- We equate ‘helicopter money’ with monetary financing. On an ex post basis, the UK, US and Japan can be thought to have experienced de facto monetary financing already, and it didn’t come with an explosion of inflation. The evidence doesn’t suggest that new helicopter money, if implemented, would spark inflation either.

- Monetary financing isn’t a wacky new policy and is easy to understand once you look at ‘money’ the right way. We should treat government debt and taxation as two forms of monetary sterilisation rather than financing operations.

- There are not clear advantages to announcing a policy of helicopter money over announcing a traditional debt-sterilised fiscal expansion. Indeed, it could end up being a backwards step.

Central banks in Europe and Japan have experimented in recent quarters with slightly negative interest rates. In doing so they have broken what many had assumed was a zero lower bound for nominal interest rates, and also given some indication as to where the true lower bound may lie (which is to say around where rates now sit). The question as to how central banks will respond to the next recession has arisen amongst academics and investors.

One option being discussed is ‘helicopter money’. Helicopter money refers to the situation where a central bank finances the fiscal expenditure of a government. Or in common parlance, the government prints money instead of raising taxes or debt to fund spending. To many this evokes the sort of policy that brought hyperinflation to Zimbabwe or the Weimar Republic – and as such provokes meaningful alarm. In this piece I will outline why the implementation of quantitative easing during periods of fiscal expansion in the UK, US and Japan have effectively already delivered ex post helicopter money, and why true helicopter money appears less attractive as a policy option than additional levels of traditional debt-financed fiscal expansion, supplemented if need be by further quantitative easing. But in order to make this clear, it is necessary to look at what money actually is and how it works.

What is money?

We tend to think of money in the bank and money in our wallets as the same thing. That we do so attests to the success of the monetary system in place. Rather than both being money, one (the bank deposit) is ‘Inside Money’, while the other (the bank note) is ‘Outside Money’. These are not fungible and are instead like oil and water. Inside (bank) Money is imagined into existence by banks in the process of creating a loan. Outside (government) Money is imagined into existence by the monetary sovereign (in the case of UK, the US or Japan, this is the government).

Inside Money

Imagine that you go to your local high street bank for a loan. In granting the loan the bank creates a deposit in your account. This deposit is a liability on the bank’s balance sheet against which it holds an asset (a loan to you). If you choose to transfer your (borrowed) deposit to another depositor of the same bank (let’s say, if you bought a house from me and I was also a customer of the same bank), the liability (eg, the deposit) never leaves the bank. If you transfer my (borrowed) deposit to a depositor of another bank, your bank would need to settle the transfer (at the BoE) – but the liability would never leave the banking system. And so, Inside Money exists only on a bank ledger and can never take physical form. Inside Money, to be specific and a trifle more technical, is the short-dated liability of the banking system. Changes in bank lending practices do not change Outside Money a jot.

Outside Money

Outside money (government money) is money that is imagined into existence not by a bank making a loan, but by the monetary sovereign (in the case of the UK, US or Japan, this is the government) making a payment. It is like an undated government IOU.

Imagine that a government pays a civil servant. As the monetary sovereign they can do so by creating brand new Outside Money. The government then typically seeks to destroy an equal amount of Outside Money to offset this monetary expansion, and this process of money destruction is called monetary sterilisation. Why do governments sterilise their money creation? The typical answer is to maintain confidence in the currency. After all, if a government went out increasing the stock of outside money exponentially it is quite conceivable that recipients might begin to become concerned that this Outside Money may not be a good store of value and so seek to turn it into goods and services at higher prices (and so lack of confidence could show up in the form of inflation), or they could seek to turn it into other peoples’ currency (and as such show up in currency depreciation) or real assets (and as such show up in real asset inflation).

Figure 1: How Outside Money is created and removed from the economy

Figure 1 shows stylized balance sheets of the non-bank private sector (of which the civil servant is part), the commercial banking system, the central bank and the government before this hypothetical civil servant is paid (column 1), immediately after but before the money is pulled back out of the system (column 2), and then after the two different forms of monetary sterilisation (columns 3a and 3b).

The government has two routes to sterilise the monetary expansion. First, it can issue debt in the form of new bonds to the private sector (column 3a). By selling bonds to the private sector the government will successfully take the new Outside Money out of circulation, and replace this Outside Money with bonds that cannot be so easily spent. Secondly, a government can tax (column 3b). Taxation is a form of monetary sterilisation – with tax revenues effectively torn up in order to maintain confidence in the currency. In the UK, by virtue of having signed the Maastricht Treaty, the sterilisation action will always happen simultaneously or before the payment to the civil servant. But this outline of how Outside Money works remains valid.

Figure 1 illustrates not only how Outside Money works, but also a couple of other things. Firstly, it shows why it is peculiar to worry about debt sustainability from a fiscal (rather than a monetary) perspective. Government debt can be seen to be no more than an instrument for monetary sterilisation: a means by which zero-coupon perpetual government IOUs (Outside Money) are removed from circulation and replaced with interest-bearing government IOUs with a specified maturity (although they will at that point again become perpetual zero-coupon government IOUs). The prospect that a monetary sovereign might be unable to sell government bonds is real, but untroubling from a financing perspective; the prospect of a bond market strike is instead troubling only from a monetary perspective.

Secondly it illustrates that when debt-sterilising rather than tax-sterilising, the private sector ends up with a larger balance sheet. Government bonds are treated as assets, although they are claims against the rest of the non-bank private sector who don’t own bonds. Given that taxation tends to be progressive in democracies, it would appear likely that the distributional consequences of debt sterilising rather than tax sterilising would be to leave upper deciles of the income distribution holding more bonds and having paid fewer taxes. That is to say, that there will likely be higher levels of wealth inequality under a government that prefers to maintain confidence in the currency via debt sterilisation, all else equal.

Now that Outside Money has been outlined, with debt issuance and taxation explained as instruments of monetary sterilisation, quantitative easing can be seen to be a pretty straightforward reverse-sterilisation operation. As government bonds are bought by the central bank, so the monetary base (in the form of Reserves and Currency, eg Outside Money) becomes inflated. While the bonds are held by the central bank they are effectively cancelled: they do not perform their monetary sterilisation duties and there is no net interest cost of holding them to HM Treasury over and above the cost of remunerating holders of Reserves (which would need to occur even if cancelled).

Figure 2 helps show the relative scale of Inside and Outside Money. The dark blue section shows M4 as a percentage of GDP as a decent proxy for Inside Money and the light blue section shows Outside Money as a percentage of GDP. Two things jump out. First, there is a lot more Inside Money than Outside Money. Secondly, the acceleration in growth of Inside Money was spectacular in the years leading up to the Global Financial Crisis, and the collapse thereafter has been precipitous. The expansion of Outside Money in the form of QE has but cushioned this contraction in the money stock.

Figure 2: UK Inside and Outside Money 1986-2016

With circa 250% debt to GDP many have asked whether Japan’s debts are too big to ever repay (Figure 3). Government debt is rarely repaid. Bonds issued to sterilise a government’s fiscal expenditure mature and are typically repaid by the proceeds of issuance of new bonds.

And so the debt issued by the British government to finance the Napoleonic Wars has never been repaid. But pursuing this line is to miss the point.

We have already seen that government debt is no more than an instrument for monetary sterilisation: it is a means of reducing the number of IOUs in the system, by replacing them with long-dated IOUs that can’t be easily spent. As such, the issue of debt to GDP should not be seen as a fiscal constraint: a government can’t run out of government IOUs. That said, uncontrolled debt growth could conceivably become a medium-term threat to monetary stability (eg, people might stop accepting government IOUs as payment). Uncontrolled debt growth comes with the uncontrolled growth in debt service obligations. And these debt service obligations come in the form of the creation of more Outside Money which in turn needs to be sterilised.

Figure 3: UK government debt to GDP / Japan government debt to GDP

Despite high levels of debt to GDP, Japan’s debt service costs are today amongst the lowest in the world, owing to low interest rates. In a scenario where inflation rises and policymakers want interest rates to rise, the stock of debt could become problematic (as maturing debt is refinanced with bonds carrying higher coupons) if nominal GDP growth is sufficiently absent (so that debt-to-GDP rises ever-higher). Essentially, the threat to Japanese monetary sustainability from its stock of government debt is the threat that people will stop accepting yen from the government as payment. As long as the government has the power to enforce demand for yen in the form of a requirement to pay taxes, this possibility appears de minimis.

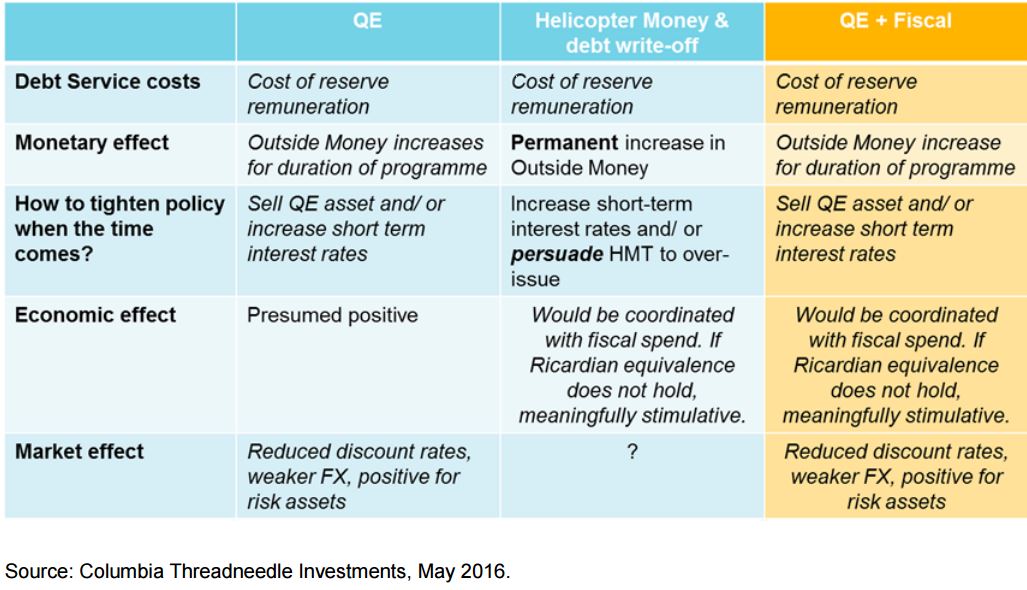

We have seen that when a central bank purchases government debt it unwinds past monetary sterilisations. Debt bought by the central bank is effectively cancelled for the duration of the QE programme. In the two charts within Figure 3 we can see the degree to which these QE programmes have impacted the UK and Japanese government’s debt to GDP metrics. In the case of the UK, the QE programme (running contiguously with fiscal expansion) had the effect of helicopter money. This can be seen from Figure 4.

The table outlines the impacts of QE, of helicopter money (where debt is purchased by the central bank and written-off), and a combination of QE and fiscal expansion. Given that debt is effectively cancelled from the moment it is bought by the central bank from a monetary and fiscal perspective, the debt service and monetary effects of QE and helicopter money appear the same.

Figure 4: Comparing quantitative easing, helicopter money, and fiscal expansion

combined with quantitative easing

The big difference arises when it comes again to tighten policy. By cancelling government bonds bought, the central bank cannot so simply resterilise the unsterilised Outside Money stock. If it wishes to calm inflation quantitatively it can auction central bank bills, term deposits and implement reverse repo programmes, all of which put upward pressure on shorter-term interest rates. And so it is left with the option of either raising short-term rates by more than they would otherwise need to rise under the QE scenario, or persuading the government to gift the central bank with large amounts of government debt that it can then sell to the market (which may be tricky politically).

The economic effects of quantitative easing are still being debated, but it is fair to say that they are presumed to be positive to date. In the case of helicopter money, there would be a direct fiscal expansion financed by central bank purchase of (and cancellation of) government bonds.

This direct fiscal spend would be economically expansionary, unless the announcement of helicopter money represented a shock to households and firms that was sufficiently significant to offset the fiscal stimulus. The economic effects of fiscal expansion combined with new quantitative easing appear identical to those of helicopter money.

The market effect of the recent experience of QE has been lower discount rates, a weaker currency, and a strong environment for risk assets. We might guess that the market’s reaction to helicopter money would be similar, but given that past episodes of dominance by the fiscal authority over the central bank have been associated with fiscal indiscipline and high inflation, there is a reasonable chance that markets could react in a meaningfully different and negative way. The truth is that we just don’t know.

Hyperinflation

Helicopter money is often associated with incidence of hyperinflation. In their study of the 56 incidents of world hyperinflation during the last 300 years, Hanke and Krus found hyperinflation to be ‘an economic malady that arises under extreme conditions: war, political mismanagement, and the transition from a command to market-based economy to name a few’. By contrast, monetary financing has been used widely in the developed and developing world over time without ending in hyperinflation.

Until the US Fed Accord in 1951 the US operated a policy of fixing long-term bond yields, and as such expanding or contracting Outside Money depending on private sector demand for these instruments. Canada used monetary financing for 40 years until 1975 under a free-floating exchange rate regime without calamitous macroeconomic effects, and India operated a policy of debt monetisation until 2006. Further examples abound. Indeed, of the 152 central bank legal frameworks analysed by the IMF, 101 permitted monetary financing in 2012. This is not to say that helicopter money is a desirable policy. It would be, in the opinion of this author, a backwards step. But neither is it to be necessarily associated with hyperinflation.

Conclusion

With the unknown market impact of helicopter money, with prospective policy tools in the hands of central banks narrowed through debt cancellation, and with the economic benefits associated with helicopter money rather than straight fiscal expansion de minimis, it is not clear why policymakers will choose the path of helicopter money. Perhaps the real lesson is that monetary policy has its limits and that in the event of an economic slowdown, aggregate demand is best supported by fiscal rather than monetary policy. In the event that new fiscal expansion requires supplemental monetary support in the form of additional QE, that is a decision that could be made at some point in the future.

So, in conclusion, helicopter money is not a weird and wacky new form of money. Indeed, once we understand how money works helicopter money looks pretty straightforward. The prospective economic, monetary and fiscal effects of helicopter money (absent the stickershock of a new unfamiliar policy being implemented) look identical to a normal fiscal expansion supplemented with additional QE. As such, it could be argued that the UK, US, and Japan have all already effectively experienced helicopter money. It is harder to say the same about the Eurozone, consisting as it does of government entities that are not monetary sovereigns. Indeed, the Eurozone is much more complicated.

){kind=link}