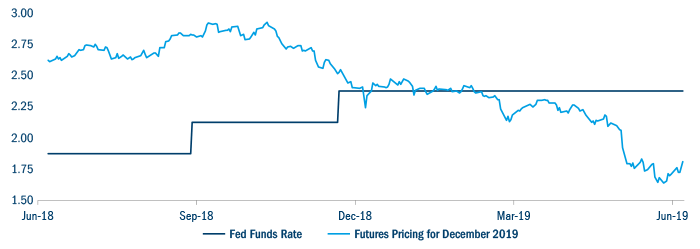

FIGURE 1 – RATE EXPECTATIONS CHANGE FROM HIKES TO CUTS

While interest rate cutting cycles are often associated with recessions, there is greater nuance to the Fed’s approach this time around. Recent research has suggested that when interest rates are low, central banks should respond more quickly and forcefully to the early signs of economic weakness in order to prevent a broader downturn to which it would have limited ability to respond.[1] This supports the idea that the Fed, European Central Bank (ECB) and others should ease policy on a precautionary basis before an actual recession begins in order to prolong the expansion. As Fed Chair Powell recently commented, “An ounce of prevention is worth a pound of cure.”

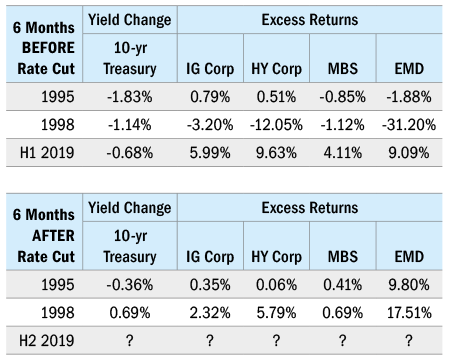

Looking back at history, we can see two relatively recent examples of precautionary rate cutting cycles by the Fed that allowed for economic soft landings, in 1995 and 1998. A closer look at bond market performance around those cycles can be instructive as we review the opportunities in the bond market for the remainder of 2019. Figure 2 shows the experience of the bond market in each of these periods compared with today.

FIGURE 2 – BOND MARKET BEFORE AND AFTER RATE CUTS

Using these two periods as a guide, we see that the bond market was quite volatile before the rate cut, particularly in 1998, but generally performed well when the Fed began to lower rates. Surprisingly, US treasury yields actually rose after the Fed started cutting rates in 1998, as the cutting cycle was more modest than market expectations. In the past six months, we have seen declines in treasury yields alongside strong excess returns in credit sectors. It seems that some of the good news may already be in the price, as returns were very front-loaded. If the Fed delivers the rates cuts markets expect, we could still see further gains, but that is not a sure thing.

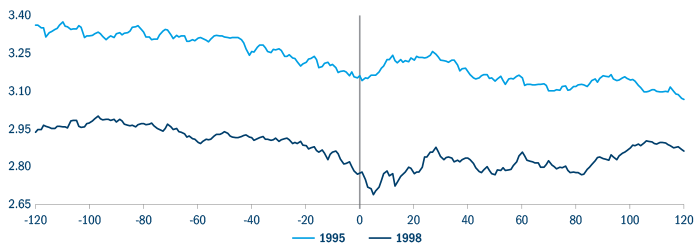

Another motivation behind the Fed’s easing is the structural decline in inflation. Chair Powell mentioned this several times recently, including in his semi-annual address to Congress. History shows that these cuts do impact inflation expectations, but the gains may be fleeting. Figure 3 shows inflation expectations, which saw a much more sustained rise in 1998 vs 1995.[2] We anticipate inflation expectations will rise this time around, particularly if geopolitical tensions continue to put upward pressure on commodity prices. A more sustained rise, however, will depend on greater passthrough of higher wages into service sector inflation.

FIGURE 3 – INFLATION EXPECTATIONS AROUND FIRST RATE CUT

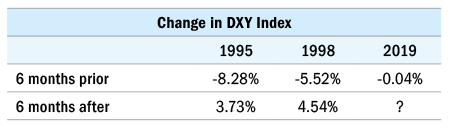

What happens to the US dollar when the Fed eases? Conventional wisdom suggests that lower short-term interest rates would portend a weaker currency. In these periods of preventative easing, however, that was not the case. In each case, the dollar weakened heading into the cut, but strengthened thereafter by about 4%. The dollar has been trading sideways so far in 2019 but remains at historically strong levels. While it will be hard for the greenback to strengthen meaningfully from its current, lofty starting point, history suggests it will be well-supported.

FIGURE 4 – CHANGE IN DYX INDEX

The starting point matters too. Clearly, government bond yields are starting at a lower level. The 10-year yield is just above 2% now, compared with 6.2% in 1995 and 4.6% in 1998. However, other valuation measures are more in line with history. Credit spreads, or risk premiums, in most sectors are wider than they were before the initial rate cut in 1995.

In our view, the Fed is likely to cut interest rates three times before year end. That does not, however, guarantee robust returns from the bond market. Following a lacklustre period for the bond market last year, the first half of 2019 has been quite rewarding to bond investors. We think that performance is unlikely to be repeated. An environment of slow growth and easy money is certainly a tailwind, but investors should not throw caution to the wind. We think the high-quality cash flows of the investment grade corporate and MBS markets will provide the best risk adjusted returns going forward.

){kind=link}