Is it now time to take partial profits? Although the year is clearly far from over, the three factors likely to kick-start the markets, that we have been monitoring for several months, appear to be losing momentum and, at the least, other themes are required to extend the rally.

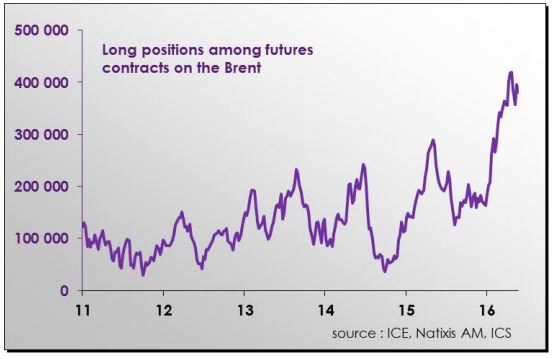

We were counting on an oil price rally to alleviate several of the fear factors present at the beginning of the year. The US energy industry was caught in a downward spiral. Deflationary pressure from falling energy prices maintained the impression that monetary policies were ineffective. Since then however, as we foresaw, the price of crude recovered. Global trade remains sluggish however and supply still outweighs demand. It would therefore appear that the latest rally has been driven by speculative buying, as illustrated by the build-up in long positions among futures contracts.

Long positions among futures contracts on the Brent

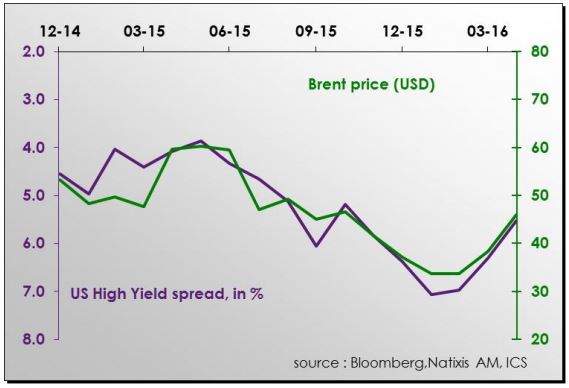

If, as we are expecting, oil prices remain flat, the positive impact that the rally has had on several other asset classes may be undermined. For example, the US high yield market was driven by fresh optimism regarding the oil-price trend, with spreads narrowing in the wake of the US crude price rally.

Oil price and US high yield

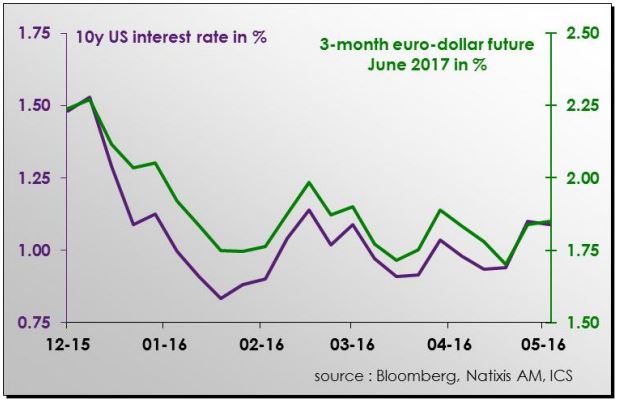

This situation may also be complicated by the Fed adopting a more hawkish tone. The US central bank had deferred taking action following market weakness and amid fears in the international setting. This was the second catalyst for a potential market rally in our opinion. However, Janet Yellen has now had to satisfy the Fed hawks and has once again stressed the improvement in the US economy in order to justify possibly resuming monetary tightening. The difficulty is that US long-term rates, which had tracked short-term rate expectations (in this case the 3-month euro-dollar future), will certainly steepen again. US companies, which are still weathering a slowdown in several economic indicators, will have to face less advantageous financial conditions, just as margins are contracting due to stagnating sales combined with slight wage pressure. As a result, the short term outlook for Wall Street now seems more uncertain.

US: 10y interest rate and short-term rate expectations

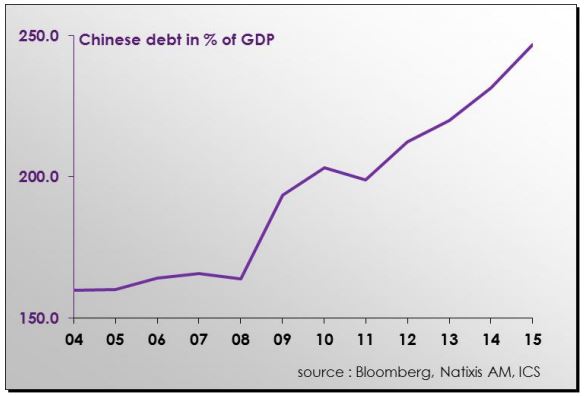

Chinese stimulus measures were the third factor supporting our interest for risky assets. From this point of view, investors seem to have ruled out the risk of a hard landing in the Chinese economy in 2016. However, China’s financial situation is becoming increasingly worrying, with debt levels surging since 2008. Over the past 15 years, Chinese debt has grown three times more rapidly than the economy. Corporate and household debt together equal 207% of GDP. Government debt is estimated at 40 - 55% of GDP. It is problematic for an emerging economy to have an equivalent debt level to industrialised countries (250% global debt/GDP ratio). There is therefore a risk that markets will penalise this type of credit-driven growth, which is unsustainable over the medium term, once investors are reassured that 2016 has been preserved.

Evolution of Chinese debt

Several factors are therefore clouding the horizon for the markets and the best policy is undoubtedly to remain patient, while setting up hedges or taking partial profits. Given the forthcoming electoral incertitude in Europe and in the US, market volatility should provide some better investment opportunities. Although the weather and the climate are, of course, two different things and the horizon may clear progressively, it would be wise to acknowledge that a number of threats are currently looming over the markets, which could cause a sharp drop in returns in Europe, just like the current temperatures!

){kind=link}