Lukas Daalder believes that the current bull run may come to an temporary end in the coming months – with values possibly falling by 10% in a long-awaited ‘correction’ – unless the macroeconomic data can justify ever-higher values.

Subsequently, his Robeco Asset Allocation team has cut exposure to global equities from a long-standing overweight position to neutral as a precaution against potentially lower prices. The multi-asset portfolio team has also raised its overweight to the US dollar, believing it will rise further in value once the Federal Reserve does raise rates.

“Two considerations made us take the decision to lower our exposure to equities,” says Daalder, Chief Investment Officer of Robeco Investment Solutions. “The first can be summarized by the simple premise that one should buy low and sell high.”

“Worldwide stocks have yielded a 7% return in local currencies so far this year (16% in euros), which is more or less the return you could expect in an average year, and even more than we had bargained for at the end of last year. As this gain is not matched by earnings, stocks have become more expensive in the process. The risk/reward outlook for equities has deteriorated, which means that reducing risk is the logical move to make.”

“Second, we raised the question as to what do we think is the more likely outcome from this point forward: a 10% further rise, or a (temporary) 10% correction? Although we can certainly not exclude the first option, it is clear that we feel that the odds for the second option have risen in recent months. Based on that premise, we do not think an overweight position is still warranted, which is why we move back to neutral.”

‘We do not think an overweight position is still warranted’

Sitting duck syndrome

Daalder says the roots of the decision go back to last September, when the high exposure to equities made him feel like a “sitting duck” during particularly turbulent market periods. Although the portfolio was able to ride out the storms and make good returns for investors, it was a nervous experience.

“For the better part of two years, we had an unchanged overweight position in equities, which by the end of 2014 had reached a maximum long position. This position served us well as stocks moved upwards,” he says.

“However, while stocks continue to hit new all-time highs throughout the year, we needed to stomach substantial drawdowns between highs: in the September-October period the drawdown reached 8%. During these volatile movements we remained overweight in equities, which limited our capacity to act effectively during sell-offs, making us a bit of a sitting duck during these down periods. As ducks, we sat, and were rewarded in the end, but it did not feel all that comfortable.”

Daalder says he expects volatility to be just as bad in 2015, for three reasons:

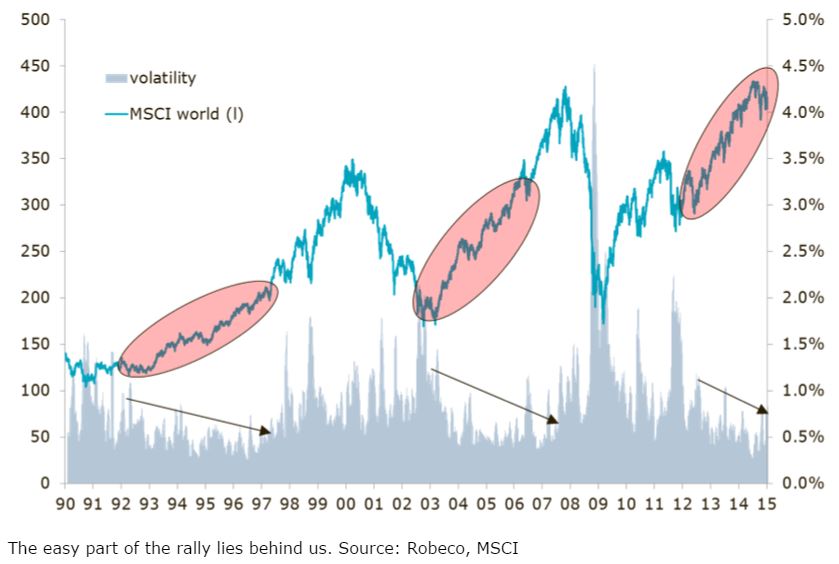

- Equities have become more and more expensive. “This means that the easy part of the rally is behind us,” he says. “This is a pattern that could easily be spotted in the previous two equity market cycles: five years into the upswing, volatility started to increase, as equities were no longer the cheap, easy bet out there.”

- The translation of divergence in the world economy into differences in monetary policy will become stark when the faster-growing US raises rates while the slower-growing Eurozone and Japanese economies remain in easing mode. “Traditionally, stocks do not suffer that much from a first rate hike, but there is a rise in volatility around it nonetheless,” Daalder says.

- Increased political tensions concerning Greece and Ukraine, and also Chinese saber-rattling against Japan in the South China Sea. “There is still no sign of a solution to either the Greek debt crisis or the Ukrainian war and the related Russian sanctions, so this will continue to weigh on stocks,” he says.

So now what?

Daalder says the big question now for investors is whether this ongoing volatility is going to be part of the stock market’s development or not – and he believes it will.

“The case for that is still pretty strong: even though the divergence in growth rates around the world has been less outspoken than we had anticipated at the start of the year, there are still numerous arguments to expect more volatile trading ahead,” he says.

“The Fed is still on track to raise rates later this year, while equities have only become more expensive in 2015, as earnings growth did not match the rise in stocks. Furthermore, we are concerned about the developments seen in the bond market: the moves are too violent to be ignored.”

“Added to this are the concerns of a bubble in Chinese stocks, as well as the fact that equities have completely ignored political tensions, ranging from Greece to Ukraine and the South China Sea. Finally, we are back in the period of the year in which equity investors historically are not compensated for the volatility risks taken on board.”

In all, Daalder says this justifies the more cautious, neutral, stance on stocks.

{kind=link}