Stock dispersion soared a few days before the selloff, but we expect a rapid mean reversion. Historically, higher dispersion following spikes of volatility only lasted when coinciding with a major macro shift.

Managers will not enjoy the extra arbitrage potential for long.

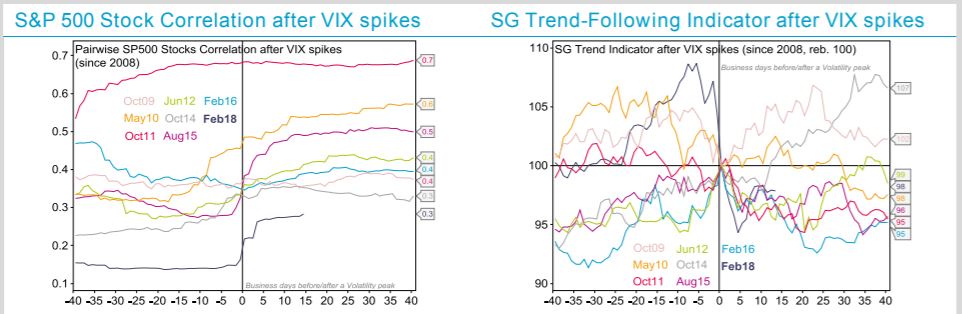

By contrast, we expect that the current stock re-correlation will last, with a common set of drivers likely to stay on the radar (including rates, inflation, dollar). Distracting markets from companies’ fundamentals, it will make bottom-up selection more challenging.

The cold shower on the U.S. earnings season was telling: strong earnings and revenues were disregarded, while returns after EPS announcements largely resulted from broader market moves.

That said, conditions are still supportive. Stock correlations remain moderate, reflecting a rich set of themes that will unfold in the coming months, including the tax reform, fiscal spending, a capex revival, and corporate activity. Moreover, most diversified funds maintained their exposures during the selloff and managed to generate alpha. We keep our preference for deep value funds and our underweight on quant/neutral funds.

We are more skeptical regarding trend-followers in the coming weeks. Multiple trends broke during the selloff. While few assets now remain stretched, a majority could be range trading. We see reduced reversal risk, but many false starts. The shock was strong enough to force a profound reshuffling of their exposures.

In aggregate, CTAs cut their long equity and commodity exposures by half, but maintained their short USD (especially vs. EUR) and their short U.S. bonds. They neutralized the bulk of their long European and Japanese Bonds.

While we acknowledge their risk profile is considerably safer (which tells us that the deleveraging is behind), they would not fully benefit from the recovery. Moreover, the market structure will take time to settle down and allow for new trends to shape up. Historically, CTAs struggled after most large selloffs. We keep our neutral stance, with a negative watch.

the fixed income funds, flat this week, still isolated from the epicenter, and ii) neutral equity funds, still suffering from sector and factor rotations. This week, we (...)){kind=link}