- That’s because even a modest pick-up in growth and inflation could arguably push sovereign yields higher — and prices lower. And that would have notable ripple effects in portfolios heavily weighted toward sovereign bonds — in particular the many passive strategies tied to the Barclays U.S. Aggregate Bond Index.[1]

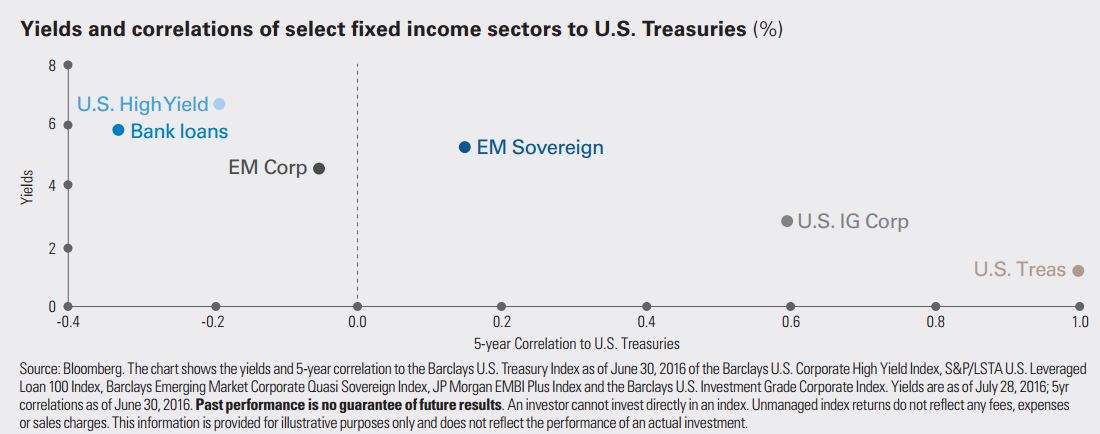

- But by the same token, higher-yielding sectors that have a low correlation to Treasuries could have the potential for further gains if and when growth picks up, and with it, investor confidence. That includes not only investmentgrade credit and emerging markets sovereign debt, but also sectors with a negative correlation to Treasuries, i.e. that have historically moved up when Treasuries move down, including emerging market corporate debt, U.S. high yield and bank loans.

- To be sure, data on the U.S. economy has yet to suggest a huge acceleration in growth. But everything’s relative — and the question is whether there might be enough to be inconsistent with the level of pessimism still priced into Treasuries.

- Consider that core inflation in the U.S. has crept higher to 2.3%[2], matching the highest level in four years — something that a data dependent Federal Reserve will certainly be paying close attention to as it debates the pace of interest rate normalization.

- All this underscores why it could make sense today to look beyond traditional bond benchmarks and their heavy tilt toward Treasuries — to more diversified active strategies, including unconstrained strategies with the flexibility to incorporate higher-yielding sectors of the bond market.

){kind=link}