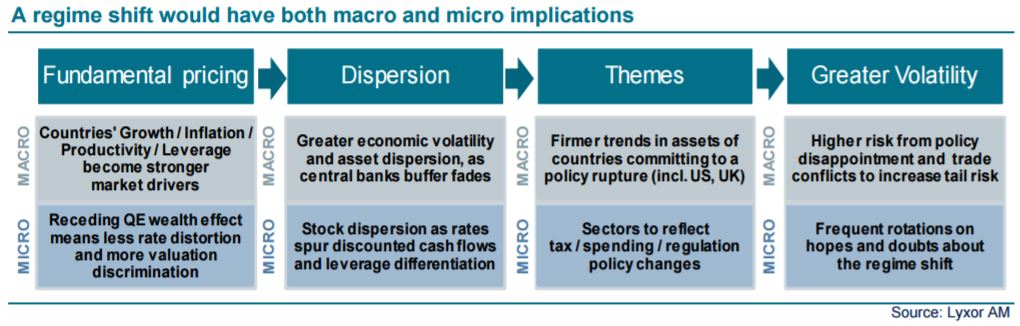

We expect less monetary accommodation, more fiscal push, and more policy ruptures to support an inflection in rates and inflation. Greater dispersion, more typical asset relationships and rising volatility might be in store, especially in the US where the process is more advanced (see below table). These factors would benefit hedge funds. This is not to say that the situation is perfect. The regime shift will be gradual.

If it eventually disappoints, the toll on markets and the economy would be all the more severe. Moreover, a number of factors impairing alpha persist. Yet, the backdrop did improve, calling for some repositioning in our view.

We would reweight US L/S Equity funds, focusing on fundamental styles, as they would be the prime beneficiaries of improving alpha conditions. Small Cap funds are also worth exploring. We expect sector rather than stock alpha in Japan, which is still under QE constraints. We favor Variable over Neutral funds. In Europe, the beta is appealing but would be volatile, leading us to a sO/W on Variable bias and a sU/W on Neutral bias.

We expect US corporate activity to heat up. We are sO/W on US Merger funds as well as on Special Situations which are well positioned on the reflation trade, yet not overly beta exposed. Credit markets might not be the first domino to fall on rates, but they offer mixed beta and alpha which is scarce. We favor multi-credit funds to benefit from dislocations.

Macro funds would benefit from higher macro differentiation, but would still be constrained by political uncertainty. Expect greater fund return differentiation. CTAs’ fate relies on the regime shift’s pace. We are sO/W on LT models after their profound portfolio adjustment. Finally, we expect to increase our focus on volatility strategies by the second half of 2017.

){kind=link}