Recent data releases in the U.S. have contributed towards stabilizing fixed income markets. Recently released data on wages and retail sales for February were below expectations, while the consumer price index in February grew just in line with the consensus at 0.2% month-over-month and 2.2% year-over-year.

In this context, 10-year Treasury yields have stabilized around 2.85% and concerns over inflationary pressures and additional monetary tightening than currently priced in by the market have somewhat abated. This has been supportive for risk assets, in particular in the U.S. and Emerging Markets.

In the hedge fund space, this has contributed towards extending the winning streak of L/S Equity and Relative Value strategies. So far during the first quarter, both have outperformed the remaining hedge fund strategies. On the contrary, CTAs continue to lag behind, to the extent that market turbulence in February forced them to deleverage their portfolios. This has prevented them from capturing the market recovery.

Going forward, we maintain firm convictions on Event-Driven.

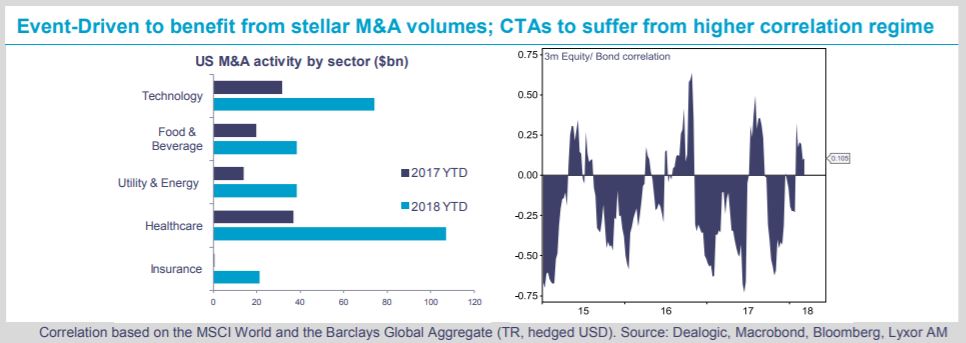

In that regard, it is important to note that M&A activity has started 2018 on very strong footing in the U.S. According to Dealogic, U.S. M&A is up 52% year-to-date compared to the same period last year, at USD 378bn. Health care and technology continue to be the sectors experiencing the stronger pace of consolidation, with volumes worth respectively USD 107bn and USD 74bn year to date (versus USD 37bn and USD 32bn respectively during the same period in 2017).

We also maintain an overweight stance on Fixed Income Arbitrage, a strategy that has delivered attractive returns on a risk adjusted basis in the past and provides protection against rising bond yields. In the L/S Equity space, we prefer U.S. funds compared to European funds. U.S. tax reform might actually generate higher dispersion between stock returns and greater opportunities for L/S funds to generate returns on both their short and long book. Finally, we downgrade CTAs to UW.

We believe that market conditions could remain unstable and trendless going forward. Meanwhile, the rising correlation regime between equities and bonds is also a headwind.

However, we acknowledge the fact that the deleveraging of their portfolios implies that they are less sensitive to trend reversals and their performance should thus be less volatile going forward than it was lately.

){kind=link}