Tuesday 1 February marks the Chinese New Year, where millions of people around the globe will celebrate the year of the tiger.

A wave of policy tightening and stringent regulation targeting sectors from property to technology rocked global investment sentiment towards China in 2021. After a challenging period for Chinese investors, Fidelity provides three reasons why China might roar back in the year of the tiger:

With inflation fears, talk of tapering and an investment-style rotation out of ‘expensive’ growth stocks dominating recent headlines across most global markets, diversification and valuations are as important, if not more, than ever. China currently ticks both boxes. The year of the tiger will bring great opportunities.

1. Policy diversion brings diversification

The divergence between the US and European monetary policy compared to China is particularly wide at present. China is certainly at a different stage in the cycle with an easing bias, that history shows often supports markets. Having approached the initial Covid-19 pandemic differently to the loose monetary policy of western governments, China’s central bank has more levers to pull to encourage growth after the slowdown of 2021. The recent cut to the borrowing rate of its medium-term loans for the first time since April 2020 is just one example.

Broadly speaking, while we do not expect the government’s drive towards a healthier, less speculative property sector to be reversed anytime soon, one should not be surprised to see some continued policy fine tuning, such as the supportive measures that have recently been announced. We are already seeing signs of accelerating mortgage approvals in some cities and there is significant scope to loosen policy further.

2. Past the peak of regulation?

We have definitely experienced a period of both new regulation, as well as some tightening of regulations, and for some businesses, the environment has become more challenging. Still it is important to keep a long-term perspective and to remember that we have seen periods of tightening regulation before, such as government-imposed restrictions around online gaming in 2018.

Also, we should not lose sight of the ambitious long-term goals and priorities around economic development and innovation. Achieving these will clearly need a healthy and growing private sector, so despite investor sentiment weakening last year, we believe China offers some interesting long term investment opportunities. Indeed, there is a good chance we are well into, if not past the peak of regulatory reforms, particularly within the technology sector – we would not expect the same degree of intensity that we saw last year and at the end of 2020 to continue.

It is also important to consider that many of the recent reforms are addressing problems that confront countries globally. Big tech and related challenges around anti-trust and data security and privacy are examples, and income inequality is a challenge around the world. Other economies also face many of these challenges and governments will likely act, albeit not as swiftly as Beijing.

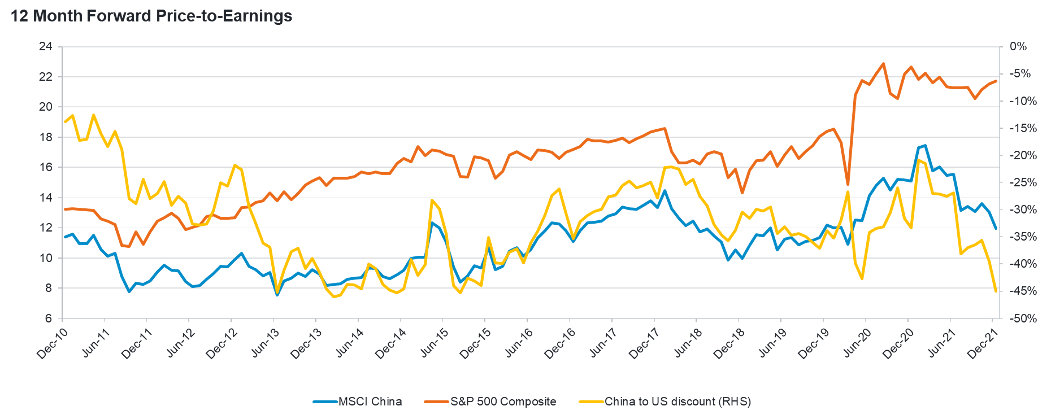

3. Attractive valuations

- Source: Refinitiv DataStream, 31 December 2021. RHS stands for Right hand side.

As is often the case with broad-based corrections, some stocks with lesser regulatory risk have also been sold off, presenting opportunities. Many smaller companies are down despite the fact they will actually be beneficiaries of regulatory action in areas like anti-trust. Further, the valuation gap versus global peers is now excessive, despite similar regulatory challenges in several markets. With valuations where they are, we believe the risk-reward balance is now clearly in the investor’s favour.

The trust continues to have a large exposure to companies that are focused on growing domestic consumption, supported by the ongoing expansion of the middle class. Beneficiaries of this trend aren’t just ‘consumer stocks’ but also in areas like healthcare and technology that also play into the theme of domestic consumption.

It clearly has been a volatile period, but we have seen times like this before, and most likely will see them again. However, history teaches us that these are usually the periods that offer the most attractive opportunities. Corporate earnings for the market are forecast to grow over 15% for the next twelve months. Meanwhile, the market overall is trading on a price earning multiple that is attractive relative to history and relative to other stock markets globally.

As always, the key thing will be individual companies’ ability to deliver on their earnings potential over time.

){kind=link}