With Janet Yellen’s term ending in February 2018, the sweepstakes for Federal Reserve (Fed) Chair is heating up. Media stories about who is favored are appearing with increasing frequency and attracting a lot of attention. Potential candidates are trying to raise their profiles and thereby increase their chances. Furthermore, our clients regularly ask us for our view on who President Donald Trump will pick. Our honest answer is “We don’t know, nor does anybody else.” That stated, we can make some informed observations. While we may or may not get the name exactly right, our thought process, detailed below, may be a helpful guide to watching the contest heat up over the coming months.

At this stage, our approach is to treat the media speculation as just that—speculation. It’s almost certainly too early for the President to have made a final decision. In 2013, President Barack Obama announced his choice of Janet Yellen in the first week of October. The current White House has lagged somewhat in making presidential appointments, suggesting the possibility that Trump’s pick will be announced even later in the year, and meaning a final decision could be more than two months away. Moreover, the appointment process can and likely will take unexpected turns between now and any official announcement. For example, Mitt Romney was a media favorite to be nominated as Secretary of State, and very few commentators even had Rex Tillerson on their list of finalists.

Rather than putting too much weight on the media reports, we prefer to build our own view based on a combination of what Trump has said, our understanding of Trump’s economic priorities and the historical precedents. It is within this context that we find the two quotes above informative and helpful. On their faces, these two statements are somewhat contradictory with regard to reappointing Janet Yellen. But at a deeper level they suggest that President Trump has a pretty clear idea of the characteristics he is looking for: Trump wants his Fed chair to be a Republican, low-interest-rate person.

Republican or Democrat?

The choice of Fed chair is inescapably political. Accordingly, previous presidents have prioritized political affiliation when making their selections. We are inclined to take Trump’s mention of Yellen’s political party as intentional and in line with recent history. Let’s not forget that Yellen served as the Chair of the Council of Economic Advisers under President Bill Clinton, so her affiliation with the Democratic Party is hardly a secret.

An instructive example of the importance of political party can be seen in the transition from former Fed Chair Paul Volcker to Alan Greenspan. Volcker had earned his reputation as an independent central banker by pursuing tight monetary policy in the early 1980s, even though the social costs were significant and there was intense political pressure to lower interest rates. In 1982, a year during which the unemployment rate reached 10.8% and overnight interest rates were above 15%, President Ronald Reagan complained publicly that Volcker and the Fed were “hurting us, and what we’re trying to do, as much as they’re hurting everyone else.” A few years later in 1986, James Baker III, who at the time was Secretary of the Treasury, was worried about the risks posed by an independent Fed as he looked forward to the upcoming presidential election. In particular, Baker was concerned about Volcker, because he feared excessively tight monetary policy could work against the incumbent party’s chances. As an initial step toward moving Volcker out, Baker extracted a promise from a newly appointed Fed Board governor that he would vote against Volcker at his first opportunity. Volcker lost an internal vote immediately after this governor joined the Board in February 1986. Without the support of the Board, Volcker saw his position as untenable, and he considered resigning that very afternoon. Volcker ended up serving another year and a half, although in a somewhat diminished capacity, before informing President Reagan that he would prefer to step down rather than serve a third term[1].

It’s clear that Volcker was a casualty of politics, but was Greenspan part of Baker’s plan? In short, yes. Everything Baker knew about Greenspan made him a good fit for the role. Baker had no reason to doubt Greenspan’s Republican Party affiliation. Greenspan had worked as an adviser on Nixon’s 1968 presidential campaign, where his responsibilities included not only economic policy but also advising on messaging and strategy with regard to the Electoral College. Greenspan later worked in President Gerald Ford’s White House as the Chairman of the Council of Economic Advisers. During that period, Greenspan generally favored lower interest rates, although from his post at the White House he did not have any responsibility for monetary policy. In any case, given his long history with Republican candidates and presidents, Greenspan seemed likely to be a much safer choice ahead of the 1988 presidential election[2].

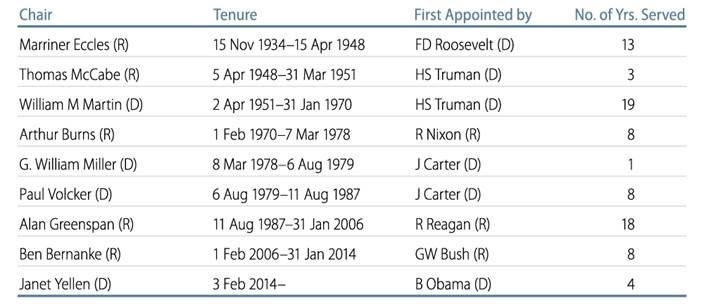

The Volcker to Greenspan transition is just one example of how politics influences the selection of the Fed chair, though it is arguably not the most troublesome. A more egregious example was when President Jimmy Carter selected G. William Miller to be Fed chair in 1978. Prior to becoming Fed chair, Miller had very little monetary policy experience (he was the CEO of a manufacturing company), but he had worked closely with Democratic presidents and party fundraisers in multiple roles. This proved to be the wrong mix of skills and, perhaps predictably, Miller struggled in his role as Fed chair, lasting only 17 months before exiting without distinction (Exhibit 1).

Exhibit 1 | Chairs of the Federal Reserve, 1935–2017

Low-Interest-Rate Person

The emphasis on political party is not all that surprising, given how consequential Fed policy can be for electoral outcomes. Any newly elected president will do everything in their power to boost job growth and raise asset prices, and President Trump is no different in this respect. However, the emphasis on low interest rates may be especially important for President Trump, as maintaining low interest rates would appear to promote two of his priorities: infrastructure and manufacturing.

Infrastructure

The link between low interest rates and construction is obvious and probably doesn’t need to be explored further here. It’s plain to see that President Trump is very familiar with the importance of low financing costs to the overall viability of construction projects. Our view has been that it will be difficult for Congress to pass legislation that substantially increases funding for infrastructure. There does not appear to be consensus within the Republican Party regarding the benefits of such a program, in particular how it should be paid for, and Democrats have been reluctant to work with the President. The slow progress on the rest of the legislative agenda has further diminished the prospects for a large spending bill. However, rather than deterring President Trump’s enthusiasm for infrastructure, this may have the effect of making him even more focused on the boost that low interest rates provides to private developers and builders.

Manufacturing

Low domestic interest rates are commonly associated with a weaker US dollar. Granted, the relationship is far from mechanical—it depends on the relative position of US interest rates to foreign interest rates, and is subject to important caveats (for example, the US dollar has tended to appreciate during financial crises, even though interest rates have been low). Caveats aside, a weaker US dollar is very likely to be good for US manufacturing, as it unambiguously improves the competitiveness of US workers and products. Moreover, because it can be framed as a domestic issue, having low interest rates may be less likely to spark retaliation from our trading partners. This makes having low interest rates a somewhat less risky path to improved competitiveness, as opposed to tariffs, which are inherently international in nature and would be more likely to lead to retaliation. While President Trump certainly cannot directly control the value of the US dollar, he can and likely will exert indirect influence through his pick for Fed chair, and we think this will be an important consideration.

The next Fed chair will have to deal with a lot of nuanced issues in monetary policy: How big should the Fed’s balance sheet be? What parts of the regulatory landscape need changing? Should the Fed change its communication policy? Clearly, there is no shortage of important considerations for the person tapped to fill the role. There are many passionate and eminently qualified Fed chair candidates on all sides of these important issues. Perhaps Trump himself has a view as well. Yet, it seems unlikely that any of these issues is likely to drive Trump’s choice of Fed chair. Instead, Trump is more likely to make his selection based on the thing he knows about—interest rates—and in doing so, we think, will naturally gravitate toward a low-interest-rate person. Not only is that what Trump has said, it is also what is most consistent with his agenda.

So, Who Will It Be?

As we have already acknowledged, we don’t know who President Trump will pick. However, following the above reasoning, we have trouble imagining the appeal of a number of frequently mentioned candidates. Our highest-conviction view is that Trump is unlikely to choose any economist who has been advocating for higher interest rates (e.g., John Taylor), regardless of political party or past experience. Among the broader list of Republican candidates, a number of them have taken principled stands on certain issues such as the size of the balance sheet (e.g., Kevin Warsh) or the future of Fed communications (e.g., Glenn Hubbard). While interesting and useful, these issues are unlikely to be deciding factors for President Trump, who is more likely to focus on interest-rate policy, where neither of these candidates have expressed a clear view.

Another alternative is that Trump could reappoint Janet Yellen. Trump has hinted as much a few times subsequent to becoming President. Yellen has the advantage of clearly fulfilling the “low-interest-rate person” part of Trump’s criteria, which we suspect is the more important of the two. But she falls short on the “Republican” part. While not a bad choice, President Trump may think he can do better than Yellen and look for somebody who fits both his criteria. Gary Cohn has a similar issue, in so far as his affiliation with the Republican Party has been, at best, opportunistic, and he may not be viewed as a reliable ally for President Trump.

With most of the frequently mentioned candidates having clear drawbacks, Trump may extend his search somewhat. One person that may fit both criteria is Jerome Powell. Mr. Powell’s low-interest-rate credentials are intact. He is currently serving on the Fed Board, and over the last five years has consistently voted with the Fed majority to maintain accommodative policy. Mr. Powell is also a Republican. Mr. Powell worked in the Treasury Department under President George W. Bush, and during his confirmation proceedings his Republican Party affiliation was emphasized in an effort to attract votes from Republican senators. Unlike all of the other candidates currently being mentioned, there is little question that Mr. Powell is a Republican, low-interest-rate person. Of course, it remains to be seen whether or not Mr. Powell will be President Trump’s Republican, low-interest-rate Fed Chair.

John L. Bellows, PhD, is a Portfolio Manager and Research Analyst with Western Asset. Prior to joining the Firm in 2012, Mr. Bellows served at the U.S. Department of the Treasury, most recently as the Acting Assistant Secretary for Economic Policy. At Western Asset, he is a member of the US Broad Strategy Committee and the Global Investment Strategy Committee.

Mr. Bellows holds a Bachelor of Arts degree in Economics from Dartmouth College, where he graduated Magna Cum Laude, and a PhD in Economics from the University of California, Berkeley. He also holds the Chartered Financial Analyst designation.

Chair is heating up. Media stories about who is favored are appearing with increasing frequency and attracting a lot of attention. Potential candidates are (...)){kind=link}