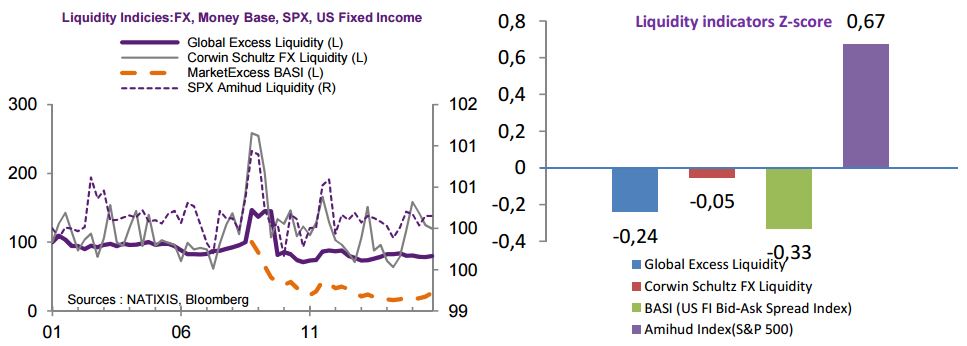

We review several liquidity proxies.

- A global excess liquidity. As introduced previous in our Record, global excess liquidity can be simply expressed by the spread between the growth of the central banks’ aggregated balance sheets and the growth of global GDP. Derived from the simple equation that MV PY (M: quantity of money, V: velocity of money, PY: nominal GDP), excess liquidity is the rate of money creation above the rate of global GDP expansion when assuming the constant velocity of money holds in the equation.

- For FX liquidity index, we use the Corwin Schultz measure that is a simple liquidity measure of market tightness using daily high and low prices (we discussed this measure recently, see Daily FX Liquidity: where do we stand ?)

- For equity markets, we use the so-called Amihud Liquidity index. This is a liquidity proxy by measuring the market turnover impact on equities returns, was used for S&P 500 Index.

- For fixed income, we use the daily spread between bids and offers in US HG segments, so-called MarketExcess’s BASI (a measure of tightness).

For all these indices, the lower the index, the more liquid the markets are.

Barring the financial crisis of 2008-2009, there has been a continuous series of quick recoveries after turmoil events (Taper tantrum, SNB intervention), implying the markets have reacted efficiently. Compared to the historical data since 2010, broader and general liquidity conditions are not yet in the level to be worried about, except SPX which is currently standing at 0.64 standard deviation above the average illiquidity measure.

Given the level of z-score for all asset classes, it appears that stocks look more liquid that they are while bonds are not as illiquid as people believe.

While many corporate bond traders have seen a diminishing liquidity recently after the inception of Volker Rule, this market by nature has infrequent and thin market activities centered, hence longer periods of time to match buy and sell orders are normal. BASI remains tight even with the increasing regulations. US Treasuries Bid-Ask spreads also have maintained tight since the last crisis. Although other studies of liquidity done by New York Fed show small signs of deteriorations after the Taper tantrum of 2013, liquidity in US Treasuries market overall remains healthy in terms of tightness and is far from the distressed level.

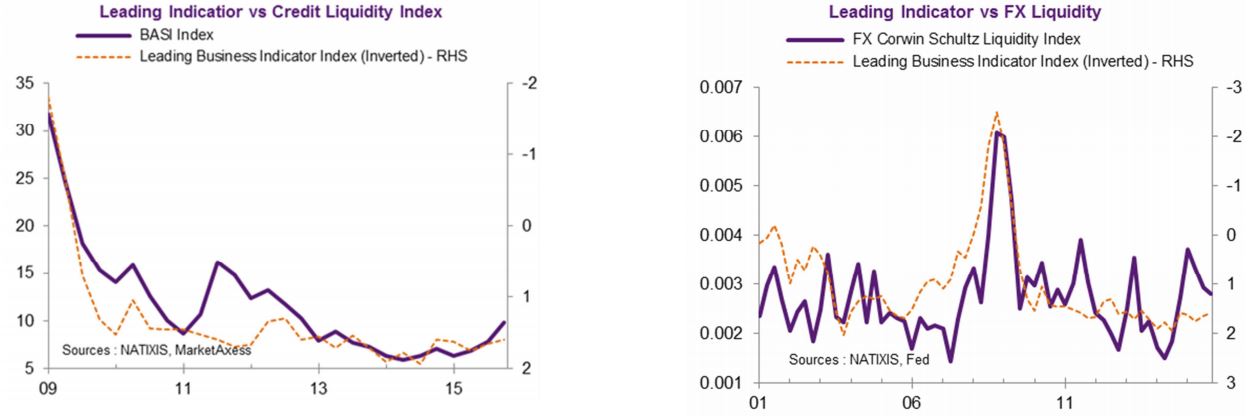

Private liquidity is an important determinant of global market stability apart from official liquidity that is created by central banks. With a growing international dependency between financial institutions, however, both types of private liquidity are becoming closely connected to macroeconomic environment over time. Especially, leveraging and deleveraging cycle of financial institutions can greatly affect the funding viability and credit conditions. Easier credit conditions and increased risk-taking help financial sector activities to enlarge the global liquidity, and when the cycle reverses, deleveraging will reduce liquidity.

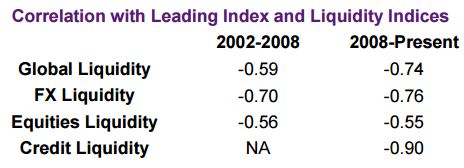

Correlation with leading index and various liquidity indices exhibit a negative sign, which means less liquidity periods coincide with lower business activities in US. Increased correlation between liquidity and business activities after the financial crisis shows an amplified role of cyclical movements in financial conditions.

Bottom line, we reviewed various liquidity measures on different markets. These measures point out that current liquidity for asset classes overall is not in the territory to be worried over yet. We must however acknowledge that these indicators are only partial indicators of the market liquidity that is multifaceted. Also, despite decent liquidity levels, liquidity risks may have also increased in parallel with more illiquidity spikes and more generally a higher volatility of volatility across the board.

){kind=link}