Powell’s dovish testimony to the Congress supported investors’ sentiment, with full odds for a rate cut as soon as July 31st. Beyond the Fed, most other major central banks are also taking accommodating measures to tackle declining economic and inflation expectations and policy uncertainties. They are boosting macro and market global liquidity, as reflected in turning M2 indicators and various financial stress indicators. Our basket of assets most sensitive to liquidity (including leveraged loans, frontier markets, EM HY, niche structured products etc.) is continuing to rally and hoard carry flows.

Several credit metrics are deteriorating. Credit valuations are rich, corporate profits and margins are stalling.

Meanwhile corporate cash balances are shrinking as opposed to corporate leverage near its highs (47% of GDP) in the U.S. Yet, we see only few red flags for credit markets for now. We are comforted by trends in the U.S. distressed segment, used as a leading indicator for mainstream markets.

The supply of U.S. distressed debt briefly spiked by the end of 2018 and, to a lesser extent, back in May 2019. However, the outstanding value ($90bn) remains far below the previous peak back in early 2016 at nearly $400bn.

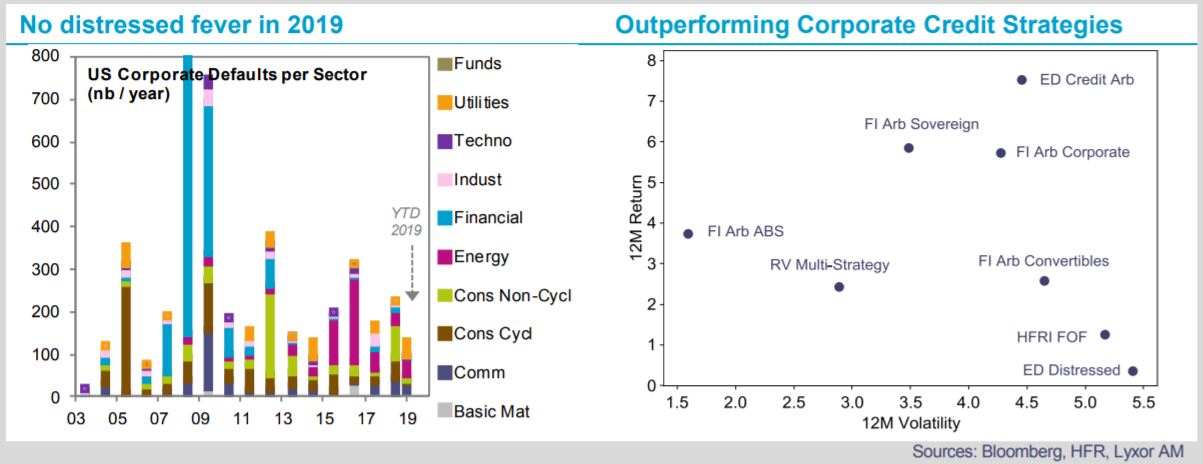

Issues’ bid-ask spreads are consistent with these trends, not suggesting a pending stress. Moreover, most of the distressed issues are concentrated in the energy, healthcare and communication sectors. Interestingly, trade and tech uncertainties are not yet showing in the corporate defaults plotted below.

With only about 12% of the distressed debt maturing within the next two years, liquidity pressure is likely to remain benign. Meanwhile, the number of issuers seeking a maturity extension, amendments or waivers to their financial covenants remain tame. Banks’ corporate loans as well as covenants standards also remain supportive.

Finally, default rates on HY or loans continued to hover around 1.5% year-to-date and are not expected to breach 2% next year. Our view is that the next distressed cycle might not start before 2021.

This is comforting our positive view on credit and deep value market segments. We are O/W in U.S. and European HY and EM HC debt. We are also O/W on Credit and EM Macro focused hedge fund strategies, which could both benefit from decent dispersion and reasonable correlations. While Special Situation strategies hold few distressed issues, opportunities for stand-alone Distressed strategies remain too tight for now.

){kind=link}