The consensus now expects a supportive 2021 backdrop for risky assets. With vaccines rolling out and continued reflation policies, the normalization of the world economy would accelerate, amid lower geopolitical uncertainties, still ample global liquidity, and large accumulated savings being gradually put back to work. Meanwhile threats from unprecedented stimulus and from rising inequalities would not surface immediately.

Yet, investors still expect an atypical vintage with multiple wildcards. With little clarity on the timing of herd immunity and the threat from virus mutations, getting the right sequence of regional, sector, and quant factor recoveries will remain a challenge.

Investors will also have to navigate rich, consensual and crowded assets, requiring skilled market timing, all the more so they will have few options to protect their portfolios. Here’s how hedge funds are navigating these paradoxes.

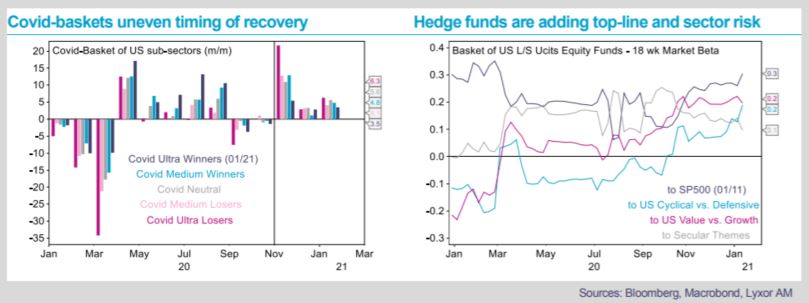

After rushing to defensive and growth stocks back in February, U.S. L/S equity hedge funds briefly reweighted cyclicals in March and April, before taking some profits as the rally matured. The main move after the crash, which generated significant alpha, has been to allocate to stocks exposed to secular trends (including digitalization, climate change, stayhome). The likelihood of a more ambitious Democrat reflation in the U.S. and vaccination announcements in November finally led managers to add more risk. With markets starting the year in euphoria (a usual pattern when exiting a recession), hedge funds have further raised their exposures in January, still overall favoring cyclical over value stocks.

In detail, we find that, in aggregate, hedge funds continue to stay away from stocks that have been the hardest hit by the pandemic and that rallied the most since November (see our covid-baskets of U.S. equity sub-sectors).

Instead, they favored stocks that have not too meaningfully lagged in 2020, displaying operational leverage and having a positive cyclical bias. Cheaper than stocks that shined last year, these include business services, construction, household products, specialty retail, auto, and chemicals stocks. We find that managers are also starting to increase allocations to stocks that have been a little more hit in 2020, including sectors such as financial services and industrial conglomerates.

In summary, U.S. hedge funds are adding risk and cautiously exploring higher-quality value stocks, as confidence firms up and as cyclical stocks richen. Meanwhile, managers are trimming their tech and secular trend exposures to marketweight. In other words, they see the recovery moving forward with global liquidity tailwinds, but they are not decisively rotating their portfolio towards value at the expense of growth and cyclical stocks yet. They also avoid stocks most vulnerable to a relapse in virus restrictions. Elevated managers’ return correlation tells us that value vs. growth exposures and market-timing are dominant drivers, while their elevated return dispersion reveals heterogeneous positioning.

){kind=link}