After inaugural government green bonds in 2020 from the Netherlands, Sweden, Germany and Hungary, Italy is the latest country to issue a green government bond. The Italian government issued its inaugural green bond for an amount of EUR 8.5 billion and a maturity of 24 years on 3 March. Although Italy is expected to be a regular green bond issuer and has committed to tap the green bond market on a regular basis, it is not planning to follow Germany’s example and build a full green yield curve.

In this first green bond issue, Italy has identified six categories of use of proceeds: renewable electricity and heat; energy efficiency; transport; pollution prevention and control and circular economy; protection of the environment; and biological diversity and research. During a pre-issuance call with NN Investment Partners (NN IP), it was confirmed that around 90% of the bond will be allocated to transport, energy efficiency and protection of the environment and biological diversity.

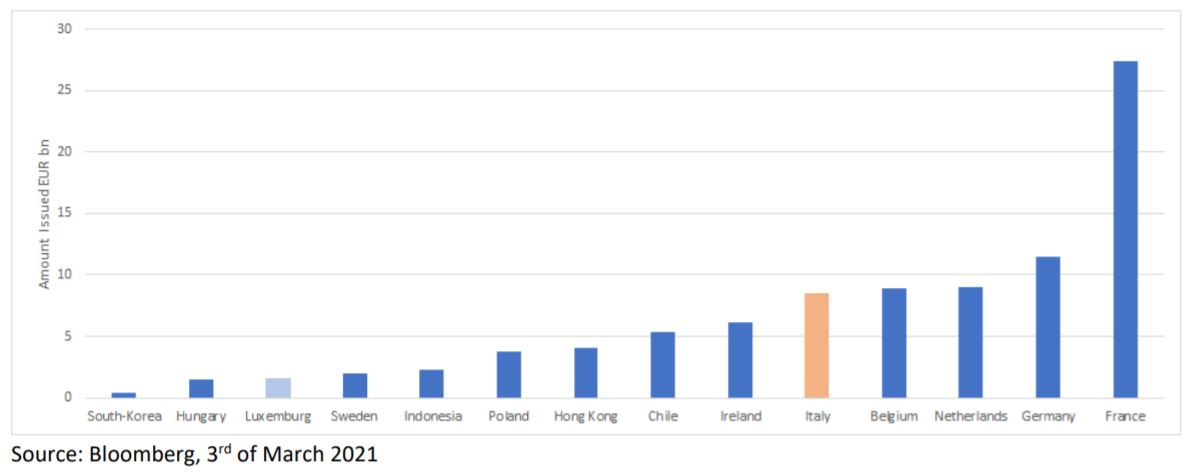

Italy has become the tenth European country to issue a green bond after last year’s sovereign boom in Europe, which

also included a sustainable bond from Luxembourg, financing both green and social projects.

“We believe this is an important milestone for the green bond market as treasury portfolios make large allocations to

Italian government bonds,” said Bram Bos, Lead Portfolio Manager Green Bonds at NN Investment Partners. “The

growth of the green bond market keeps on accelerating and the strong increase in issuance from governments gives

more investors the chance to greenify their fixed income portfolios. We are reaching a stage in which replacing part of a

regular government bond portfolio with green government bonds is a logical and feasible step. The government bond market has become more diversified and will keep on growing, with countries like Spain, UK and Singapore all expected

to issue inaugural green bonds later in the year”.

“We believe this is an important milestone for the green bond market as treasury portfolios make large allocations to

Italian government bonds,” said Bram Bos, Lead Portfolio Manager Green Bonds at NN Investment Partners. “The

growth of the green bond market keeps on accelerating and the strong increase in issuance from governments gives

more investors the chance to greenify their fixed income portfolios. We are reaching a stage in which replacing part of a

regular government bond portfolio with green government bonds is a logical and feasible step. The government bond market has become more diversified and will keep on growing, with countries like Spain, UK and Singapore all expected

to issue inaugural green bonds later in the year”.

As an EU country, in 2019 Italy pledged to meet the EU bloc’s target of carbon neutrality by 2050 to keep in line with the Paris Agreement’s 1.5°C scenario. In February 2021, the new prime minister Mario Draghi announced that climate change would be at the heart of his plans for Italy and said his government intends to boost renewable energy and green hydrogen production. It is interesting that this green bond framework does not mirror that renewable and hydrogen commitment, placing it is as the smallest category of the allocation.

‘’Italy has made efforts to align all its green bond categories to the EU Taxonomy in terms of the mitigation objective criteria’’ said Isobel Edwards, Green Bond Analyst at NN Investment Partners. ‘’While we welcome this, we hope that the ’do no significant harm’ criteria will be considered for each activity as laid out in the EU Taxonomy technical criteria for each industry. As it has unfortunately not been included at green bond framework stage pre-issuance, we hope it will be laid out in the impact report as the ‘do no significant harm’ assessment is one of the key pillars underpinning the EU Taxonomy and EU Green Bond Standard”.

Italy has been a large importer of natural gas over the years, given that its natural gas consumption is 1.5 times more than its total reserves. Unlike some other Italian issuers, the framework of the green government bond does not include natural gas as an eligible activity. NN IP hopes this signals a more strategic shift to reduce the share of natural gas in the country’s energy mix in the coming years.

’’Protection of environment and biological diversity’’ is a significant category in the framework. Biodiversity and land protection are crucial, not just because they provide more resilience against future extreme climatic weather events, but also because restored high carbon landscapes with rich biodiversity can act more effectively as carbon sinks and therefore provide mitigation benefits.

One question remains about the inclusion of maritime infrastructure in the green bond framework. This forms part of a wider plan for Italy to develop their maritime freight network. Given that the shipping industry is not yet on a transition path in line with the 1.5°C scenario, NN IP recommends that the available guidance from the EU Taxonomy on shipping and maritime infrastructure should form the basis of any plans involving maritime freight going forward.

NN IP increasingly sees mining being excluded from issuers’ green bond frameworks and Italy is no exception. It is understandable that issuers feel that they cannot establish sufficient safeguards in these industries to ensure robust environmental standards. However, more metals and minerals will be needed in the future, in particular rare earth metals, as these required for renewable technologies such as electric vehicle batteries. It is crucial to invest and find a way to source and recycle these sustainably, if we are going to develop into a green economy. Issuers should not feel afraid to be ambitious in this area and look for solutions for green mining.

){kind=link}