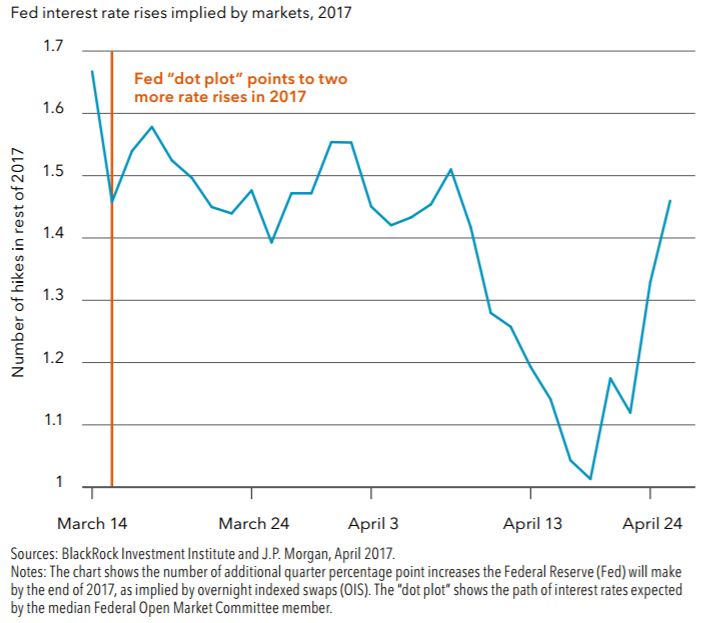

The business-friendly Emmanuel Macron’s clear first-round presidential election win reduced near-term European political risk. Markets are now pricing in nearly 1.5 additional quarter-percentage-point rate increases this year, but we think they still underestimate the Fed’s resolve to tighten policy.

Focus returns to the Fed

The Fed has made clear it views the U.S. economy as nearing the central bank’s employment and inflation goals and accordingly plans to stay on a gradual normalization path. We expect global government bond yields to rise – and prices to fall – as market expectations catch up to our base case of two more Fed rate increases this year.

Strong demand for income and still-accommodative central bank policies in much of the world should help keep rises in yields moderate, in our view. We do expect to see a steepening of the yield curve over time, with very long term yields in particular set to rise as we move from a period of accelerating growth to a new phase of sustained economic expansion.

We see yields on bonds with durations of five years or less as vulnerable in the near term to any jumps in Fed tightening expectations, and we are underweight U.S. Treasuries and European sovereign bonds. Bullish sentiment following the French vote sparked selling of safe-haven assets. Rising European growth and inflation, and the prospect of a less supportive European Central Bank (ECB), may help push European and global yields higher. We expect the Bank of Japan (BoJ) to stay on hold until we see meaningful Japanese growth and inflation.

){kind=link}