Last week Lyxor Cross Asset Research team addressed the positive performance of CTA strategies during the market downturn, which started a few weeks ago and dragged global equities nearly -6% lower in May. This fact is nonetheless debatable since other benchmarks, such as the SG Trend Index, have reported a negative performance in May.

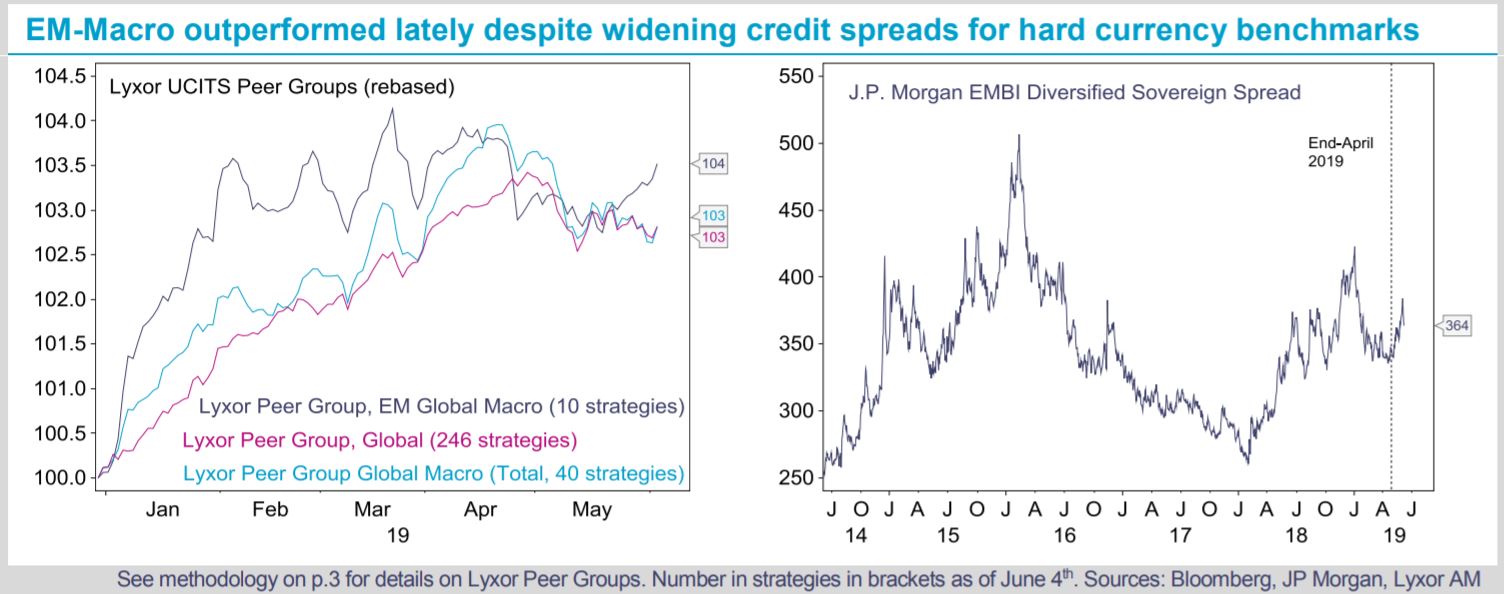

EM-focused Global Macro strategies also outperformed other hedge fund strategies since the beginning of the market turmoil. They managed to deliver slightly positive returns in May according to the Lyxor UCITS Peer Group.

Our views on EM-focused Global Macro strategies has been constructive (Overweight) during the last quarter. They reflect our stance on EM Sovereign Credit, which assumes that sovereign bond yields would remain low for longer in developed markets and higher yielding assets such as High Yield and EM Credit would be attractive in relative terms. The accommodative stance on major central banks has proved to be supportive. EM Sovereign Bonds in hard currency have experienced six consecutive months in positive territory according to the EMBI Global Diversified Index.

Beyond the Fed tailwind for EM-Macro strategies, research on active vs. passive investing also shows that EM Fixed Income is the segment where active investing shows the best results. More than 48% of active managers outperformed their benchmark on average between 2001 and 2018 (compared to only 33% in the U.S. fixed income space) according to S&P. Dispersion across EM issuers tends to be large and active investors who managed to avoid exposures to the usual suspects such as Argentina, Turkey and Venezuela were rewarded.

Finally, with regards to hedge fund performance, most strategies were flat across the board at the turn of the month.

L/S Credit, Merger Arbitrage and Market Neutral L/S were up +0.1% last week. Concurrently, Directional L/S Equity strategies were down -0.2%. Markets were buoyed by the dovish stance of the Federal Reserve, as investors expect aggressive Fed rate cuts could offset the trade war headwind. During the period under review (May 28th to June 4th), the MSCI World was nonetheless down -0.5%.

){kind=link}