The Pandemic Emergency Financing Facility

In 2017, the International Bank for International Reconstruction and Development (IBRD; part of the WBG) established the PEF following the cross-border 2014–15 West African Ebola virus outbreak, which caused more than 11,000 deaths. This outbreak proved the need for an established funding mechanism to mitigate pandemics in developing countries.

The IBRD and the International Development Association (IDA; part of the WBG), in collaboration with the World Health Organization (WHO) and other public- and private-sector partners, designed the PEF to provide surge funding for response efforts in eligible countries to help prevent rare, high-severity disease outbreaks from becoming pandemics. In general, countries with access to the PEF are those eligible to receive resources from IDA.[1]

This funding mechanism aims to provide additional financing to help the world’s poorest countries respond to cross-border, larger-scale outbreaks by complementing, rather than replacing, the much wider role that IDA as well as other international organizations and donors play in supporting pandemic responses. PEF funds can be used to finance the cost of response efforts during an outbreak. This includes, but is not limited to, the deployment of human resources, drugs and medicines, essential and critical lifesaving medical equipment and personal protective equipment, logistics and supply chain of critical supplies, nonmedical equipment, minor civil works (e.g., setting up temporary attention centres), services, transportation, hazard payments, and communication and coordination.

The Insurance Window and Pandemic Bonds

The PEF provides funding to eligible countries through (1) a cash window and (2) an insurance window.

These windows are triggered in different ways and are specifically designed to complement each other.

To date, the PEF has paid out $61.4 million from its cash windows to fight Ebola in the Democratic

Republic of Congo, including $50 million for the current 10th outbreak. The insurance window provides

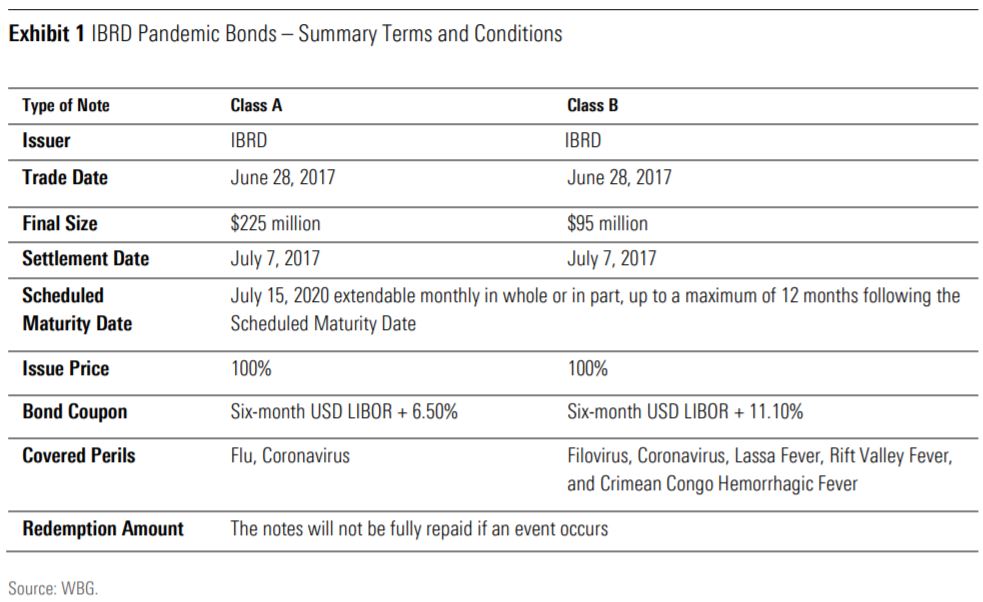

coverage of up to $425 million, composed of pandemic-risk-linked swaps[2] for $105 million and two classes of pandemic bonds for $320 million in floating-rate catastrophe-linked capital at-risk notes issued

in June 2017 (see Exhibit 1). Class A of these pandemic bonds totalled $225 million while Class B

totalled $95 million. Similar to other catastrophe-linked bonds in the market, investors could lose their

principal if a set of parametric triggers, such as outbreak size, growth rate, and spread across borders,

are met.

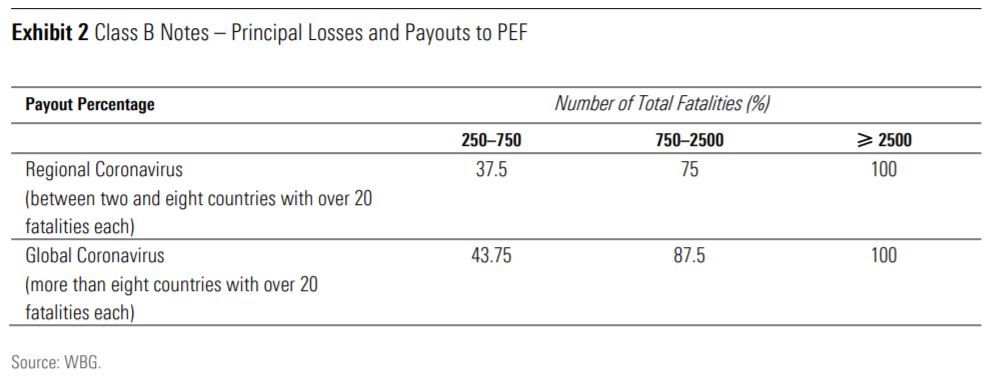

Under the current coronavirus outbreak, investors in both classes of IBRD pandemic bonds can potentially lose all or part of their principal, given the conditions outlined in the prospectus of these pandemic bonds and the most recent statistical information provided by the WHO. However, we estimate that Class B investors are more likely to be affected and the proportional loss of their principal will be higher. For an outbreak to become an eligible event under the terms of the IBRD’s pandemic bonds, it needs to meet a certain level of severity in terms of event duration, number of confirmed deaths, geographical spread, and growth rate.

The Class A Notes would require the current coronavirus outbreak to (1) cause more than 2,500 fatalities in countries and territories specified in the prospectus with 250 cases confirmed on rolling basis, (2) last at least 12 weeks, and (3) cause more than 20 fatalities in a second country. If these conditions are met, the Class A Notes would lose 16.67% of principal or $37.5 million,[3] which will be available for the PEF to distribute among governments of certain countries or specialized international agencies. Based on the most recent data published by the WHO, COVID-19 essentially meets the conditions to trigger the Class A Notes in terms of the number of fatalities and geographic spreads; however, the WHO dates the start of this outbreak on December 31, 2019, which means that the bonds will pay out on March 24, 2020 (the 12-week duration period).

The Class B Notes require fewer fatalities to be triggered (250) while the rest of the conditions are materially similar to those for the Class A Notes. The main difference is that, if all conditions are met, Class B investors would lose all principal ($90 million) on March 24, 2020 (see Exhibit 2). As of the date of this commentary, this would be the case for Class B investors, bringing the total amount available in the PEF to $132.5 million; however, a larger coupon compensates for this higher risk associated with the Class B Notes.

Outlook for the Pandemic Bonds Market

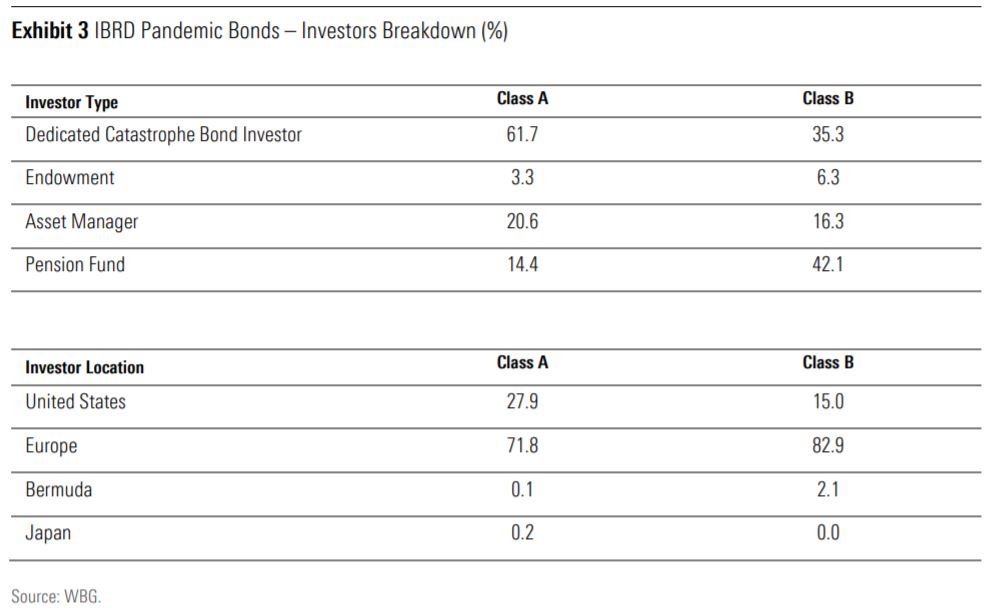

IBRD-issued pandemic bonds amounting to $320 million account for a small fraction of total catastrophe bonds, which are currently sized at approximately $37 billion. Although IBRD pandemic bonds were oversubscribed in 2017 at over 200%, there have been no other issuances of pandemic bonds since. Similar to other catastrophe bonds, defining parametric triggers is not an easy task and IBRD pandemic bonds are no exception with a prospectus of almost 400 pages. Although catastrophe bonds are mostly bought by sophisticated institutional investors (see Exhibit 3), the convoluted definition of trigger events for the different types of pandemics covered might make pandemics bond valuation extremely difficult.

The typical investor in catastrophe bonds is attracted to this asset class because it is generally uncorrelated with the general markets; however, the current coronavirus outbreak is showing that the valuation of pandemic bonds is highly correlated with the performance of global financial markets when it matters most. Pandemic bonds are designed to cover events whose impact is much more global by definition while traditional catastrophe bonds are designed to cover earthquakes or hurricanes, which tend to have a more geographically focalized impact, making them less correlated with the overall global market.

Another objection from public health experts is that pandemic bonds are not designed to help poor countries prevent an outbreak as funding might be available too late. Public health experts have also pointed out that pandemic bonds are quite expensive, given that they have high-interest coupons and that these resources can be invested in the health sector infrastructure of developing countries; however, pandemic bonds were never intended to replace other development aid programs, but rather to introduce market-based funding tools to transfer some risk to the financial markets. Despite a number of complaints in the early stages of the current coronavirus outbreak which highlighted that pandemic bonds would not likely pay out, we believe that they will actually be triggered soon and that resources from principal write-offs will be available to help the poorest countries in the world manage this extreme event. It is still to be seen if investors will remain attracted to pandemic bonds after payouts are activated, but past experience with catastrophe bonds illustrates that interest remains even after large natural catastrophes affect this asset class. We believe that a second round of pandemic bonds can address some existing concerns and remain a viable funding source for low-frequency but high-severity pandemics.

to Trigger Pandemic Bonds&urllanguage=en&urlaffiliate=31151&encoding=UTF-8&urlpicture=https://mobile.next-finance.net/squelettes/images/logo_nf.gif&overview=The current Coronavirus Disease (COVID-19) outbreak will likely trigger payouts for $132.5 million in pandemic catastrophe bonds sponsored by the World Bank Group’s (WBG) Pandemic Emergency Financing Facility (PEF). This funding will be channelled to (...)){kind=link}