Market conditions have been supportive since early July, but the flattening of the Treasury curve raises questions about the probability of a U.S. recession next year. Fund manager surveys suggest investors have erred on the side of caution lately, amid mounting evidence that trade tensions are escalating.

In the hedge fund space, CTAs and L/S Equity funds outperformed lately. The former benefitted from the rise in stock prices as well as from the USD appreciation. The latter was bolstered by its market beta and by the rebound in momentum stocks.

Event-Driven strategies underperformed, both last week and since end of June. The performance of the strategy has been dragged lower by Special Situations managers.

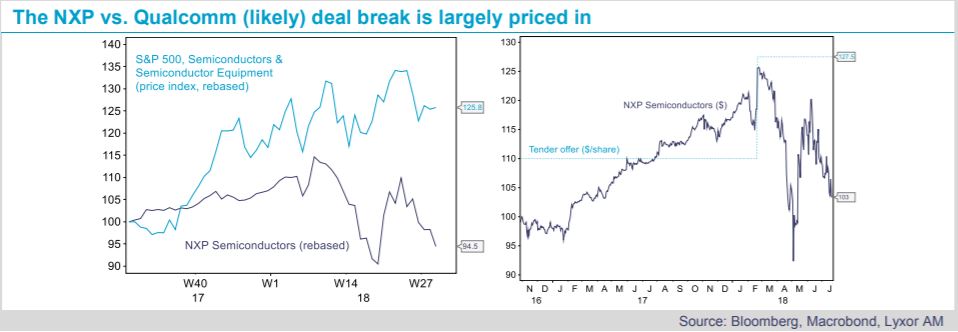

So far this year, Merger Arbitrage strategies performed better than their Special Situations peers, but a key milestone looms this week. Qualcomm’s USD 44 billion cash tender offer for NXP Semiconductors is scheduled to expire this week, and the approval from the new Chinese super-regulator (SAMR) is still pending. The acquisition was announced in October 2016 and the tender offer has already been extended many times. The biggest-ever deal in the semiconductor industry appears to be a hostage of the trade war between the U.S. and China, though the SAMR approved smaller semiconductor deals involving U.S. companies earlier in the year, such as the Microsemi vs. Microchip merger. The SAMR can once again delay the deal review before its expiry on July 25 but it has been reported that Qualcomm doesn’t plan to seek for an extension. The risk of a major deal break looms but we argue that the impact on the performance of Merger Arbitrage strategies is likely to be contained. Anecdotal evidence suggests fund managers have significantly reduced their exposure to the deal over the recent weeks.

Moreover, the deal premium (i.e. the gap between the tender offer and the current stock price), which currently stands in excess of 20%, largely prices in a deal break.

Finally, the likelihood of a contagion from this potential deal break to other parts of Merger Arbitrage portfolios is low, in our view. Overall, the strategy stays attractive in current market conditions (low correlation to stock returns, low volatility).

){kind=link}