The recent U-turn of major central banks from monetary normalization to renewed accommodation beat market expectations. In particular, the minutes from the FOMC meeting held on 29-30 January suggested the likely ending of the balance sheet runoff at the end of 2019. Bond markets may thus extend their winning streak with the backing of central bankers, especially as inflation continues to be dragged lower by energy base effects. Yet, if credible, this monetary boost could well translate into a bear steepening of the Treasury curve. In our view, the short-end of the Treasury curve is more attractive compared to the long-end. However, our overall fixed income stance remains defensive in both the euro area and the U.S. after the recent rally, despite the fact that this rally does not look stretched compared to the past. The risks for the 10-year Bund yield are asymmetric in our view at current levels.

For the time being, momentum investors are enjoying the tailwind.

Trend followers are on track to deliver their best monthly performance since August 2018 according one benchmark (the SG Trend Index). Our own peer groups, composed of 31 UCITS strategies, point to most strategies (80%) that are in positive territory so far in February. Both the bond market rally and U.S. Dollar appreciation have been supportive. Their net long positioning on bonds has significantly increased over the recent months, while the net equity positioning is back to zero from net short. However, investors will probably need more than a positive month to add to CTA strategies after the difficulties faced last year.

Our views going forward remain tilted towards strategies such as Merger Arbitrage and Fixed Income Arbitrage.

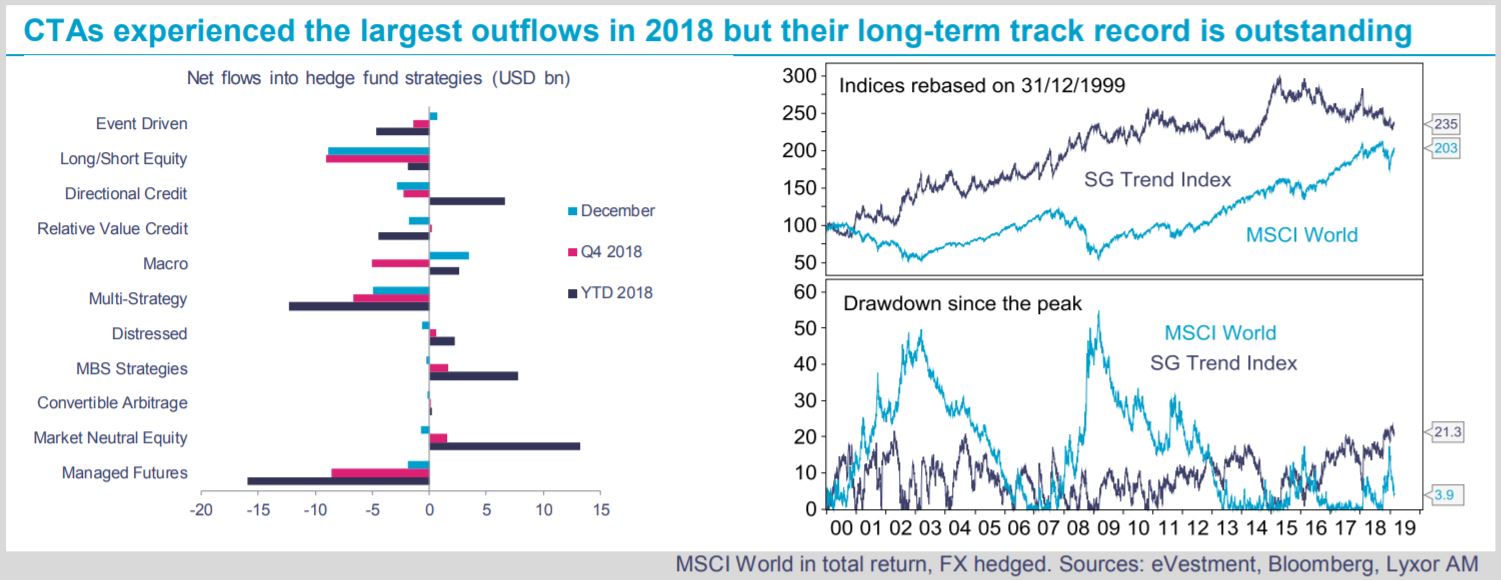

Such strategies have demonstrated their ability to generate alpha over time with a low volatility in returns and a low correlation to equity markets. Our stance on CTAs stays neutral. But it looks like investors capitulated on CTAs last year. According to eVestment, the strategy experienced the largest outflows in 2018. Investors should keep in mind that over the past 20 years, CTAs outperformed equities and their maximum drawdown has been limited to 20% (where it stands now) compared to 55% for equities.

){kind=link}