UK government leaning towards a ‘hard-Brexit’

It started on 2 October, when British Prime Minister Theresa May told the annual Conservative Party congress that the UK would trigger Article 50 (the official legal notification of the UK’s wish to leave the European Union (EU)) “no later than the end of March”. May’s final setting of a hard deadline for Brexit has grabbed the market’s attention in recent days.

The subsequent statements from PM May suggest that immigration control will be the UK government’s top priority, potentially at the expense of a weaker negotiating position on all other issues, including of course the contours of a free trade agreement with the EU. May’s statements do not preclude a “soft” Brexit (ie. one that seeks to preserve the UK’s economic links with the EU as close as possible to existing arrangements), but they do significantly increase the odds of a hard one.

Hard Brexit means hard time for the GBP

Accordingly, the political factor has begun to weigh heavily again on sterling, even as the economy has held up much better than many had expected after the 23 June referendum. Indeed, UK purchasing manager index (PMI) surveys released on 4 and 5 October showed that activity in September remained quite resilient, and markets have lowered their expectations for cuts in the bank rate compared to the levels seen after the August Monetary Policy Committee meeting. Yet it is noticeable that a resilient economy and reduced expectations for monetary policy easing have not helped push the GBP higher. Unfortunately, the currency impact of political factors is very difficult to apprehend, but the chances are that they will be at the root of sterling volatility for some time to come.

Using the GBP’s withdrawal from the European Exchange Rate Mechanism in September 1992 as a guide and adjusting it for fundamental valuations, our analysis suggests that an exchange rate of USD1.25-USD1.35 per GBP range was roughly in line with a soft-Brexit scenario. But should a hard Brexit occur, the example of 1992 suggests that the GBP could fall closer to USD1.15 per GBP.

Given that UK’s ‘hard Brexiters’ are at the helm of negotiations with the EU and given the PM May’s recent statements, it seems reasonable that the GBP’s exchange rate should reflect the greater likelihood of a hard Brexit. This seems to be what occurred between 2 October, when May gave her speech, and 7 October. In this period, the GBP declined from USD1.30 to close to USD1.25.

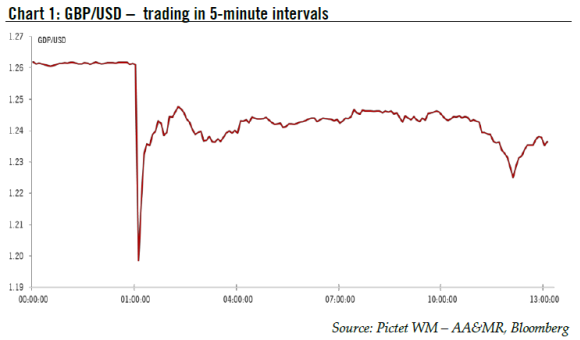

‘Flash crash’ in Asia

It is still unclear what caused the sharp decline in the GBP early on 7 October. But the high volume of GBP sell trades occurred at a moment of very low liquidity, resulting in a roughly 6% drop in the GBP/USD exchange rate, which fell to a 30-year low of 1.1841 in the space of a few minutes. In spite of the rapid (but partial) recovery in sterling’s value, it is quite worrying to see a major currency moving so much without any key triggers. Consequently, investors attracted by sterling’s valuation (it is 28% undervalued versus the USD on a CPI-based purchasing power parity) may think twice.

Macro risk for UK GDP

Whatever the reasons for the sudden, sharp fall of 7 October, the GBP remains exposed to various macro risks. Hopefully, the BoE policy meeting on 3 November and the Chancellor of the Exchequer’s Autumn Statement on fiscal policy on 23 November will provide some clarity for sterling. The BoE has made it clear its intention to create “fiscal space” to allow the government to put in place a more accommodative policy-mix after the Brexit vote.

As mentioned, recent activity data have been stronger than expected on balance. The latest PMI indices pointed to a GDP growth rate of around 0.2- 0.3% q-o-q in Q3 (compared to our own forecast of stagnation). But there is also growing evidence of rising imported inflation. This, in isolation, may be enough for the BoE to remain on hold in November, although we still think the Bank is likely to be more afraid of the long-term consequences of market volatility and political uncertainty. We therefore still expect further monetary easing in November, including a final cut in the bank rate to 0.10%, but we also acknowledge that the BoE’s next move could be postponed until next year.

At the same time, recent utterances by PM May and other government officials have left markets confused about the scale and composition of any change in the fiscal stance. In particular, it was not clear what the PM meant in her speech at the Conservative Party conference this week when she said that monetary policy created bad side-effects and that “something had to change”. Most likely, she was talking about fiscal policy rather than any attempt to reduce the BoE’s influence, let alone independence. However, a very large fiscal stimulus still looks unlikely, in our view, in light of the latest comments by Philip Hammond, the Chancellor of the Exchequer, that fiscal consolidation had to continue even though he intended to relax deficit targets.

Broader political uncertainty in a post-Brexit world is a further macro risk hanging over the GBP, especially if the UK government is indeed headed towards a hard Brexit. Some sectors of the economy could be hit very hard in such a scenario. Our forecast of 0.9% GDP growth in 2017 would likely prove over-optimistic, and the GBP could feel even greater pain than it has already.

Caution towards sterling still warranted

Looking forward, the UK’s large twin deficit should continue to weigh on sterling as the high uncertainties facing the UK economy will make it harder to attract inflows. Consequently, a weak sterling environment is likely to prevail in the coming months and favour a move toward USD1.20 per GBP. As such, prospects for the GBP remain unattractive.

){kind=link}