Given the degree of volatility in markets, and the extreme nature of the quality/growth outperformance, we would expect in any recovery for there to be times when value – typically those companies which may go out of business given the degree of the contraction – will outperform. Similar periods occurred temporarily in Q2 2003 and Q2 2009 as markets rallied.

However, our contention is that given elevated levels of debt, the 2020s may well be similar to the 2010s with low growth, inflation and interest rates – at least after the sugar rush of the immediate recovery from such depressed levels of economic activity. In this low growth environment, I believe it is entirely realistic that quality will outperform value, as long as quality companies continue to earn high returns, which it is our job to research.

For those fund managers with a consistent style skew in their portfolios, there will always be times when underperformance should be anticipated, as well as outperformance. In the wake of the Covid-19 pandemic the potential for style shifts to impact performance is amplified, and in our view a sustained period of quality outperformance is likely.

2020 MARKET MOVES

In March, markets descended into chaos as Covid-19 became a global pandemic, with spreads widening hugely – to more than 10% in high yield – and equity markets down by more than 30%. From there we have witnessed a rally driven by central bank stimulus along with the belief that this is a temporary situation and the corner will soon be turned (as well as sideways movements and, more recently, some extreme downward swings in markets). There has certainly been less leadership in markets and something of a swing to value from growth has been seen in the past few weeks.

However, I would caution against the view that this is a more permanent rotation of style performance. Our central forecast is that economic activity will get back to end-2019 levels by the end of 2022. While it is encouraging that we have seen progress across Asia and much of continental Europe in terms of low levels of new coronavirus cases, it is unlikely it will be a smooth ride from here. We are cognizant of the possibility of a second wave of Covid cases before we reach the holy grail of a scalable vaccine, and such a second wave could rock economies and markets alike. We are already seeing market setbacks and increased volatility as parts of the world emerge from lockdown. The recovery is clearly not going to be linear between now and 2022.

Such a backdrop is not one where value is likely to outperform. At the end of the global financial crisis in 2009 we saw a sugar rush within markets, specifically for a couple of quarters from March that year where value stocks performed very well. This is clearly being mimicked in some markets today, but following unprecedented levels of stimulus and government intervention the level of debt is going to be even greater than it was after 2009, so that rush of recovery is unlikely to persist. We will thus emerge into a world of low inflation, low growth and low interest rates.

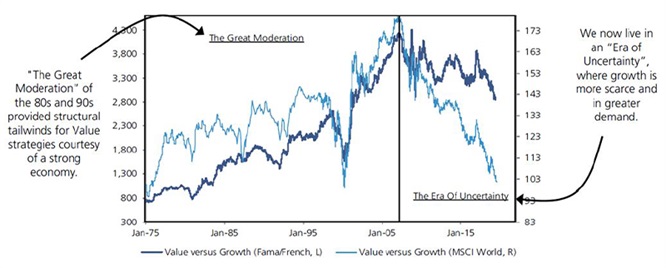

This is shown in Figure 1, with faster growing companies standing out in the slower growing, post-global financial crisis environment – referred to as the “Era of Uncertainty”.

Figure 1: The 2008 crisis ushered in a structural shift in the style cycle

- UBS Quantitative Research, septembre 2019.

A big fiscal deficit is of course potentially inflationary, but any inflation is unlikely to persist – for two reasons. One is that there is a lot of spare capacity within the economy (as measured by unemployment and low industrial capacity utilisation), and secondly, if we do begin to see inflation it will be accompanied by rising interest rates and that will quickly dampen growth due to the cost of servicing such high levels of debt.

So the 2020s are likely to be similar to the 2010s and this is an environment in which we would expect quality companies and those less cyclically oriented to perform better. We would therefore caution against a rush to value and poorly performing stocks irrespective of the outlook. Clearly, there will be periods where this is tested, and that may well be sooner rather than later, but it is less likely to be persistent.

Moreover, even if value looks attractive at any point, as investors we must be extremely certain that we can avoid value traps. The companies that are financially, as well as operationally, leveraged appear very dangerous entities for us to be committing capital to at the present moment.

SO WHAT DO WE LIKE?

We still believe that those companies taking share from their dominant market positions, such as those within technology and communications, as well as the large semi-conductor companies, are well positioned and will continue to be the winners as we move forward. Companies that are operationally leveraged but have a strong balance sheet can be quite attractive, but they tend to be the quality economically sensitive or cyclical companies where we will already have positions.

Within fixed income we prefer investment grade over high yield credit because we are keen to have exposure to companies that have a stronger chance of weathering the current environment better. We prefer credit over government bonds given the significant number of negative yields at the moment. So while emerging market debt and high yield in general has recovered reasonably well in recent weeks, we prefer IG from a risk/reward viewpoint against the uncertainty over the next couple of years and the direction of the recovery.

Within equities, we continue to believe the outlook for global smaller companies remains excellent and remain confident of our ability to find opportunities in quality companies that have the potential to grow into the behemoths of their respective industries over time. Also, within our value proposition we are careful to select the better-quality names that have low levels of leverage.

We like to invest in companies that have strong market positioning and good business models. They tend to be leaders in their sector and possess some sort of economic moat that distinguishes them from their competition in a growing sector, allowing them to create high or sustainably rising returns. These quality companies have a well-established management team with a transparent governance structure. We look for financial strength in the form of a solid balance sheet, high quality earnings and the ability to generate ample cash flows. All these factors should come at an attractive valuation which is also an important factor in our quality investing process. These are the companies we believe will outperform as we go through the 2020s and will benefit in this environment of low inflation, low growth and low interest rates.

){kind=link}