In the aftermath of the French election, European assets are now in a sweet spot of reduced political tail risks, strong economic fundamentals and relatively easy central bank policy. Adding cheap valuation to the mix, the conditions are in place for European equities to outperform their global counterparts. Admittedly, optimism on European equities is not a new story. But for a long time this optimism has resulted in cheap talk: There seemed to be a lack of conviction behind investors’ positive view of the region.

What’s triggering European outperformance?

Strong economic momentum with growth above US levels and favourable valuation on various metrics has not been enough to trump underlying scepticism among investors. Based on classic valuation metrics like price to book values (P/B), European stocks look cheap. Europe is currently 3% cheaper than its long term median P/B, whereas the US is 10% more expensive. When looking through cyclical swings in earnings relative to prices (Shiller P/E), European companies trade 5% below their average, becoming historically cheap relative to their US peers which trade 38% above their average. But instead of bargain-hunting, investors have remained largely on the sidelines in recent quarters.

With 2017 dubbed a super election year, the lag of conviction has first and foremost been tied to one factor: As long as political risks loom large, investors fail to put their money where their mouth is. The attrition of political risks, therefore is a precondition for the reversal of deeply entrenched scepticism on European equities.

So where are we now, after the Macron victory? It’s likely markets have reached a turning point in their perception of political risk. The worst bugaboo seems to be out of the way, especially from a European perspective. To put it in economic terms, tail risks have been reduced. With the main political hurdle for European equities now having been cleared, we expect investors increasingly to shift their focus back towards the fundamental basics of investing, namely growth, earnings, monetary conditions and valuation.

Politics overpriced, fundamentals underpriced

With the inflection point behind us, it now looks as if political paranoia has been overpriced in European equities. With political risk largely in the rear view mirror, it now looks as if the necessary conditions are in place for European equity outperformance. On top of waning political headwinds and attractive valuation, green lights are flashing on economic momentum, companies’ earnings and monetary policy.

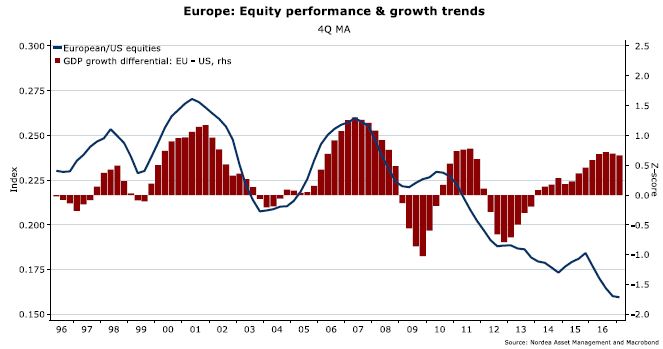

Growth indicators are still going strong in Europe and we expect them to continue to do so, especially relative to other major regions. In 2016, GDP in the Euro Area grew at 1.8%, outpacing US growth at 1.6%. We haven’t seen this scenario since 2008. In other words, the growth differential between Europe and the US has narrowed substantially in recent years. Although this has not been reflected in the performance of European equities relative to the US (see graph), the catch-up potential is tangible.

From a fundamental perspective, companies’ earnings confirm that Europe is turning the corner. Earnings surprises are set up for the best season in a decade. So far, earnings in the first quarter are on track to grow 23% compared to Q1 last year, much better than expected. Looking ahead, future earnings upgrades for European companies are outnumbering downgrades. This has only happened twice over the last five years.

What about monetary conditions? Although the ECB is tightening on an absolute basis through reduced asset purchases, monetary conditions are still much easier in the Euro Area relatively speaking. The European Central Bank still resists calls from some countries to tighten more decisively. While policy rates are rising in China and the US, the ECB is staying put on rates, only making minor adjustments to its macroeconomic risk assessment. This leaves the Euro Area with the most dovish central bank of the three biggest economic regions.

From a market perspective, the flipside of overpriced political tail risks is that fundamental improvements have been underpriced. This is one of the main reasons why European equities have underperformed in 2016 and much of 2017, in our view. The upshot is that there should be quite a lot of juice left in terms of performance. Risk-reward for European equities now looks increasingly attractive to us.

But one size does not fit all

This being said, simply piling into European stock indices might not do the trick. First, there is significant divergence in valuation, revenue exposure etc. between European countries and sectors. Second, with central banks not lifting all boats anymore this divergence should, if anything, grow bigger – between countries, sectors and at the stock level. Finally, the late stage of the global business cycle points towards higher dispersion. While generally a good environment for European equities, late cycle dynamics also result in higher macro uncertainty, potentially increasing the divergence between sectors as well as countries. From an investor perspective, this means one size will not fit all—differentiation is gaining importance. When harvesting European performance potential, active management should be a central part of the investment strategy.

The odds for European equities to outperform global benchmarks are looking favourable, in our view. As political tail risks decline, it’s time to get back to basics: Going forward, European performance should be driven by robust fundamentals in a context of favourable valuation. After a lot of cheap talk, we think investors should consider walking the bullish talk and increase their exposure to European equity.

){kind=link}