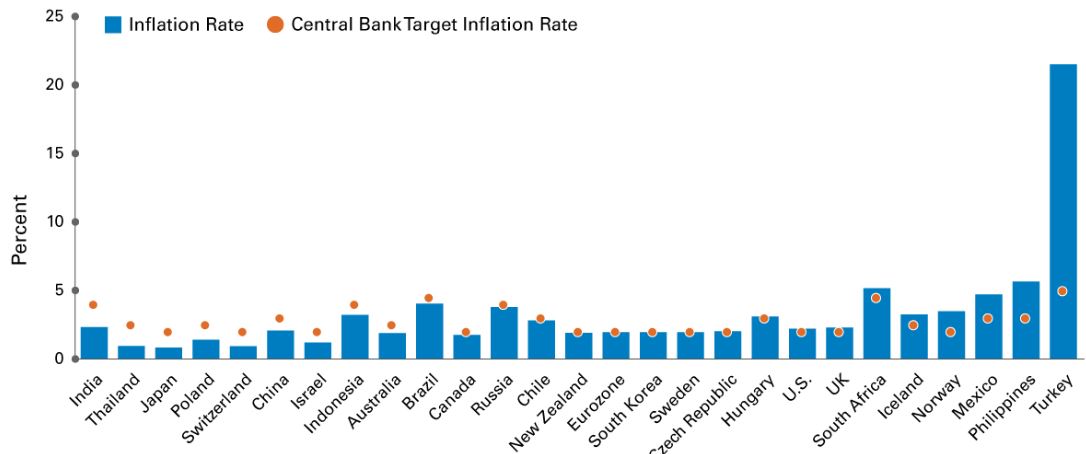

But there’s another way of looking at low inflation – as evidence of policy successes on the part of countries’ central banks. – a point that managers at Brandywine Global see as particularly compelling in emerging markets (EM) economies. Not only do many of these countries have inflation rates below their central bank targets, but inflation is also low in absolute terms, with many below 4% to 5%.

The chart below (from Tailwind in 2019: Global Inflation) makes this point clearly by showing key economies ranked by inflation shortfall vs. their own central banks’ targets. That list of “shortfall” countries includes not only giants like India, China, Japan, Brazil, the U.S. and the Eurozone, but also Thailand, Poland, Chile, Sweden and Hungary.

Inflation Target Shortfalls: Room for Maneuver for Central Banks

Central bank successes in controlling inflation are a tailwind for global growth

- Chart courtesy of Brandywine Global. Source: Brandywine Global, as of 30 November 2018. Past performance is no guarantee of future results. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

Even where inflation has shot upward, as in Mexico and Turkey, central banks have eventually stepped in with inflation-busting rate reductions and other deflationary policies, rather than riding the wave to oblivion, as may be taking place in Venezuela.

Brandywine’s conclusion is that renewed global central bank discipline could potentially help counteract the planned withdrawal of liquidity from the global economy by the Federal Reserve. Once the FOMC meets during the week of February 28th and reveals its members’ projections for future hikes, it could become clearer how much of that discipline will be needed in the year ahead.

On the rise: Short-term U.S. credit

In sectors not overburdened with good news, improved returns for U.S. credit since the start of 2019 have been welcome. As measured by their respective indexes, U.S. Investment Grade, High Yield and even leveraged loans rose 1.37%, 3.76% and 2.51% respectively[1]. However, the rally truly began on “Boxing Day” (Dec. 26), with the indexes up 1.81%, 4.38% and 2.23% since that date.

While noteworthy, these mini-rallies in 2019 still left Investment Grade underwater by about ‑0.72% since the beginning of 2018. High Yield did better over the interval, up 1.57%, while Leveraged Loans were ahead by 2.96% for the period.

Like much else in the U.S. bond markets, credit for the recent gains was laid at the feet of Fed Chair Powell and other members of the FOMC, whose markedly dovish speeches at the end of 2018 calmed fears of a potentially calamitous policy error fed by an irrationally exuberant Committee. By the end of Chair Powell’s press conference on January 30, it may become clearer whether markets got this one right, at least in the short run.

On the slide: Fed hike expectations

There are still a few members of the Fed’s Open Market Committee who are on record forecasting as many as three rate hikes in 2019 – at least according to the Fed’s December “dot plot”.

Financial markets, however, are priced as if the odds of even a single hike this year are slim-to-none. Indeed, the former president of the Federal Reserve Bank of Minneapolis from 2009 to 2015, Narayana Kocherlakota, recently published an opinion piece titled “The Fed Should Consider Lowering Rates”.

Chair Powell’s new communications plan for 2019 calls for each of the FOMC’s 10 meetings to be followed by its own press conference, with the stated goal of offering increased communication with market participants. January 30 will offer a glimpse of whether the increased number of opportunities might also be an improvement.

countries, where inflation rates are often below their central bank (...)){kind=link}