None of these trends are new. But the pace of change has likely accelerated by a few years and online payment providers are the winners. They benefit from the shift to ecommerce and tap into new revenue opportunities by leveraging their technology to help traditional retailers in the transition to this new “omni-channel” world.

Generally, Covid-19 has led to an acceleration of the transition to cashless societies globally that should prove a net positive for all players despite the important shift of market shares to e-commerce.

E-commerce is gaining traction

Almost two months of lockdown and store closures have led to a surge in online retail sales globally. Data from Bank of America suggest online represented around 30% of card transactions in the US in May - up from around 15% before the implementation of social distancing policies. Physical stores are going to re-open at some point but it is difficult to quantify how much of this online shift will persist in the longer run. However, we do believe the change in customer behaviour created by the pandemic such as working-from-home is set to have long-lasting consequences. For the first time, online retail has penetrated new age cohorts (those 45 or older) and new product categories (groceries, health products, food delivery). Data from Nielsen shows that – in the UK alone - 600,000 households have tried online shopping in the first weeks after the lockdown was put in place.

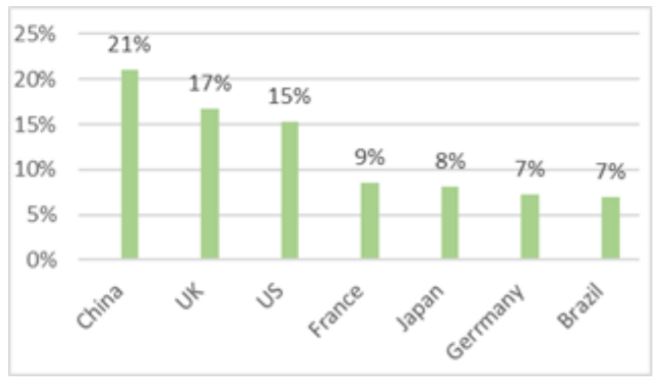

More importantly, penetration rate of e-commerce before Covid-19 suggests there is a long runway for growth. The share of online in retail sales is over 20% in China, hovers around 15% in the US and UK but remains below 10% in Continental Europe and Japan. Overall, this makes us optimistic that the pace of growth in the e-commerce market (low-to-mid teens before this year) is likely to get a long-term boost.

Figure 1: E-commerce as a % of retail sales (2018)

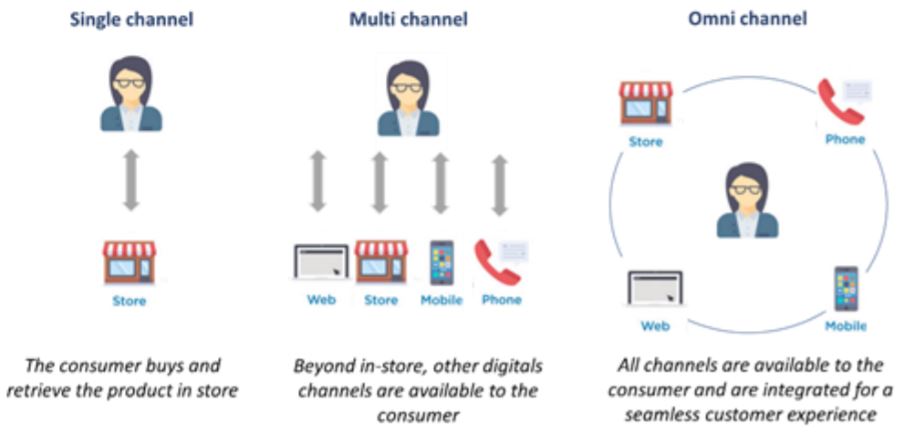

Omni-channel is the new norm

Beyond e-commerce, social distancing has favoured hybrid ways of buying, at the intersection of online and physical retail. For example, a client may want to check inventory online for a given product in different stores, pay for the transaction using his smartphone and then retrieve the item a few hours later at his chosen location (“click and collect”). Buying a product online but being able to return it in store (“click & return”) can also be a popular option notably in sectors like clothing.

Arguably, the lines between physical and online retail started to blur a long time before the pandemic broke out. In 2016, a study from Deloitte found that the experiences of consumers on digital channels (online or mobile) actually influenced 56 cents of every dollar spent in physical stores. However, the stakes are even higher in a context where social distancing might remain the norm for some time.

Omni-channel might seem easy to implement in theory. But in practice, companies have struggled to provide their clients with a seamless and integrated experience across all channels, digital or physical. To push the right offer at the right time, merchants need a single data pool that collects information on transactions across all payment methods and across all channels for each individual customer. That has proven difficult to achieve given the fragmentation of the current payment processing landscape with many retailers using different partners for online and in-store payment processing for instance.

Figure 2: Omni-channel is the next step in the digitalisation of retail

How to access the theme

Winners of the migration to e-commerce are the online payment providers like Adyen and Paypal. The latter announced a record number of new account opening in its first quarter. The emergence of omni-channel provides these players entry into the traditional in-store payment processing market with in-store transactions still representing close to 80% of all payments.

Adyen has gained some traction there with its unique technology that makes it possible for merchants to process all transactions in-store as well as online on the same platform. Both Adyen and Paypal are holdings in the financials strategy.

Other holdings in the strategy, such as the more traditional payment providers Global Payments in the US, Worldline and Nexi in Europe also have a card to play in our view. Covid19 has led to an acceleration of the transition to cashless societies globally that should prove a net positive for these players despite the shift of market shares from in-store to e-commerce.

){kind=link}