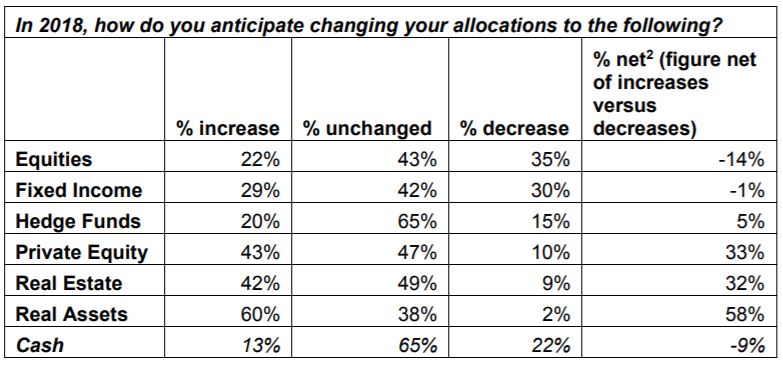

While 65% of clients plan to leave cash allocations unchanged for the year ahead, the survey shows an interest in active management among institutional investors, which should play out across a diverse set of alternative asset classes, including illiquid assets and hedge funds, and also within public equities.

The survey of 224 institutional clients globally, representing $7.4 trillion[1] in assets, found that illiquid or real assets remain the frontrunner within the private market universe for large global institutional investors and are expected to be the largest beneficiary of asset flows. Three fifths (60%) of institutional investors globally are expecting to increase their allocations to Infrastructure and Renewables.

Real Estate is similarly set to gain, with more than two fifths (42%) of institutions increasing allocations to the asset class. Over two fifths of institutions (43%) are looking to increase private equity allocations globally.

“Clients’ intention to reallocate to private markets and other highly active strategies is a recognition that global risks persist and of the value of portfolio managers’ skill. Despite synchronized global growth, our overall return expectations for most segments of institutional investors are well below their return targets”, commented Edwin Conway, Global Head of BlackRock’s Institutional Client Business. “Maintaining current cash levels and increasing allocations to active managers may seem counterintuitive. But for many of our clients, it’s their two-pronged strategy for navigating risk and potentially volatile markets.”

Hedge funds set for inflows, active equities in favour

Hedge funds appear to be back in favour with investors, who have shifted from an intended decrease in 2017 to an anticipated increase in 2018. One fifth of those surveyed (20%) plan to increase their allocations to hedge funds.

Despite an anticipated overall decrease in equity allocations, almost one quarter of institutions (24%) expect to shift allocations to active relative to index investments, versus 16% that plan to do the opposite.

Alternative credit set to capture fresh capital

Globally the hunt for yield means alternative forms of credit such as private credit remain attractive, with over half of respondents (58%) looking to increase allocations. Within credit more broadly, emerging markets also find favour, with almost two fifths (37%) looking to increase allocations here. Overall a decrease is expected in core and core plus allocations (28%), a consistent trend in the survey’s year-over-year results.

Edwin Conway adds: “In the current environment of record-high asset performance, we believe that active portfolio decisions need to be taken by institutional investors this year. For several years, we have been talking to clients about the need to embrace alternative strategies as a way to add diverse sources of return, and offset the current rate environment. It’s gratifying to see them continuing to embrace these assets as they slowly become the norm for institutional investors seeking differentiated sources of return, inflation hedging and counter-cyclical investments.”

Rebalancing survey data

){kind=link}