Infrastructure assets are large-scale facilities and services essential for the orderly operations of an economy like transportation assets (for example toll roads, railroads and airports), regulated utilities (such as water distribution systems, gas and oil pipelines), communications assets (wireless communication towers) and social infrastructure assets (for example schools and hospitals).

Dedicated infrastructure funds were first developed by Australian banks in the mid-1990s and they began to expand significantly in the 2000s in the US, as well as Europe and Asia, following the dotcom crisis.

«The sector enjoys high barriers to entry due to the high cost for developing the assets. It means that infrastructure financial performance should not be as sensitive to the economic cycle as many other asset classes due to their general characteristics : stable and predictable cash flows, low default rates and partial inflation hedge as the services paid by end users are often subject to inflation clauses» explains Henry Boua, Associate Director for France and Monaco at ETF Securities.

Even if infrastructure investments shares some of the characteristics with fixed income (long term predictable yield), real estate (investing in physical assets) and private equity (leverage is used), its popularity is increasing among investors. In fact, these assets offer reliable long term cash flows with inflation protection and exhibit a low correlation to other asset classes, as shown below.

« However, investors should bear in mind that infrastructure assets are exposed to a number of specific risks like regulatory risks through long-term concession agreements or operational risks for example. In addition, the leverage involved in financing infrastructure assets exposes investors to the cost of debt and refinancing risks » says Henri Boua.

Despite these different types of risks, a growing number of investors are looking to include infrastructure assets in their investment portfolio.

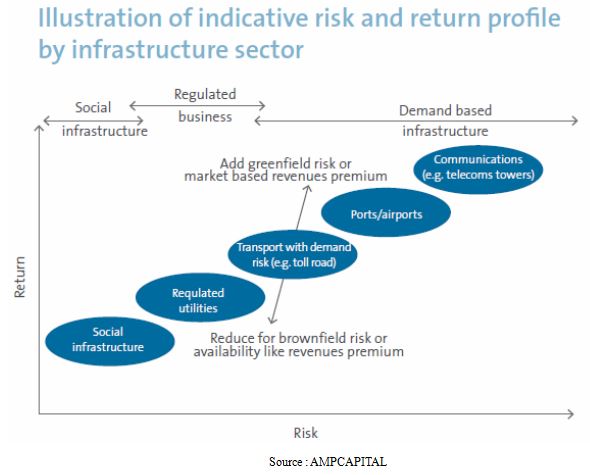

While target returns have dropped since the financial crisis in 2008, Preqin reports that three-quarters of infrastructure funds report IRR objectives of 10,1% to 20%, depending on the nature of infrastructure, as shown on the below.

As investors become more comfortable with the risk/return potential of these funds, allocations to this asset class are likely to rise. According to the 2014 Preqin Global Infrastructure Report, 46% of surveyed investors are planning to increase their allocation to infrastructure over the long term.

«Globally, only of a small portion of infrastructure assets are currently listed on stock markets through infrastructure companies. But, it is possible to invest through a variety of infrastructure vehicles, including: private equity-type investments (mostly closed-end funds), listed infrastructure funds (closed-end or open-end, including ETFs), and direct unlisted investment» says Henri Boua.

, real estate (investing in physical assets) and private equity (leverage is used), its popularity is increasing among (...)){kind=link}