The latest round of business surveys helped to devise a clearer macro picture globally. According to composite PMI indices, the global economy bottomed out in January 2019 and has experienced a mild rebound since then. PMI data releases last week pointed to an unexpected expansion in China’s manufacturing sector, which fueled risk assets.

However, the German industry was still in deep contraction mode in March and the ECB is trying to figure out which unconventional tools it can now use to stimulate the economy (a tiering system for the remuneration of deposits?).

Despite the mixed signals at the level of individual countries, the rally in risk assets continues unabated on the back of improving economic prospects and looser monetary conditions. In the hedge fund space, CTAs’ winning streak continues (+1.1% last week according to the Lyxor CTA UCITS peer group). CTA strategies that exclude commodities from their investment universe outperformed (+5.9% vs. +3.5% yearto-date for CTAs including commodities). CTAs’ long positions on European fixed income have been rewarded by the poor macro numbers in Germany which dragged bond yields lower. The strategy is now up +5.4% since the trough at end-January but the road to recovery is still long. The drawdown since the previous peak in March 2015 is in excess of 15%.

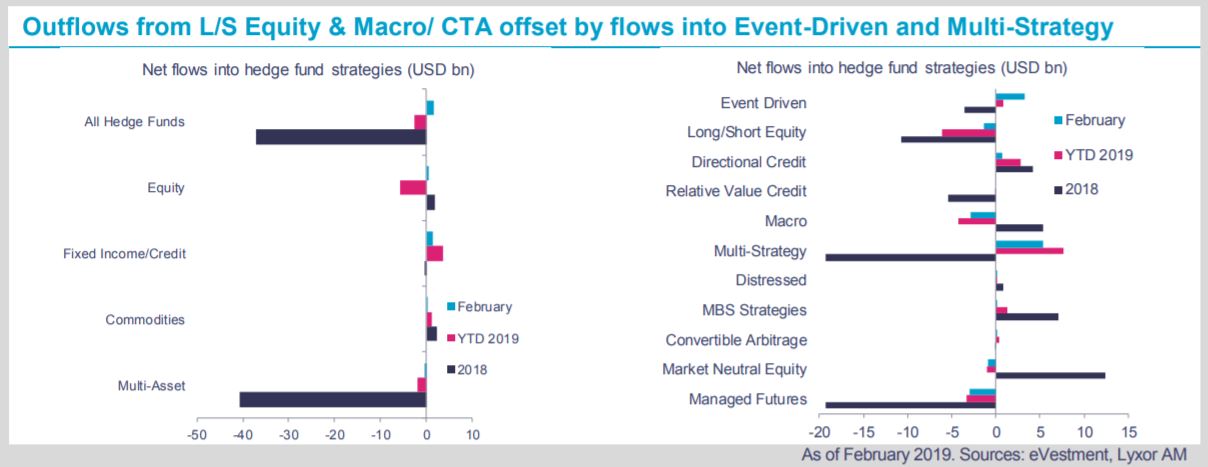

Concurrently, L/S Equity strategies lagged behind. Both Directional and Market Neutral L/S Equity strategies delivered meagre returns in March despite elevated stock dispersion on both sides of the Atlantic. Flows into offshore hedge fund strategies were back in positive territory in February according to eVestment. However, investors’ appetite for L/S Equity remains low. Both directional and Market Neutral L/S Equity strategies experienced substantial outflows in January and February. Based on our Peer Group of 243 strategies, the five worst performing ones in March were mostly L/S Equity, both directional and Market Neutral in a range of -3.3% to -4.3%.

Our views on the strategy stay relatively defensive, though we recently upgraded long biased L/S Equity from Underweight to Neutral to capture some beta in portfolios.

){kind=link}